Corona fears have shifted the world’s central banks into hyperdrive. Talk more, do more, lend more—and buy everything that moves. One after the other, the major central banks took to the barricades, manned the canons, fired their bazookas, and every other military metaphor you can think of. Nobody stopped to think whether the policies that they quickly and loudly announced would work. Nobody investigated whether they could be prevented from reaching their increasingly desperate creators’ desired recipients—nevermind the much bigger questions of whether these goals are desirable or whether central banks ought to do what they’re doing in the first place. “What if,” asked nobody at any central bank during the last few chaotic weeks, “some crucial stage of our

Topics:

Joakim Book considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Corona fears have shifted the world’s central banks into hyperdrive. Talk more, do more, lend more—and buy everything that moves. One after the other, the major central banks took to the barricades, manned the canons, fired their bazookas, and every other military metaphor you can think of.

Corona fears have shifted the world’s central banks into hyperdrive. Talk more, do more, lend more—and buy everything that moves. One after the other, the major central banks took to the barricades, manned the canons, fired their bazookas, and every other military metaphor you can think of.

Nobody stopped to think whether the policies that they quickly and loudly announced would work. Nobody investigated whether they could be prevented from reaching their increasingly desperate creators’ desired recipients—nevermind the much bigger questions of whether these goals are desirable or whether central banks ought to do what they’re doing in the first place. “What if,” asked nobody at any central bank during the last few chaotic weeks, “some crucial stage of our lengthy stimulus chains won’t operate the way we planned?”

After all, it’s not like neatly laid or hastily arranged government plans have ever backfired before.

The mad desire to deal with the crisis, to do something—or at least be seen as doing something—overshadowed anything else.

The European Central Bank delivered an increase in its €2.6 trillion ($2.9 trillion) bond-buying program and offered loans to eurozone banks at –0.75 percent—lower than its already zero interest rate refinancing facilities and below the rate of its previous liquidity-providing and stimulus-enhancing lending facilities. But markets panicked.

Why? President Lagarde hinted that it wasn’t the ECB’s task to manage interest rate spreads between German and Italian bonds (“we are not here to close spreads”), and at the same time tried to offload some responsibility on fiscal authorities. Lagarde quickly backtracked, and the ECB wrote press releases to clarify what she had said and assured that the full range of ECB’s monetary arsenal stood at the ready.

What exactly that arsenal consisted of was still unclear, as there didn’t seem to be much left for an already hyperstimulating central bank to do. On Wednesday they brought out the even bigger guns, from the same tired and dysfunctional arsenal, containing—you guessed it—efforts to buy even more stuff in the form of government and private sector bonds: €750 billion (over $800 billion), a monumental sum, to supply financial markets with extra liquidity. Yet again, Italian and Green bond yields spiked as investors panicked. Something is not working.

On this side of the Atlantic, the Fed hasn’t fared much better. Sunday night last it launched its major crisis-fighting attack by dropping the fed funds rate to the 0–0.25 percent bound and announcing that it would buy $500 billion in Treasurys and $200 billion in mortgage-backed securities, dropping reserve requirements and liquidity buffers.

Stock markets, perhaps unexpectedly in some select corners of the Fed-watching universe, reacted with the second-largest crash in living memory. And here our silly monetary overlords thought that stimulating the economy, providing unfathomably large quantities of liquidity and promises in every way they could, would stabilize financial markets, stave off the impending chaos that we lived through.

Not so much. The Fed acted out of desperation; it truly panicked: here is all we’ve got, guys. Treasury, take it from here!

For each of the next few days the Fed offered repo operations of $500 billion—except that almost no bank made use of them. What is an all-powerful central bank to do if the pesky commercial banks won’t cooperate? This week it extended the earlier facilities by making them “unlimited,” mirroring Mario Draghi’s infamous “whatever it takes” stance during the 2012 eurozone crisis. The Fed also added credit market facilities, with the Treasury footing the bill for losses up to $30 billion.

We’ll see how that monetary bazooka unfolds.

But the most striking corona-fighting story is from the Swedish Riksbank, this hardly admired institution of monetary mischiefs that recently gave up on its failed experiment with negative interest rates.

The Riksbank offered upwards of 10 percent of GDP in direct zero interest loans to businesses, administered through the major banks, which already have business relations with the vast majority of all small- and medium-sized businesses. Banks “better use this facility,” warned Finance minister Magdalena Andersson, and Riksbank governor Stefan Ingves proclaimed that this was “pretty much free money for the banks.”

Except that it wasn’t.

First, it wasn’t free. Banks needed to post collateral in the form of Swedish government bonds—the very securities that the Riksbank’s own QE programs have made a more endangered species than black rhinos. Even ten-year government bonds trade in negative territory, exposing to losses the banks who buy them on the market in order to take advantage of the Riksbank’s emergency funding program. Analysts at the major banks calculated that taking the Riksbank’s “free money” was roughly 20–60 basis points more expensive than the bank’s normal market funding.

No, thanks, said Nordea, the largest Nordic bank formaly under the jurisdiction of the ECB, and pointed to its even cheaper funding from Frankfurt. We’ll pass.

Second, the Riksbank wanted the banks to relend these funds to businesses so that they in turn could weather the impending storm. In theory this is clever. The operation is fast and effective: the banks can quickly forward the Riksbank’s funds to their existing clients, and the Riksbank avoids exposing itself to losses. The banks still hold the default risk, as the Riksbank declined to take that on kindly enough, presuming that making a loan is a simple matter of interest rate.

Showering commercial banks with seemingly cheap loans on the condition that they lend them on to businesses struggling (from a government-mandated shutdown, I might add), would have exposed the banks to much higher losses than they were willing to stomach. This obstacle the Fed tried to avoid by invoking its infamous Section 13(3) clause and offering loans directly to “investment grade companies.”

