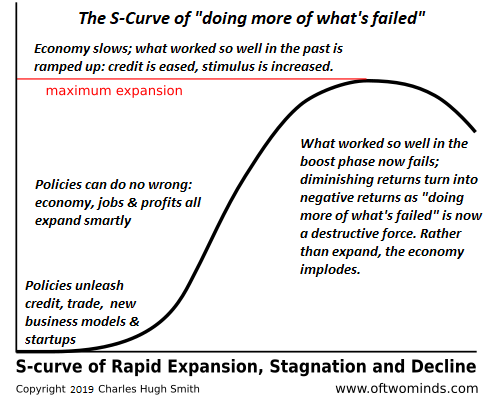

The decline phase of S-Curves can be gradual or a cliff-dive. Way back in 2007 I charted five long-wave cycles that I reckoned consequential: 1. Public debt (accumulating federal deficits) 2. Inflation 3. Oil (energy) 4. Interest rates 5. Speculative fever Fifteen years ago, my chart look-ahead was about three years, to 2010, with the basic idea being that these long-term cycles had already turned or were about to turn. Looking back, I should have added a few other long cycles: demographics, for example. I have two takeaways looking at this chart 15 years later. You probably have similar takeaways. 1. I underestimated the status quo’s ability to kick the can down the road for a decade. The motivation to kick the can down the road was never in doubt; what was in

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

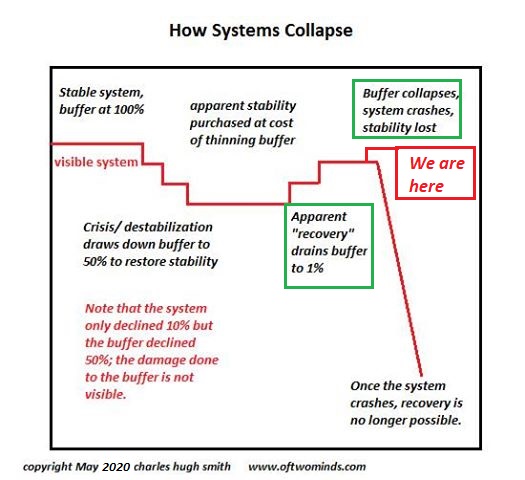

The decline phase of S-Curves can be gradual or a cliff-dive. Way back in 2007 I charted five long-wave cycles that I reckoned consequential: 1. Public debt (accumulating federal deficits) 2. Inflation 3. Oil (energy) 4. Interest rates 5. Speculative fever Fifteen years ago, my chart look-ahead was about three years, to 2010, with the basic idea being that these long-term cycles had already turned or were about to turn. Looking back, I should have added a few other long cycles: demographics, for example. I have two takeaways looking at this chart 15 years later. You probably have similar takeaways. 1. I underestimated the status quo’s ability to kick the can down the road for a decade. The motivation to kick the can down the road was never in doubt; what was in doubt was the system’s ability to respond to doing more of what’s failed spectacularly and keep on keeping on more or less unfazed. 2. After 15 years of frantic can-kicking, the cycles have indeed turned. I would say the predicted turns were correct but frantic can-kicking extended the existing cycle of hyper-financialization / hyper-globalization an extra decade. Various dynamics extended the hyper-financialization / hyper-globalization bubble phase. Fracking in the U.S.–funded by the massive expansion of cheap credit–extended the global energy abundance as the resulting losses were swept away in a tsunami of cheap credit. Zombie frackers were fed as many billions in new loans as were needed to keep the cheap oil flowing. |

. |

| The whole shebang was at risk of unraveling in 2011, but China’s gargantuan credit expansion saved the day, and did so again in 2016. But China’s credit expansion has now reached systemic limits, and so those relying on China to save the global economy yet again from the banquet of consequences are about to be severely disappointed.

The Federal Reserve’s ten-fold expansion of its balance sheet artificially suppressed interest and mortgage rates while various gaming-how-we-measure-what-we-measure tricks understated real-world inflation while hyper-globalization continued deflating costs by shifting production to the lowest-cost regions. The success of frantic can-kicking to extend hyper-financialization / hyper-globalization pushed speculation into hyper-speculation. The monumental bubbles in stocks and housing 1999-2008 now look modest compared to today’s Everything Bubble. The past 20 years have “proven” the profitability of buying the dip which is essentially a bet that there are no limits on frantic can-kicking. |

. |

| Alas, it is now clear that at long last there are limits on frantic can-kicking, and the cycles have turned. The 40-year decline in interest rates has turned, the four-decade quiescence of inflation has turned, the era of low-cost extraction of abundant hydrocarbons has turned, the cycle of being able to “borrow our way out of trouble” has turned and the era of rewarding hyper-speculation has turned.

