The headlines last Friday were ominous: Inflation Hits Highest Level in Nearly 40 Years Inflation is Painfully High… Groceries and Christmas Presents Are Going To Cost More Inflation is Soaring.. America’s Inflation Burst This morning on Face The Nation, Mohamed El-Erian, former Harvard endowment manager, former bond king apprentice, economist and the man who seems to have a permanent presence on CNBC, had this to say: The characterization of inflation as transitory — it’s probably the worst inflation call in the history of the Federal Reserve. It results in a high probability of a policy mistake. So the Fed must quickly, starting this week, regain regain control of the inflation narrative and regain its own credibility. It would be hard, in my opinion, for the

Topics:

Joseph Y. Calhoun considers the following as important: 5.) Alhambra Investments, Alhambra Research, bonds, commodities, consumption, Crude Oil, Cryptocurrencies, economic growth, economy, eurodollar curve, Eurodollars, Featured, Federal Reserve, growth stocks, inflation, Jerome Powell, job openings, large cap stocks, Markets, Mohamed El-Erian, newsletter, QE, Quantitative Easing, quits rate, small cap stocks, TIPS, treasuries, value stocks, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The headlines last Friday were ominous:

Inflation Hits Highest Level in Nearly 40 Years

Inflation is Painfully High…

Groceries and Christmas Presents Are Going To Cost More

Inflation is Soaring..

America’s Inflation Burst

This morning on Face The Nation, Mohamed El-Erian, former Harvard endowment manager, former bond king apprentice, economist and the man who seems to have a permanent presence on CNBC, had this to say:

The characterization of inflation as transitory — it’s probably the worst inflation call in the history of the Federal Reserve. It results in a high probability of a policy mistake. So the Fed must quickly, starting this week, regain regain control of the inflation narrative and regain its own credibility.

It would be hard, in my opinion, for the Fed to regain something it hasn’t had in a very long time but I guess hope springs eternal.

The Fed’s economic forecasting track record is, quite simply, awful. But Mr. El-Erian’s isn’t any better and that’s why I think the inflation scare is past its sell by date. I wouldn’t say he’s a contrarian indicator but he is the embodiment of conventional wisdom which is rarely wise. I’ve been watching the man for at least 20 years and I can’t remember a single thing he’s ever said that turned out to be true enough to make money on. He is a walking advertisement for passive investing. Besides, he’s a Jets fan.