In desperation, the Riksbank made the facility limitless for three months—perhaps a bigger tasteless carrot will work?—and launched another QE program involving treasuries and municipal bonds (and late on Thursday another one involving direct purchases of corporate debt and lending in dollars through its currency swap agreement with the Fed). As if yields weren’t rock bottom already and the available stock of government bonds weren’t alarmingly low already (not that national governments couldn’t solve that shortage by running extreme deficits, which, by all accounts, they seem to be doing anyway).

Sovereign governments can force their citizens and companies to do (or refrain from doing) all sorts of things, a power that central banks usually don’t have. They can merely regulate, print money, and dangle cheap credit in front of banks—loans that well-capitalized banks are often in a position to reject.

Central banks have one dusty old playbook with about three moves. None of them seems to work now. We have truly reached the end of this monetary experiment of activist central banks.

I wonder when central bankers will realize that.

You Might Also Like

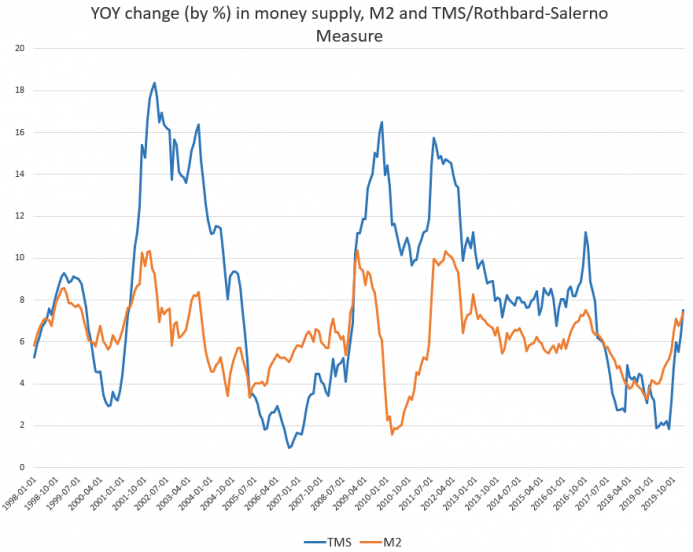

Money Supply Growth Climbs to 37-Month High

Money Supply Growth Climbs to 37-Month High

The money supply growth rate rose again in February, climbing to a 37-month high. The last time the growth rate was higher was during February of 2017, when the growth rate was 7.9 percent. During February 2020, year-over-year (YOY) growth in the money supply was at 7.49 percent. That’s up from January’s rate of 6.32 percent, and up from February 2019’s rate of 3.20 percent.

Government Is No Match for the Coronavirus

Government Is No Match for the Coronavirus

The coronavirus is reminding everyone that you cannot rely on government and that ultimately it is the private sector that will provide the solutions. Many nonmedical government officials and members of the media are predicting massive cases of COVID-19 and death, when in fact no one can predict the outcome.

Financialization: Why the Financial Sector Now Rules the Global Economy

Financialization: Why the Financial Sector Now Rules the Global Economy

To read or watch the news in today’s world is to be confronted with a wide array of stories about financial organization and financial institutions. News about central banks, interest rates, and debt appear to be everywhere.

No, Technology Shocks Aren’t Behind Recurring Business Cycles

No, Technology Shocks Aren’t Behind Recurring Business Cycles

Economic fluctuations, also known as business cycles, are seen as being driven by mysterious forces that are difficult to identify. Finn Kydland and Edward C. Prescott (KP), the 2004 Nobel laureates in economics, decided to attempt to find out what these forces were.1 They hypothesized that technology shocks are a major factor behind economic fluctuations and demonstrated that a technology-induced shock can explain 70 percent of the fluctuations in the postwar US data.

In Spain You Can’t Use Your Own Back Yard. Police Make Sure of It.

In Spain You Can’t Use Your Own Back Yard. Police Make Sure of It.

The last days and weeks of the coronavirus epidemic give an interesting insight into the human psyche. Elementary liberties are restricted all over the world, such as the freedom of movement or private property. Yet most people accept these restrictions without blinking, as the state declares their indispensability.

The European Central Bank Is Being Stretched to Its Breaking Point in Italy

The European Central Bank Is Being Stretched to Its Breaking Point in Italy

When Mario Draghi’s tenure was approaching its end, I argued for a sterner governor for the European Central Bank (ECB); hence, I was not even slightly enthusiastic when Draghi’s successor turned out to be Christine Lagarde—a patent dove, as can be inferred from her ideological proximity to a famous Keynesian like Olivier Blanchard.

Diseases Are Bad. Government-Forced Shutdowns Are Often Worse.

Diseases Are Bad. Government-Forced Shutdowns Are Often Worse.

However high the death rate of the COVID-19 coronavirus becomes, the governmental response to the threat will be even more dangerous. If the current blockade of economic life continues, more people will die from the countermeasures than from the virus itself. In a short time, the basic supply of everyday goods will be at risk. By interrupting the global transport and supply chains, important medicines will be missing and food supplies will be insufficient.

Budget Deficits, not “Neoliberalism,” Are To Blame for Argentina’s Crisis

Budget Deficits, not “Neoliberalism,” Are To Blame for Argentina’s Crisis

Argentinians are known for for slinging clever insults. Spaniards, for example, love Argentine “puteadas” so much that they created a website called “Curse like an Argentinian.” Now in the world of bad words, one stands out that, when received, mortally wounds the rival in the argument. It’s hard to recover after such an attack. Curiously, this insult can be written without violating the rules of decorum.

Tags: Featured,newsletter