Stock Markets EM FX ended the holiday-shortened week on a soft note. While most were up on the entire week, notable laggards were TRY, CLP, and ZAR. All three currencies underperformed due to rising political risks, and we suspect that will continue. We believe MXN and BRL are likely to rejoin the laggards in the coming days. Stock Markets Emerging Markets, November 22 Source: economist.com - Click to enlarge Israel Bank of Israel meets Monday and is expected to keep rates steady at 0.10%. Inflation was 0.2% y/y in October, well below the 1-3% target range. However, the bar to further stimulus is very high. Instead, the central bank will likely continue trying to weaken the shekel. Mexico Mexico reports

Topics:

Win Thin considers the following as important: emerging markets, Featured, newsletter, win-thin

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Stock MarketsEM FX ended the holiday-shortened week on a soft note. While most were up on the entire week, notable laggards were TRY, CLP, and ZAR. All three currencies underperformed due to rising political risks, and we suspect that will continue. We believe MXN and BRL are likely to rejoin the laggards in the coming days. |

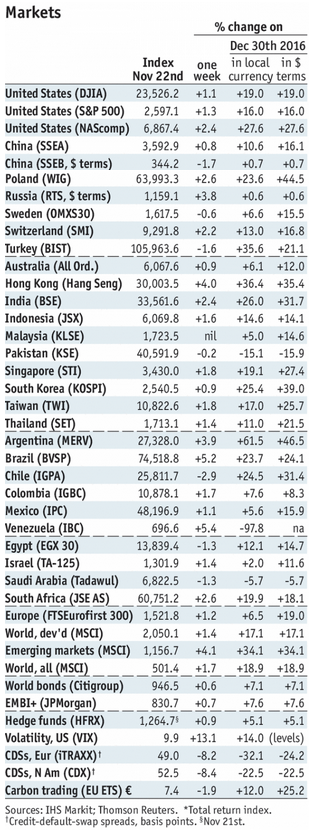

Stock Markets Emerging Markets, November 22 Source: economist.com - Click to enlarge |

IsraelBank of Israel meets Monday and is expected to keep rates steady at 0.10%. Inflation was 0.2% y/y in October, well below the 1-3% target range. However, the bar to further stimulus is very high. Instead, the central bank will likely continue trying to weaken the shekel. MexicoMexico reports October trade Monday. A deficit of -$912 mln is expected. Export growth slowed to 3.4% y/y in September, the slowest since October 2016. With NAFTA talks ongoing, we think markets may become particularly sensitive to Mexico’s trade performance. BrazilBrazil reports October central government budget data Tuesday. A primary surplus of BRL3 bln is expected. Consolidated government budget data will be reported Wednesday, where a primary surplus of BRL3.5 bln is expected. Tax revenues were strong in October, suggesting some upside risks to the budget data. November trade and Q3 GDP will be reported Friday. South AfricaSouth Africa reports October money and loan growth Tuesday. It then reports October trade and budget data Thursday. S&P downgraded South Africa Friday as we expected, whilst Moody’s put it on review for possible downgrade. The S&P downgrade will lead to ejection from Barclays Global Aggregate index, but a Moody’s downgrade will lead to ejection from Citi’s WGBI. ChileChile reports October IP Wednesday, which is expected to rise 5.6% y/y vs. 1.0% in September. It then reports October retail sales Friday. The economy is finally picking up, which supports the central bank’s desire to end the easing cycle. However, low inflation should allow for steady policy until well into next year. KoreaKorea reports October IP Thursday, which is expected to rise 3.2% y/y vs. 8.4% in September. Later that day, Bank of Korea meets and is expected to keep rates steady at 1.5%. Korea then reports November CPI and trade Friday. Inflation is expected to remain steady at 1.8% y/y, just below the target of 2%. ChinaChina reports official November manufacturing PMI Thursday, which is expected at 51.5 vs. 51.6 in October. Caixin reports its China manufacturing PMI Friday, which is expected to remain steady at 51.0. For now, the mainland economy appears to be stabilizing and that is helping the rest of the regional economies. TurkeyTurkey reports October trade Thursday. A deficit of -$7.4 bln is expected. If so, the 12-month total would continue to worsen. Indeed, the external accounts are deteriorating just as it is becoming harder to finance these deficits. Reliance on hot money flows makes the lira even more vulnerable. IndiaIndia reports Q3 GDP Thursday, which is expected to grow 6.5% y/y vs. 5.7% in Q2. The economy is struggling a bit from last year’s demonetization and this year’s introduction of the GST. Still, price pressures are rising as the RBI expects and so we see steady rates for now. Next RBI meeting is December 6, no change is expected. PolandPoland reports November CPI Thursday, which is expected to rise 2.3% y/y vs. 2.1% in October. The inflation target range is 1.5-3.5%. The next central bank meeting is December 5, and no change is expected. However, we do not think the bank will be able to stick with its forward guidance of no hikes in 2018, and look for the first hike in H1. ThailandThailand reports November CPI Friday, which is expected to rise 0.98% y/y vs. 0.86% in October. This would be just below the inflation target range of 1-4%, and should support steady rates well into next year. The next central bank meeting is December 20, no change is expected. PeruPeru reports November CPI Friday, which is expected to rise 1.74% y/y vs. 2.04% in October. This would be the lowest since June 2010. It would also be below the 2% target but in the bottom half of the inflation target range of 1-3%. The next central bank meeting is December 14, and we think another 25 bp cut to 3.0% is likely. |

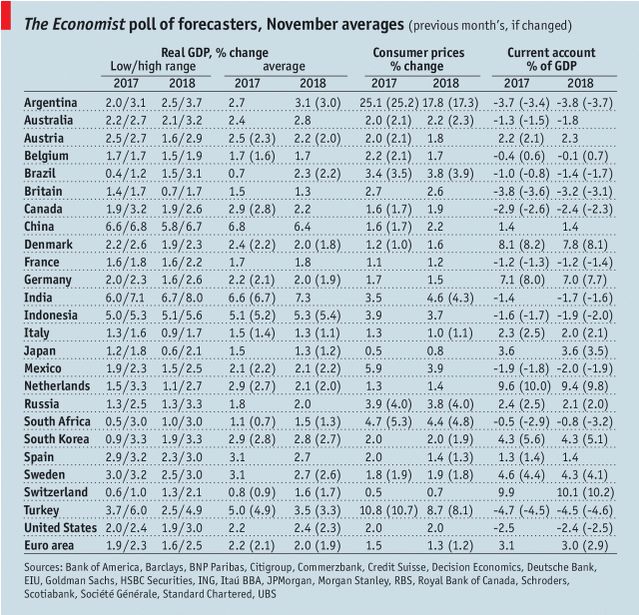

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, November 2017 Source: economist.com - Click to enlarge |

Tags: Emerging Markets,Featured,newsletter,win-thin