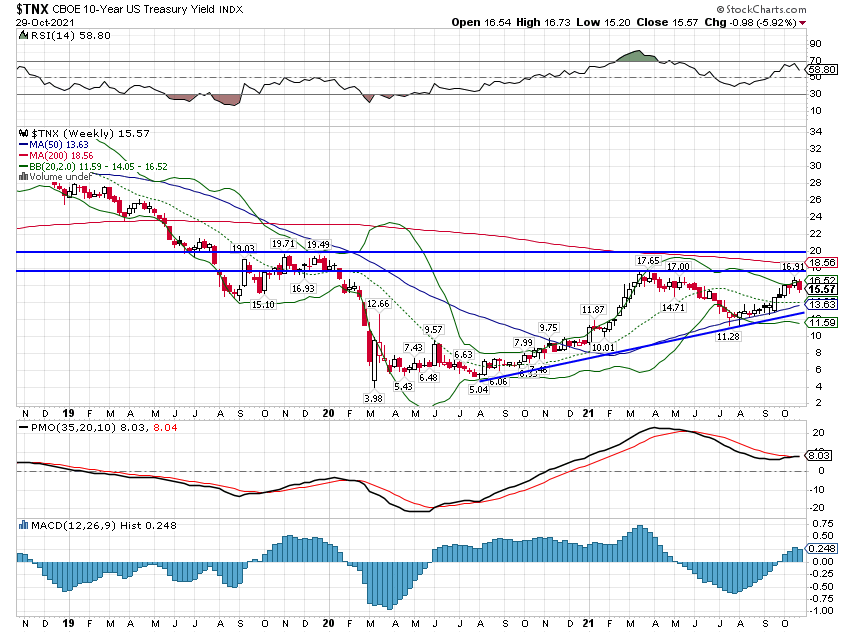

I don’t know if inflation has peaked for this cycle but inflation expectations have, at least for now. Since mid-November TIPS yields have risen as nominal rates have fallen. The 10 year inflation breakeven has fallen by 30 basis points while the 5 year has fallen over 40. All while the headlines have screamed about inflation. This could be temporary I suppose but I see no reason to believe that we are about to repeat the 1970s. The price rises we’ve seen over the course of COVID are not ones driven by monetary policy, regardless of how loose everyone perceives it to be. The culprit is more on the fiscal policy side as politicians provided cash to juice demand when the problems were self-inflicted on the supply side of the economy. Even today, nearly 2 years after the onset of the pandemic, consumption continues well above the pre-COVID trend. The pressure on prices will eventually be relieved as either consumption falls back to the previous trend or supply catches up with the new level of demand. Whichever it is, the Fed doesn’t need to do anything to make it happen.

That isn’t to say that I think Fed policy is now optimal. I don’t believe QE is wise, necessary or effective. I also don’t believe that continuing to hold rates at zero is doing anything except encouraging more speculative activity which is already well beyond anything that is healthy for our economy or society as a whole. Having said that I wonder what the rates complex would look like absent any Fed intervention in the markets. I highly doubt that rates would be a lot higher than they are; the Fed is essentially irrelevant except for their impact on market psychology. I am reluctant to say so but it may be that the speculative nature of today’s financial markets requires a regulatory response. The entire crypto market, in my opinion, is nothing more than a regulatory arbitrage, a convenient way to fleece the public by selling worthless securities that are somehow not classified as such. Or, in the case of stable coins, a convenient way to evade banking regulations. Banking regs are probably too onerous but the proper amount of regulation is surely not none.

If inflation has indeed peaked the implications for markets could be significant. Maybe the most obvious is that the demand for TIPS would likely wane; real rates would rise. That, in turn, would have implications in the real economy. Rising real rates is an indication, generally, of rising real growth expectations. As inflation ebbs, the demand for inflation protection drops freeing up capital for more productive uses. Rising real rates would also be expected to impact gold and could also impact exchange rates. If inflation is peaking the impact will be global.

