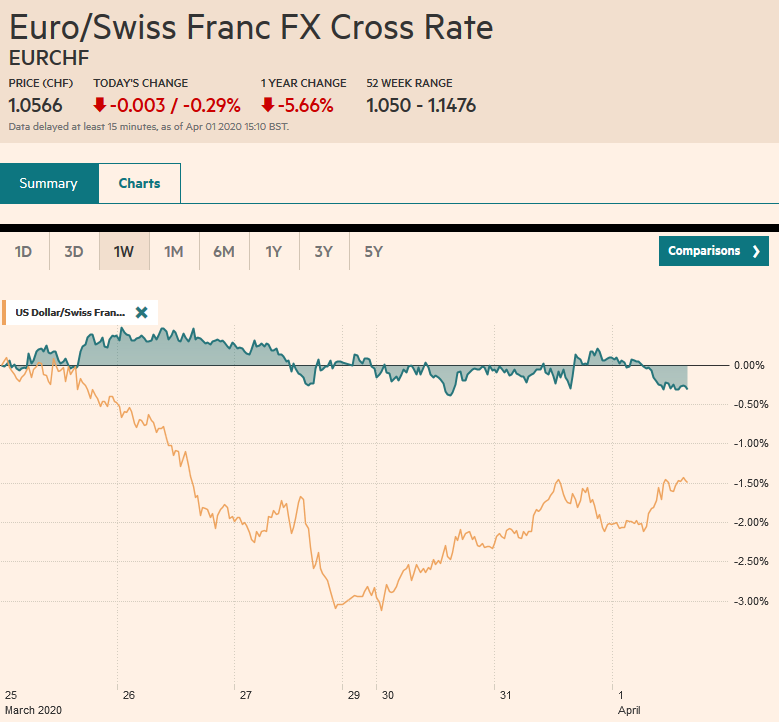

Swiss Franc The Euro has fallen by 0.29% to 1.0566 EUR/CHF and USD/CHF, April 1(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: There is no reprieve for investors. Equities are falling sharply. Nearly all the Asia Pacific markets slumped but Australia. Chinese markets fared better than most, but the Nikkei was off 4.5%, and India was down almost as much in late dealings. Europe’s Dow Jones Stoxx 600 is off more than 3% near midday, led by a sell-off in banks that are suspending dividends and share buybacks. It is giving back the last two days of gains. US share is sharply lower. Yesterday, the S&P 500 gave back half of Monday’s gains, and today it is set to give up the other half and more. Bond markets are

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movement, EMU, Featured, Federal Reserve, newsletter, Repo, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.29% to 1.0566 |

EUR/CHF and USD/CHF, April 1(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