How gradual or dramatic the new cycle will be is unknown. If we imagine all these dynamics as a pendulum, the pendulum has been pushed by frantic can-kicking to systemic extremes that will reverse to extremes at the other end of the spectrum (minus a bit of friction). The decline phase of S-Curves can be gradual or a cliff-dive. While we don’t know the decay / unraveling trajectory yet, we can anticipate all these long cycle turns reinforcing each other. It’s all one system, after all, and the decay / unraveling of each subsystem will accelerate the decay / unraveling of the other subsystems. As a general rule, it’s a good idea not to stand in the way of the pendulum. Put another way, it’s considerably safer to be in the stands watching the great beasts slouching towards Bethlehem than being on the blood-soaked sand of the Coliseum, clutching a wooden sword and a shredded net. |

. |

You Might Also Like

The Contrarian Curse

The Contrarian Curse

2022-05-07

What if all the new consensus memes are as wrong as the ones they replaced? I have the Contrarian Curse, and I have it bad. The Contrarian Curse is: as soon as the herd adopts your previously contrarian view, you start questioning the new consensus, just as you questioned the previous consensus.

Doom Porn and Empty Optimism

Doom Porn and Empty Optimism

2022-04-29

If we can’t discern the difference between doom-porn and investing in self-reliance, then solutions will continue to be out of reach. I’m often accused of calling 783 of the last two bubble pops (or was it 789? Forgive the imprecision). Like many others who have publicly explored the notion that the status quo isn’t actually sustainable despite its remarkable tenaciousness, I am pilloried as a doom-and-gloomer (among other things, ahem).

Yes, It Is Different This Time

Yes, It Is Different This Time

2022-04-15

Most people would be horrified by a 40% decline in their “investments.” When bubbles pop, speculative assets don’t drop 40%, they drop 90% or even 98%.

Inflation Winners and Losers

Inflation Winners and Losers

2022-01-27

The clear winners in inflation are those who require little from global supply chains, the frugal, and those who own their own labor, skills and enterprises. As the case for systemic inflation builds, the question arises: who wins and who loses in an up-cycle of inflation? The general view is that inflation is bad for almost everyone, but this ignores the big winners in an inflationary cycle.

The Real Threat to Democracy is Corrupting Wealth Inequality

The Real Threat to Democracy is Corrupting Wealth Inequality

2022-01-11

Try to find a developing-world kleptocracy in which the top few collect more than 97% of the income from capital. There aren’t any that top the USA, the world’s most extreme kleptocracy. We’re Number 1. Imagine a town of 1,000 adults and their dependents in which one person holds the vast majority of wealth and political influence. Would that qualify as a democracy?

How Vulnerable Is Your Personal Supply Chain?

2021-12-20

How vulnerable is your personal supply chain? For the average American, the answer is: very. Americans consider abundance and ready availability as birthrights so basic they’re like the air we breathe. The idea that shelves could become bare and stay bare is incomprehensible. yet that is the world we’re entering, for a number of complex reasons.

Smart Enough to Get Rich, Not Smart Enough to Keep It

Smart Enough to Get Rich, Not Smart Enough to Keep It

2021-12-19

Are we smart enough to keep our oh-so-easily conjured riches? If we continue to believe that doing more of what’s failed spectacularly will deliver permanently expanding riches, then the answer is no.

When Everything Is Artifice and PR, Collapse Beckons

When Everything Is Artifice and PR, Collapse Beckons

2021-11-23

The notion that consequence can be as easily managed as PR is the ultimate artifice and the ultimate delusion. The consequences of the drip-drip-drip of moral decay is difficult to discern in day-to-day life. It’s easy to dismiss the ubiquity of artifice, PR, spin, corruption, racketeering, fraud, collusion and narrative manipulation (a.k.a. propaganda) as nothing more than human nature, but this dismissal of moral decay is nothing more than rationalizing the rot to protect insiders from the sobering reality that the entire system is unraveling and heading for its final reckoning: collapse.

Tags: Featured,newsletter