Swiss Economicblogs.org

Swiss Economicblogs.org

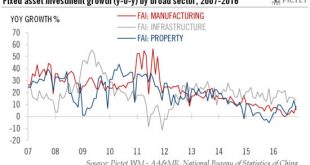

The latest economic data indicate a steady pace in the Chinese economy as 2016 draws to a close. But while we don’t expect a hard landing, 2017 will bring challenges for China on many fronts.The latest data releases out of Beijing indicate steady momentum in the Chinese economy. Exports are showing signs of recovery and investment in manufacturing is helping to offset a recent drop in property investment. All in all, the latest data releases are consistent with our full-year GDP forecast of...

Read More »China maintains economic momentum