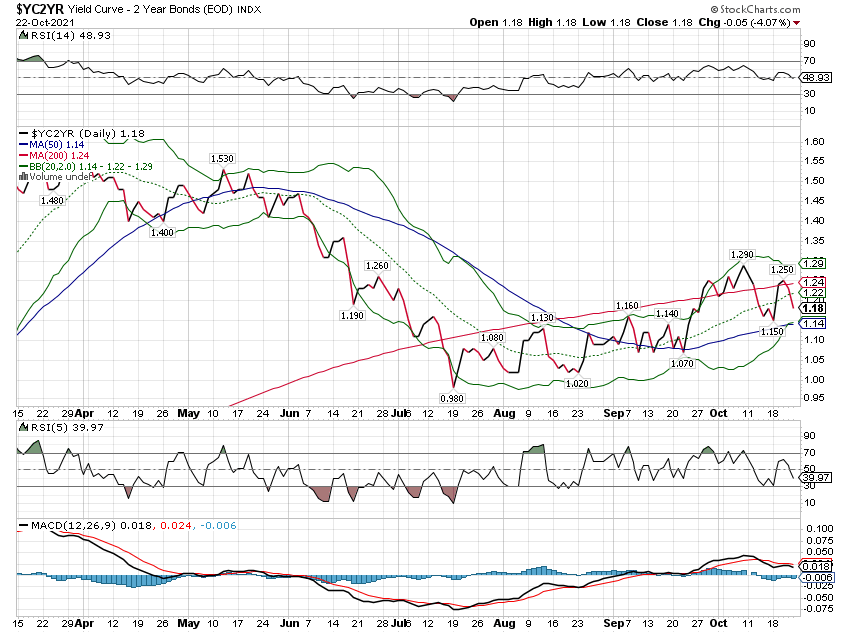

| For now though, the changes are fairly small even if they are in a favorable direction. We can’t declare inflation dead yet and certainly the Fed won’t when it meets next week. If anything, Powell and Co. seem likely to repeat their mistakes of the last cycle and tighten policy into a nominal slowdown. That isn’t imminent as Q4 growth looks quite a bit better than Q3 and nothing in our review of bond markets points to a big slowdown or recession. Jeff Snider has recently pointed out a calendar inversion in the Eurodollar market but the kink in that curve is currently out in 2023/24, meaning that’s where that market sees rates peaking. If that is accurate, we have quite a bit of time before we need to get worried. The term spread (10year/2year spread) isn’t even close to inverting and actually steepened by a couple of basis points last week. A further and larger re-steepening cannot by any measure be ruled out either. But that would require a significant change in long term growth expectations which have been stubbornly low for over a decade. Could that happen? Sure and it may be changes wrought by COVID that make it happen. But I don’t think we can even begin to assess that until all the impact of COVID – and the response to it – has faded. That’s what next year will be about and I’ll have a longer update on our outlook soon.

