Jeffrey P. Snider

December 7, 2018

SNB & CHF

Now that the slowdown is being absorbed and even talked about openly, it will require a period of heavy CYA. This part is, or at least it has been at each of the past downturns, quite easy for its practitioners. It was all so “unexpected”, you see. Nobody could have seen it coming, therefore it just showed up out of nowhere unpredictably spoiling the heretofore unbreakable, incorruptible boom everyone was talking about...

Read More »

Jeffrey P. Snider

September 16, 2018

SNB & CHF

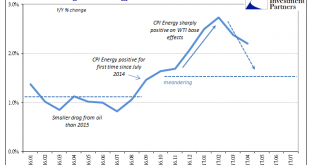

Cushing, OK, delivered what it could for the CPI. The contribution to the inflation rate from oil prices was again substantial in August 2018. The energy component of the index gained 10.3% year-over-year, compared to 11.9% in July. It was the fourth straight month of double digit gains.

Yet, the CPI headline retreated a little further than expected. After reaching the highest since December 2011 the month before,...

Read More »

Joseph Y. Calhoun

August 2, 2018

SNB & CHF

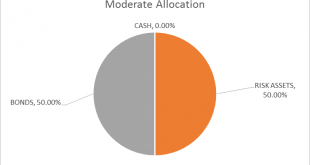

The risk budget is unchanged again this month. For the moderate risk investor, the allocation between bonds and risk assets is evenly split. The only change to the portfolio is the one I wrote about last week, an exchange of TIP for SHY.

Interest rates are on the rise again, the 10 year Treasury yield punching through 3% again this morning. That is an indication that growth and/or inflation expectations have risen...

Read More »

Joseph Y. Calhoun

June 21, 2018

SNB & CHF

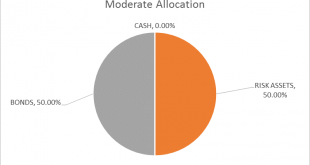

The risk budget is unchanged this month. For the moderate risk investor the allocation to bonds and risk assets is evenly split. There are changes this month within the asset classes.

How far are we from the end of this cycle? When will the next recession arrive and more importantly when will stocks and other markets start to anticipate a slowdown? These are critical questions for investors and ones that can’t be...

Read More »

Marc Chandler

February 16, 2018

SNB & CHF

Summary:

Speculators have a large net short 10-year Treasury position.

The gross short position is a record.

CPI is likely to be softer, while retail sales may show a still robust consumer.

The US reports January CPI figures tomorrow. The market seems especially sensitive to it. The main narrative is that it is an inflation scare spurred by the jump in January average hourly earnings that pushed yields higher...

Read More »

Jeffrey P. Snider

January 31, 2018

SNB & CHF

In one of those rare turns, the term “globally synchronized growth” actually means what the words do. It is economic growth that for the first time in ten years has all the major economies of the world participating in it. It’s the kind of big idea that seems like a big thing we all should pay attention to.

In The New York Times this weekend, we learn:

A decade after the world descended into a devastating economic...

Read More »

Joseph Y. Calhoun

June 7, 2017

SNB & CHF

The economic reports released since the last of these updates was generally not all that bad but the reports considered more important were disappointing. And it should be noted that economic reports lately have generally been worse than expected which, if you believe the market to be fairly efficient, is what really matters. The disappointing employment report and the generally less than expected tone of the reports...

Read More »

Joseph Y. Calhoun

May 23, 2017

SNB & CHF

The economic data releases since the last update were generally upbeat but markets are forward looking and the future apparently isn’t to their liking. Of course, it is hard to tell sometimes whether bonds, the dollar and stocks are responding to the real economy or the one people hope Donald Trump can deliver when he isn’t busy contradicting his communications staff. Politics has been front and center recently but...

Read More »

Jeffrey P. Snider

May 16, 2017

SNB & CHF

The average annual change in the WTI benchmark price was in April about 25%. That was still a sizable increase year-over-year, and just marginally less than March’s average of 33%. For calculated inflation rates, it represents the last of the base effects that have to this point made it appear as if economic improvement was possibly serious.

CPI Changes On Energy, January 2016 - May 2017 - Click to enlarge

Combined...

Read More »

Marc Chandler

January 11, 2017

SNB & CHF

The US 10-year yield fell briefly below 1.32% last July. The yield slowly rose to reach 1.80% in mid-October. The day after the election, the yield initially slipped to almost 1.71%. This was a bit of a miscue, and the yield rose sharply to hit almost 2.64% the day after the FOMC hiked rates for the second time in the cycle on December 14. The yield backed off to hit 2.33% at the end of last week.

The difference between...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org