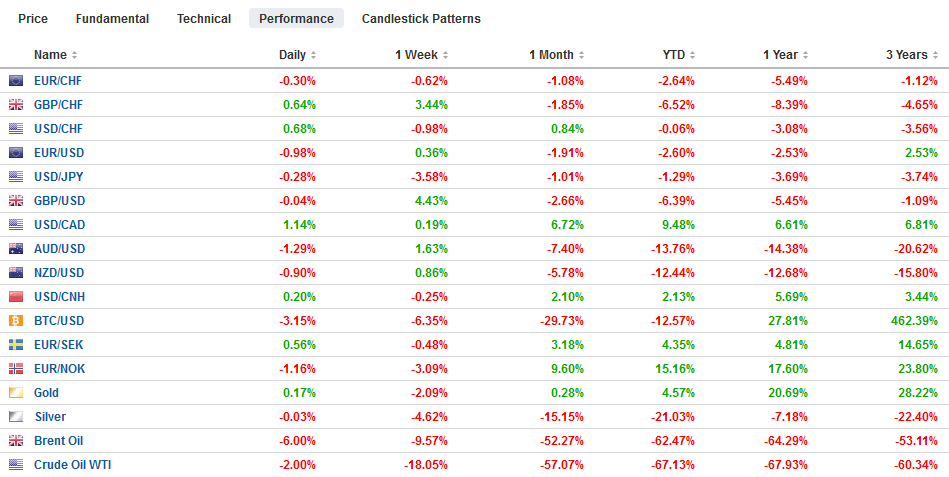

FX RatesOverview: There is no reprieve for investors. Equities are falling sharply. Nearly all the Asia Pacific markets slumped but Australia. Chinese markets fared better than most, but the Nikkei was off 4.5%, and India was down almost as much in late dealings. Europe’s Dow Jones Stoxx 600 is off more than 3% near midday, led by a sell-off in banks that are suspending dividends and share buybacks. It is giving back the last two days of gains. US share is sharply lower. Yesterday, the S&P 500 gave back half of Monday’s gains, and today it is set to give up the other half and more. Bond markets are quieter, but still, the US and UK 10-year benchmarks are around five basis points lower, while peripheral European bond yields are firmer, with Italy’s up five basis points. Core yields are a couple basis points lower. The dollar is extending yesterday’s gains, accept against the yen. Emerging market currencies are nearly all on the downside, led by 1.5%-2.0% losses of the Mexican peso and Hungarian forint. Gold is higher but struggling to reclaim the $1600 handle after giving it up yesterday. Oil is giving back yesterday’s gains with the May WTI contract hovering near $20 a barrel. |

FX Performance, April 01 - Click to enlarge |

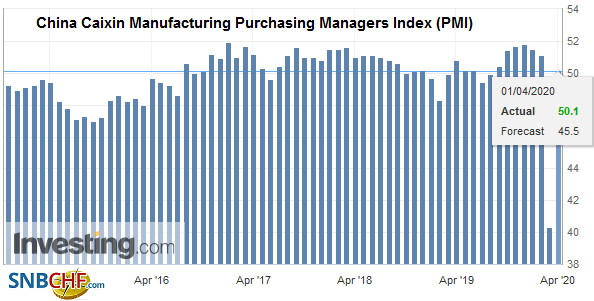

Asia PacificThe news from Asia was mixed. China’s Caixin manufacturing PMI, like the official measure, moved back above the 50 boom/bust level. Taiwan may have been the only other one in the region to report above 50 for the manufacturing PMI (50.4). Other news from the area was poor. South Korea’s manufacturing PMI fell to 44.2 from 48.7, and March exports slipped by 0.2% (economists had forecast an increase). |

China Caixin Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on China Caixin Manufacturing PMI, ) Source: investing.com - Click to enlarge |

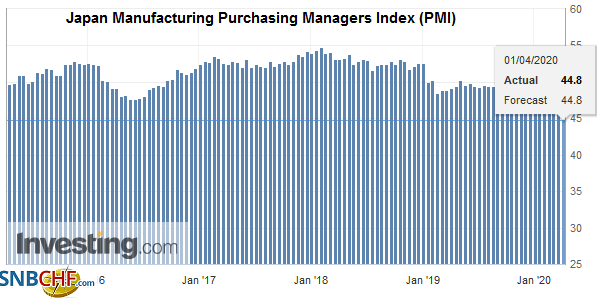

| Japan’s Tankan survey showed deterioration of sentiment that was a little less than forecast. Of note, capex plans were slashed to 1.8% from 6.8%. The March manufacturing PMI was in line with the flash report at 44.8 down from 47.8 in February. Note that Japan’s manufacturing PMI has not been above 50 since last April. Separately, the BOJ reduced the amount of the 3-5 year bonds it bought today, which had been anticipated as they increased the frequency of their purchases. The Abe government is putting together a fiscal package that is expected to be around 10% of GDP in the next week or so. |

Japan Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The dollar is in a relatively narrow range against the yen (~JPY107.25-JPY107.95). The week’s low was set closer to JPY107, where a $1.4 bln option is set to expire today. Yesterday’s rejection of the JPY108.70 area left a bearish shoot star candlestick in its wake, but follow-through selling has been minimal. A break of JPY107 could signal a test on the JPY106.50 area. There is a $1.4 bln expiring option at JPY107.50 and a $2 bln option at JPY108.00. For the past three sessions, the Australian dollar has been knocking on the $0.6200 area but was unable to close above it. It is pulling back today, reaching almost $0.6050. Support is seen near $0.6000 but the (38.2%) retracement of the bounce that began from near $0.5500 on March 19 is found near $0.5945. The Chinese yuan had been in a narrow range for the past two sessions but widened today as the dollar rose to a five-day high near CNY7.1065. For two weeks now, the dollar has been in a range between CNY7.05 and CNY7.1250.