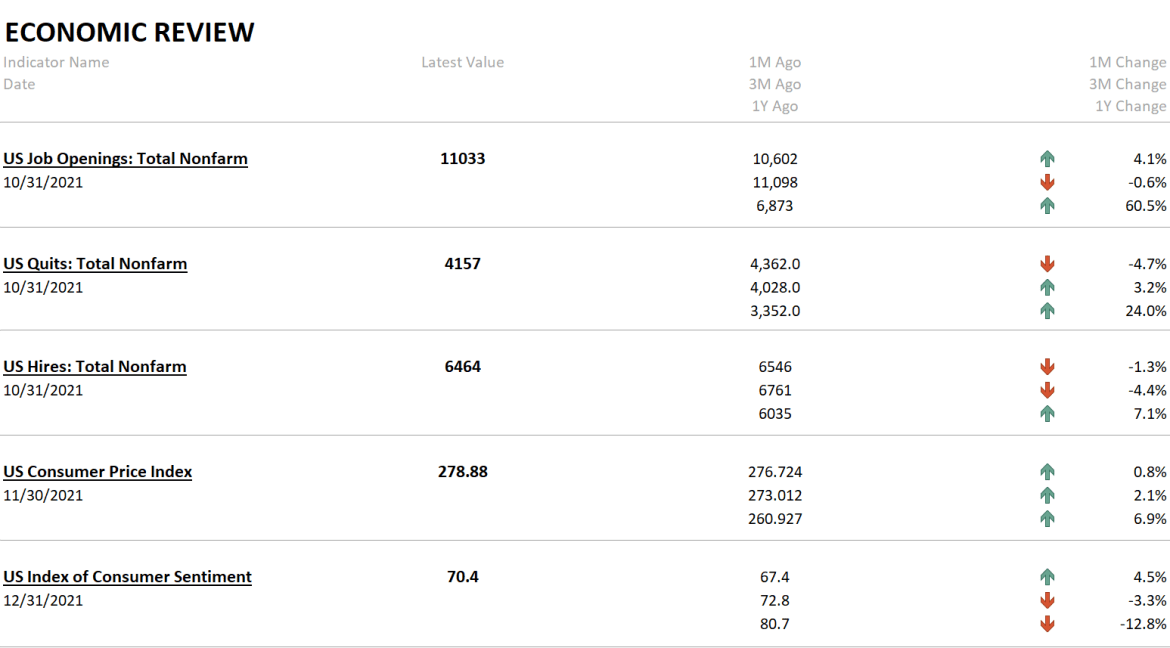

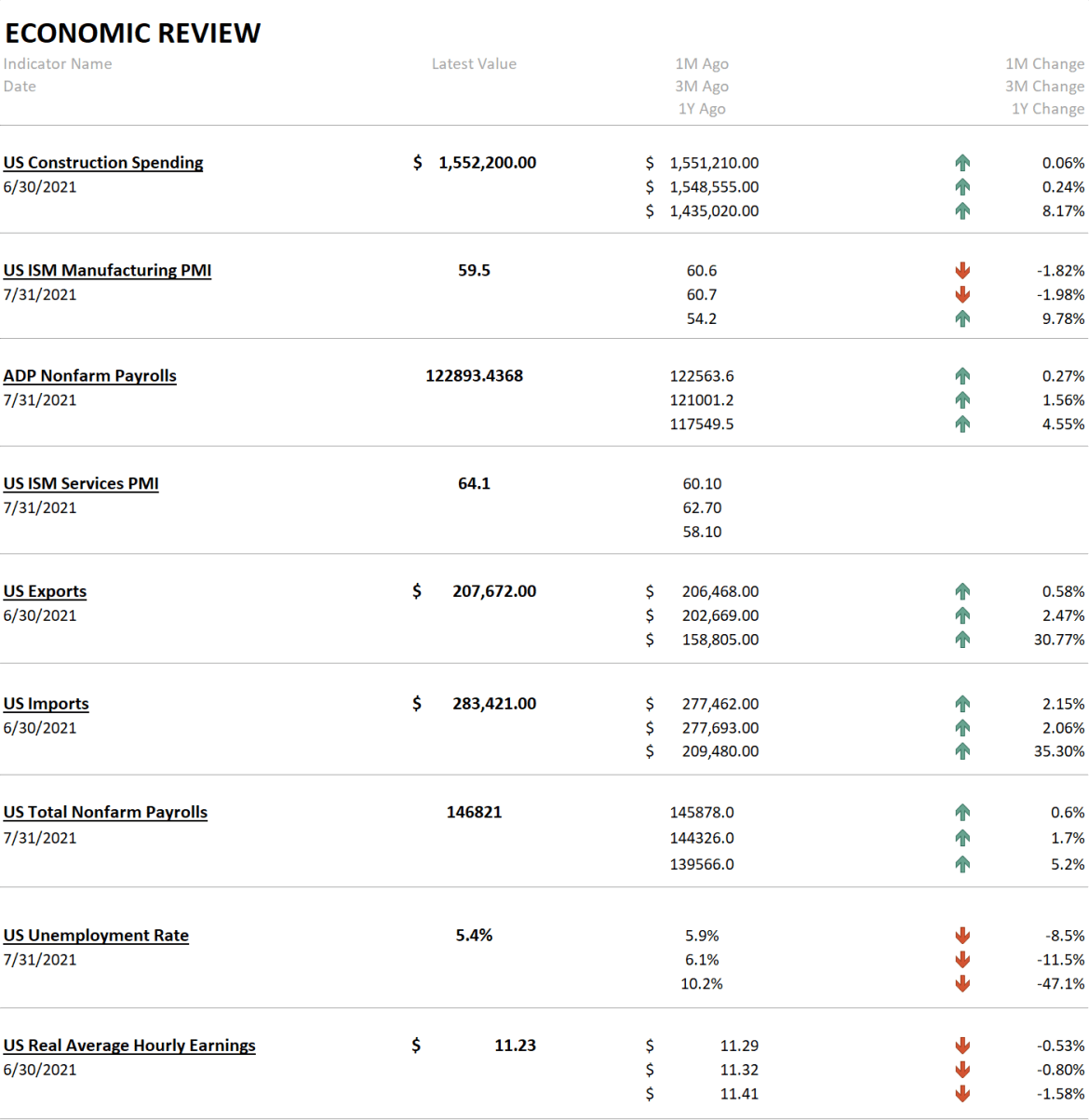

Note: This will be the last weekly commentary this year unless something happens that warrants further comment. I’ll be working on the 2022 Outlook which I expect to publish the first week of January. There wasn’t a lot of data last week but it was generally positive. The JOLTS report continues to show more job openings than folks who want to fill them and people are still quitting their jobs at a furious rate. This churn in the labor market is an example of what I mean about the potential for positive change in the growth outlook. The people quitting their jobs are not just sitting on their couch. We know that new company formations are way above the pre-COVID level but we don’t know what exactly that means. Surely some of it is due to people shifting from employee to independent contractor – some of it involuntary – but we also know a good portion of these new companies expect to hire employees (so called high propensity applications). Recessions and other economic disruptions are often times of great innovation and this one will probably be no different. But change like this doesn’t happen quickly so we’ll have to be patient. One other slightly positive sign was the rise in consumer sentiment. It is still down a lot over the last year but at least it bounced up a bit from last month. |

