Competing forces mean the two currencies could remain in a holding pattern for a while.

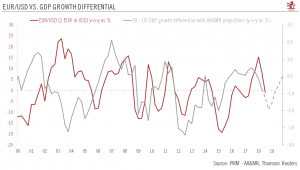

The euro has remained relatively stable relative to the US dollar in the wake of the European Central Bank (ECB) and US Federal Reserve (Fed) September policy meetings. Growth and interest rate differentials, two key drivers for the EUR/USD rate, suggest things could stay this way.

The growth differential (based on leading indicators) has barely budged since March after a sharp decline that began in late 2017. Although we still forecast a narrowing of the gap between the US and the euro area going forward, growth should remain slightly supportive of the greenback, unlike interest rate differentials. Should global growth continue to be sluggish, we believe there is more scope

Euro/USD: things look pretty stable

September 21, 2019