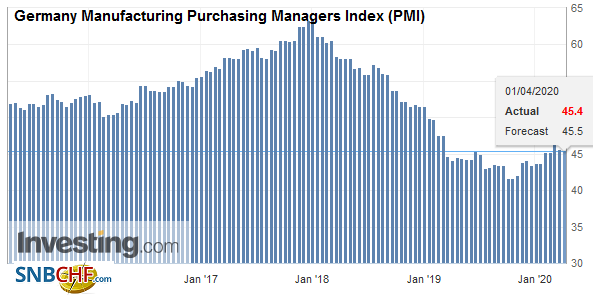

EuropeItaly and the Netherlands are extending their shutdowns, as the manufacturing PMIs give a sense of the economic hit. Italy’s PMI fell to a record low of 40.3 from 48.7. Unexpectedly the Dutch manufacturing PMI eased to 50.5 from 52.9. However, that was the pocket of good news. Germany’s manufacturing PMI was revised to 45.4 from 45.7 of the flash report and 48.0 in February. It has not been above 50 since December 2018. |

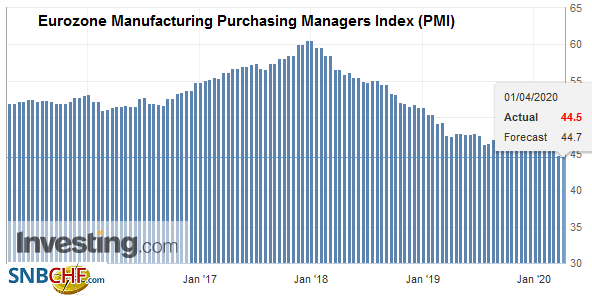

Eurozone Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| France’s PMI edged up to 43.2 from the flash report of 42.9. It was just below 50 in February. Rounding off the large EMU members, Spains’ manufacturing PMI fell to 45.7 from 50.4. The aggregate EMU reading fell to 44.5 from 49.2 in February. The flash estimated was 44.8. |

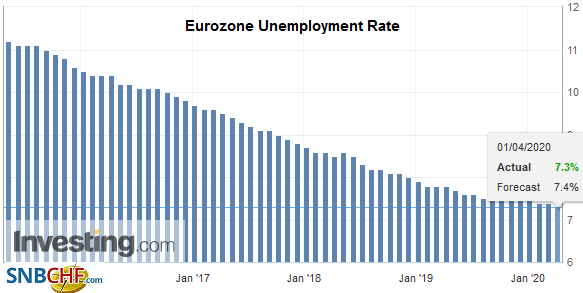

Eurozone Unemployment Rate, February 2020(see more posts on Eurozone Unemployment Rate, ) Source: investing.com - Click to enlarge |

| German reported a 1.2% jump in February retail sales. The median forecast in the Bloomberg survey anticipated a 0.1% rise after a 1% rise in February. And sticking with the counter-intuitive meme, Italy reported a small decline in February unemployment (9.7% from 9.8%), while economists had forecast an increase. We would not make much of these reports as the underlying theme is one of a deep contraction. |

Germany Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on Germany Manufacturing PMI, ) Source: investing.com - Click to enlarge |

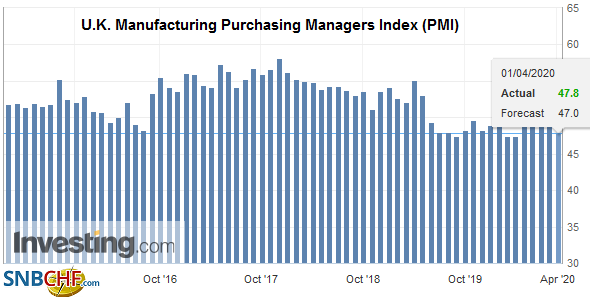

| Consistent with the theme seen among the EMU manufacturing sector, the UK reported its March manufacturing PMI. It fell to 47.8 from the flash reported of 48.0. It stood at 51.7 in February. Separately, UK financial shares are off over 6% today as banks stop dividends and share buybacks. No other sector is down more than 4% near midday. |