. |

|

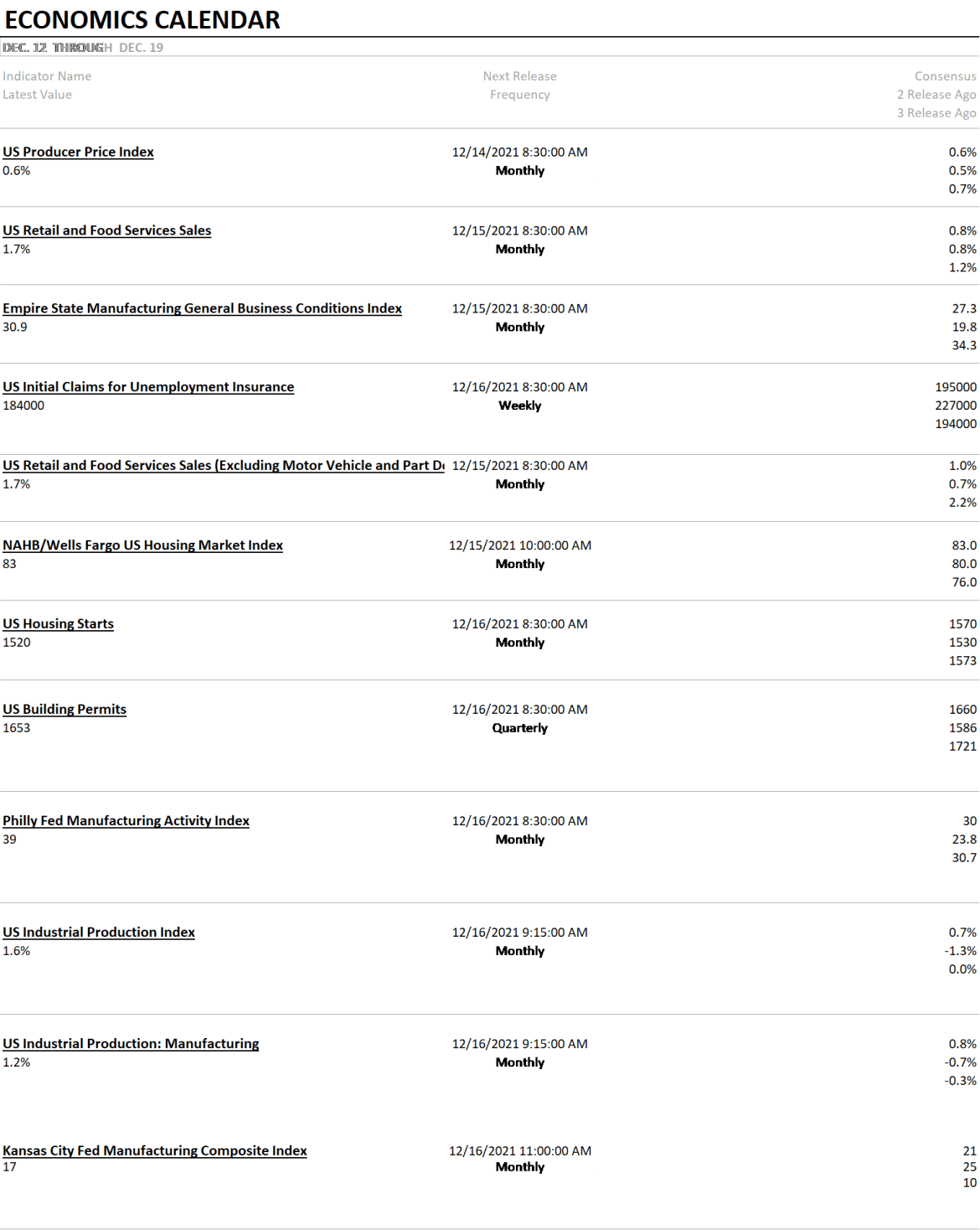

We’ll get some info on whether consumption is starting to normalize – or whether this is the new normal – with retail sales next week. The pattern of retail sales is probably distorted this year by early ordering due to supply concerns so this one could be wildly off expectations. We also get news on housing and industrial production this week. Both are expected to improve. |

. |

|

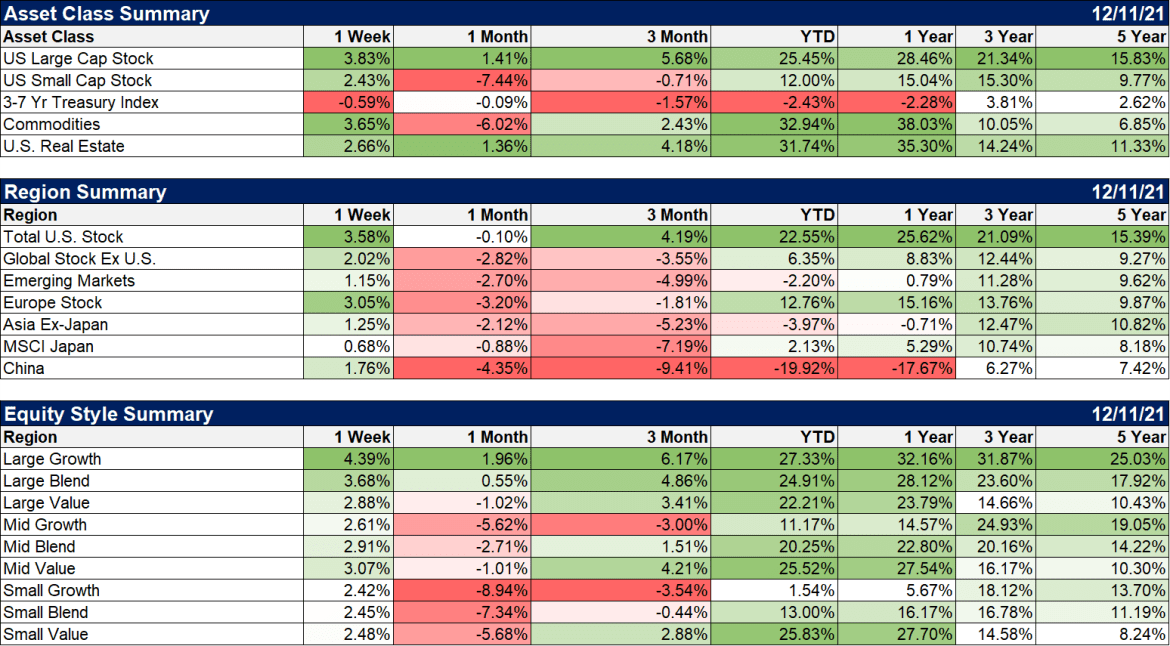

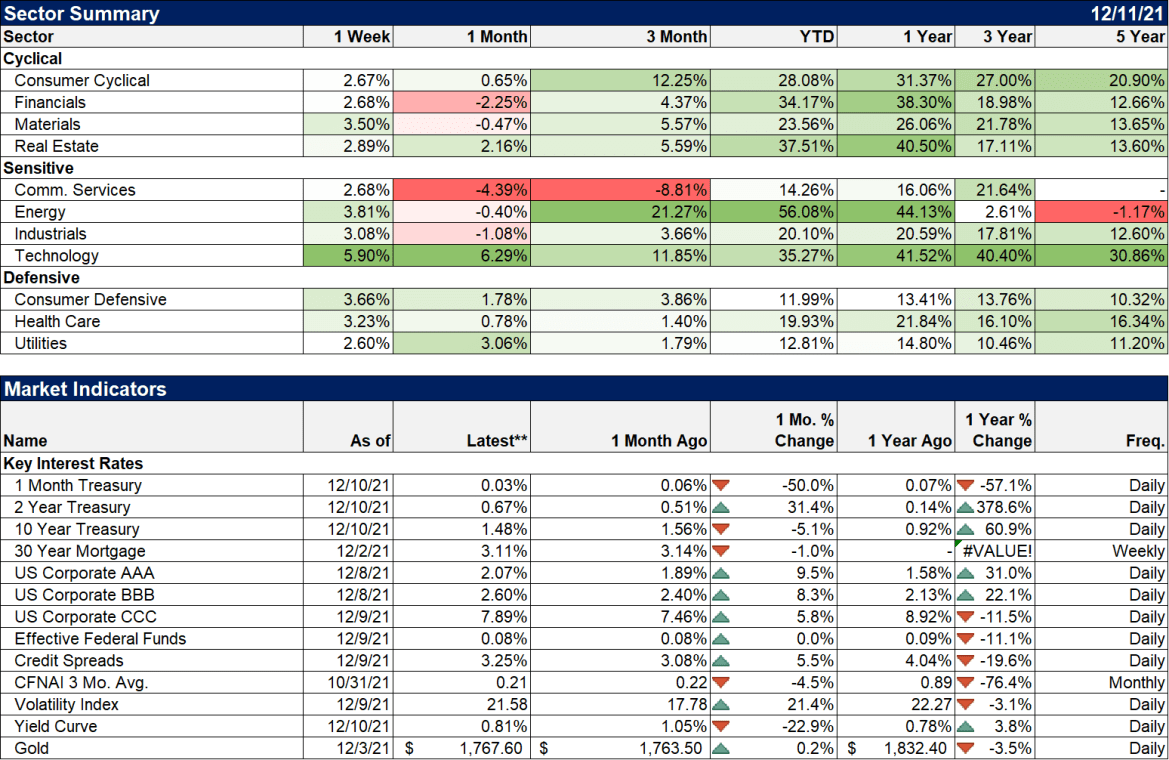

Bonds have been all over the place recently with the nominal 10 year yield peaking the day before Thanksgiving and falling 35 basis points over the next 6 trading sessions. Last week saw yields rise 15 basis points and get some of that back. Risk assets were all higher last week with large cap growth leading the way. We talk a lot about the gap between growth and value but there is another gap that doesn’t get nearly enough attention. Small cap growth stocks are up just 1.5% this year while large cap growth stocks are up 27.3%. So this isn’t just a growth versus value thing. Size matters. Commodities rebounded last week and continue to be the best performing of the asset classes we normally follow. |

. |

| Crude oil led the way, up 8.2% on the week.

The big sector winner was – surprise – technology. Week Happy Holidays to all our readers! We really appreciate you reading every week and providing so much great feedback. |

. |

You Might Also Like

Weekly Market Pulse: Discounting The Future

Weekly Market Pulse: Discounting The Future

2021-12-07

The economic news recently has been better than expected and in most cases just pretty darn good. That isn’t true on a global basis as Europe continues to experience a pretty sluggish recovery from COVID. And China is busy shooting itself in the foot as Xi pursues the re-Maoing of Chinese society, damn the economic costs.

Weekly Market Pulse: Growth Scare?

Weekly Market Pulse: Growth Scare?

2021-11-01

A couple of weeks ago the 10 year Treasury note yield rose 16 basis points in the course of 5 trading days. That move was driven by near term inflation fears as I discussed last week. Long term inflation expectations were and are well behaved.

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!

2021-10-25

The S&P 500 and Dow Jones Industrial stock averages made new all time highs last week as bonds sold off, the 10 year Treasury note yield briefly breaking above 1.7% before a pretty good sized rally Friday brought the yield back to 1.65%. And thus we’re right back where we were at the end of March when the 10 year yield hit its high for the year.

Weekly Market Pulse: Inflation Scare?

Weekly Market Pulse: Inflation Scare?