U.K. Manufacturing Purchasing Managers Index (PMI), March 2020(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The euro recovered yesterday from around $1.0925 to nearly $1.1040, but the bounce appeared to simply provide some players with a better selling level. It traded flat in Asia before coming off in the European morning to almost $1.0915. The (50%) retracement objective of the recent bounce is found by $1.09, where a roughly 600 mln euro option is set to expire today. A 1.8 bln euro option that also will be cut today is struck at $1.10. Sterling has not broken down as has the euro and is trading inside yesterday’s range (~$1.2245-$1.2475). It has found support near $1.2330 in Europe today. There is an option for a little more than GBP315 mln at $1.2345 that expires today.

America

The US efforts to absorb the economic and financial body blow were extended yesterday. The Federal Reserve moved first. It announced a new facility for foreign central banks to repo their Treasury bonds rather than sell them to raise dollars. It would be an overnight repo that can be renewed. The cost is the interest on reserves (10 bp now) plus 25 bp. In announcing the facility, the Fed explained the intent is to help restore order to the Treasury market. The Fed acts as a custodian for foreign central banks. Its custody holdings of Treasuries fell by nearly $110 bln in March (leaving them with roughly $2.9 trillion. Central banks may have sold Treasuries to raise funds to intervene or as an investment decision after a rally that pushed the benchmark yield below 40 bp in the first part of March. Central banks that wanted to repo their Treasuries could have done so with commercial banks. The Fed may not publish who uses the new repo facility. There may be a stigma to the bank that encumbers its reserves in a public way. It is different than the currency swaps, which seems aimed explicitly at making dollars available to foreign central banks that can make them available to their members.

President Trump signaled that payment for some tariffs will be deferred. The tariffs are not the ones levied on Chinese goods or the controversial tariffs on aluminum and steel on national security grounds. The import tax that is part of the “most favored nation” non-discriminatory will be deferred for 90 days. Footwear and apparel are the big examples, but imported light trucks also will be included. These are like the deferral of the April 15 tax date. The net impact is to boost the liquidity of the taxpayer. It seems to be a tacit acknowledgment of what it seems like everyone knows. Importers pay the tariff, even if it leads to fewer sales by the exporter. Separately, talk of a fourth fiscal package is being discussed, and Trump suggested that should be as much as $2 trillion, which would include a large infrastructure commitment.

Today’s US economic reads come primarily from the private sector. The PMI and ISM are expected to show a hit to the US manufacturing sector, but more interest may be on the ADP’s private-sector job estimate and the auto sales figures. The median forecast in the Bloomberg survey calls for a loss of 150k jobs in ADP’s estimate, which would appear to only be an inkling of what is to come. The weekly jobless claims are the closest to a real-time read of the labor market. Note that NY Governor Cuomo indicated that between March 23 and March 28, the NY Department of Labor got 8.2 mln calls. Typically, it gets 50k in a week. Its website had 3.2 mln hits, almost a 10-fold increase. Auto sales are forecast to slump toward 12 mln (seasonally adjusted annualized rate) down from 16.8 mln in February. Separately, Canada and Mexico report their PMI figures. Mexico also reports March worker remittances. It is an important source of capital inflows into Mexico. Last year, it averaged about $3 bln a month. It may be a little early to see the impact of the economic hit in the US.