2021-10-11

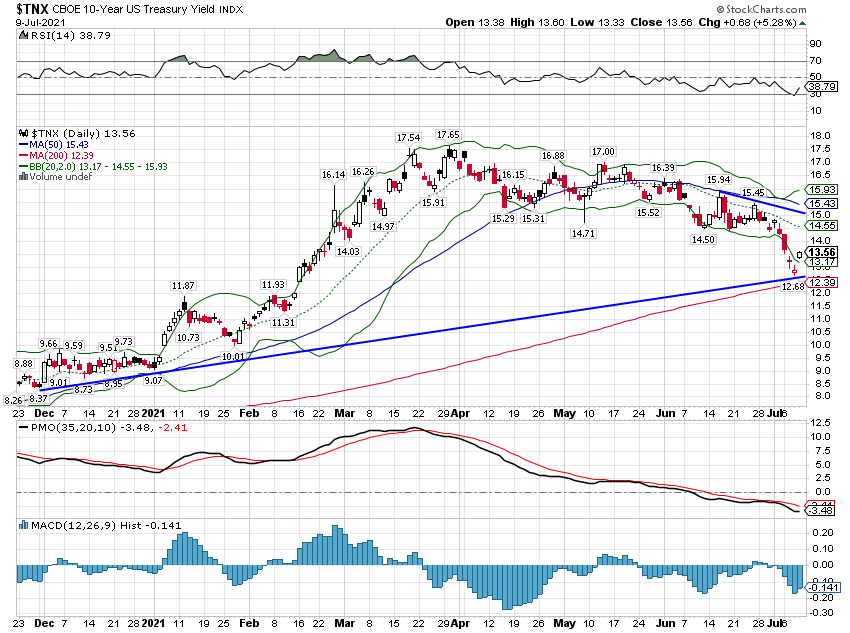

Bonds sold off again last week with the yield on the 10 year Treasury closing over 1.6% for the first time since early June. The yield is now down just 16 basis points from the high of 1.76% set on March 30. But this rise in rates is at least a little different than the fall that preceded it.

Weekly Market Pulse: Zooming Out

Weekly Market Pulse: Zooming Out

2021-10-03

How often do you check your brokerage account? There is a famous economics paper from 1997, written by some of the giants in behavioral finance (Thaler, Kahnemann, Tversky & Schwartz), that tested what is known as myopic loss aversion.

Weekly Market Pulse: What Is Today’s New Normal?

Weekly Market Pulse: What Is Today’s New Normal?

2021-08-09

Remember “The New Normal”? Back in 2009, Bill Gross, the old bond king before Gundlach came along, penned a market commentary called “On the Course to a New Normal” which he said would be:

“a period of time in which economies grow very slowly as opposed to growing like weeds, the way children do; in which profits are relatively static; in which the government plays a significant role in terms of deficits and reregulation and control of the economy; in which the consumer stops shopping until he drops and begins, as they do in Japan (to be a little ghoulish), starts saving to the grave.”

Weekly Market Pulse: As Clear As Mud

Weekly Market Pulse: As Clear As Mud

2021-07-19

Is there anyone left out there who doesn’t know the rate of economic growth is slowing? The 10 year Treasury yield has fallen 45 basis points since peaking in mid-March. 10 year TIPS yields have fallen by the same amount and now reside below -1% again. Copper prices peaked a little later (early May), fell 16% at the recent low and are still down nearly 12% from the highs.

Weekly Market Pulse: Is It Time To Panic Yet?

Weekly Market Pulse: Is It Time To Panic Yet?

2021-07-12

Until last week you hadn’t heard much about the bond market rally. I told you we were probably near a rally way back in early April when the 10 year was yielding around 1.7%. And I told you in mid-April that the 10 year yield could fall all the way back to the 1.2 to 1.3% range.

Tags: Alhambra Research,Bonds,commodities,consumption,Crude Oil,Cryptocurrencies,economic growth,economy,eurodollar curve,Eurodollars,Featured,federal-reserve,growth stocks,inflation,Jerome Powell,job openings,large cap stocks,Markets,Mohamed El-Erian,newsletter,QE,Quantitative Easing,quits rate,small cap stocks,TIPS,treasuries,value stocks,Yield Curve