The risk-off environment and the inability of oil to sustain even modest upticks are taking a toll on the Canadian dollar. So far today, the US dollar is inside yesterday’s range against its Canadian counterpart (~CAD1.4010-CAD1.4350), but it is looking firm. A move now back over CAD1.4300 could spur a move toward CAD1.4400. The Mexican peso is also on the defensive. The US dollar has pushed a little above yesterday’s high (~MXN24.15). The next targets are in the MXN25.45-MXN24.55 area. Last week’s record high was near MXN25.46. Elsewhere, note that Chile cut its overnight rate to 50 bp from 1% and extended its bond purchase program. The US dollar closed at a record high against the Brazilian real (~BRL5.2060). It reports February trade and industrial production figures today.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, March 30: Monday Blues

FX Daily, March 30: Monday Blues

Overview: Risk appetites remain in check as the spread of the coronavirus is leading to more and longer shutdowns. Asia Pacific equities fell with Australia, the notable exception. Its benchmark rallied a record 7%, encouraged by additional stimulus measures.

FX Daily, April 03: Oil Firm, Greenback Extends Gains

FX Daily, April 03: Oil Firm, Greenback Extends Gains

Overview: Global equities are finishing the week on a soggy tone despite the 2%+ gains seen in the US yesterday. The extension of shutdowns, rising contagion and fatality rate, and imploding economies weigh on prices. In Asia, Korea and Indonesia bucked the trend to most minor gains. Europe is giving back yesterday’s gains, and the Dow Jones Stoxx 600 is nearly flat on the week.

FX Daily, November 13: Investors Temper Euphoria

FX Daily, November 13: Investors Temper Euphoria

Overview: The recent rise in equity markets and backing up in yields spurred many observers to upgrade their macroeconomic outlooks rather than the other way around. Yet we continue to see may worrisome signs. It is not just trade, though, of course, that is part of it. Sentiment itself is fragile and will likely follow prices.

FX Daily, November 19: Hong Kong Stocks Rally as Stand-Off Continues

FX Daily, November 19: Hong Kong Stocks Rally as Stand-Off Continues

Overview: The run-up in equities continues to be the dominant development in the capital markets. Although the Japanese and South Korean bourses fell, the rise in Australia, China, Hong Kong, and Taiwan underpin the MSCI Asia Pacific Index. The Hang Seng’s gains (1.5% on top of yesterday’s 1.3% rise) is notable as the situation on the ground remains intense and unresolved.

FX Daily, January 8: Hopes of De-Escalation Help Markets Stabilize

FX Daily, January 8: Hopes of De-Escalation Help Markets Stabilize

The Iranian retaliatory missile strike on Iraqi-bases housing US forces initially sparked a dramatic risk-off response throughout the capital markets. The muted response by the US coupled with signals from Tehran that it had “concluded” its proportionate measures saw the markets retrace the initial reaction. It was too late for equities in the Asia Pacific region, and several markets (Japan, China, Korea, Malaysia, and Thailand) fell more than 1%.

FX Daily, January 30: Contagion Impact not Peaked, Weighs on Risk Appetites

FX Daily, January 30: Contagion Impact not Peaked, Weighs on Risk Appetites

Overview: The ongoing concerns about the geometric progression of the new coronavirus continues to swamp other considerations for investors. Risk continues to be unwound, as the World Health Organization meets to decide if this is indeed a global health emergency. Several large equity markets in Asia were hit particularly hard.

FX Daily, February 21: Covid-19 Contagion Outside China Keeps Investors on the Defensive

FX Daily, February 21: Covid-19 Contagion Outside China Keeps Investors on the Defensive

Overview: The spread of Covid-19 outside of China and early signs of the economic consequences again emerged to weigh on investor sentiment. Poor Japanese and Australian preliminary February PMI reports and some trade indications from South Korea saw most Asia Pacific equities sell-off. China was an exception. The small gain (0.3%), lifted the Shanghai Composite 4.2% on the week.

FX Daily, March 9: Monday Meltdown

FX Daily, March 9: Monday Meltdown

Overview: Equities plunged, and yields sank as the coronavirus threatens a global recession. The oil price war signaled by Saudi Arabia and Russia aggravates the desperate situation. Equities markets in the Asia Pacific region slumped 3-7%. The Shanghai Composite was fell 3%. The Nikkei was off by 5%, and Australia was hit among the hardest with a 7.3% loss.

Tags: #USD,Currency Movement,EMU,Featured,federal-reserve,newsletter,repo