Jeffrey P. Snider

November 3, 2018

SNB & CHF

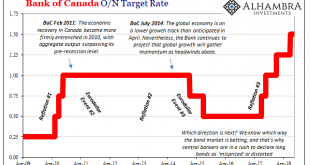

Trade war stuff didn’t really hit the tape until several months into 2018. There were some noises about it back in January, but there was also a prominent liquidation in global markets in the same month. If the world’s economy hit a wall in that particular month, which is the more likely candidate for blame?

We see it register in so many places. Canada, Europe, Brazil, etc. It does seem as if someone flipped a switch...

Read More »

Jeffrey P. Snider

September 2, 2018

SNB & CHF

The US yield curve isn’t the only one on the precipice. There are any number of them that are getting attention for all the wrong reasons. At least those rationalizations provided by mainstream Economists and the central bankers they parrot. As noted yesterday, the UST 2s10s is now the most requested data out of FRED. It’s not just that the UST curve is askew, it’s more important given how many of them are.

Look to our...

Read More »

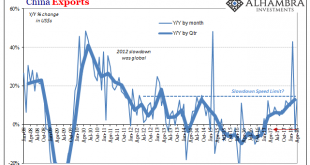

Jeffrey P. Snider

May 12, 2018

SNB & CHF

Chinese exports rose 12.9% year-over-year in April 2018.

China Exports, Jan 2008 - Apr 2018(see more posts on China Exports, ) - Click to enlarge

Imports were up 20.9%. As always, both numbers sound impressive but they are far short of rates consistent with a growing global economy. China’s participation in global growth, synchronized or not, is a must.

The lack of acceleration on the export side tells us a lot...

Read More »

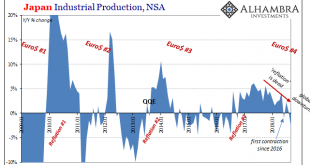

Jeffrey P. Snider

April 4, 2018

SNB & CHF

Japanese industrial production dropped sharply in January 2018, Japan’s Ministry of Economy, Trade, and Industry reported last month. Seasonally-adjusted, the IP index fell 6.8% month-over-month from December 2017. Since the country has very little mining sector to speak of, and Japan’s IP doesn’t include utility output, this was entirely manufacturing in nature (99.79% of the IP index is derived from the manufacturing...

Read More »

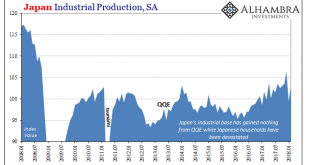

Jeffrey P. Snider

February 16, 2018

SNB & CHF

The conventional interpretation of “reflation” in the second half of 2016 was that it was simply the opening act, the first step in the long-awaiting global recovery. That is what reflation technically means as distinct from recovery; something falls off, and to get back on track first there has to be acceleration to make up that lost difference.

There was, to me anyway, a lot of Japan in it, even still if “globally...

Read More »

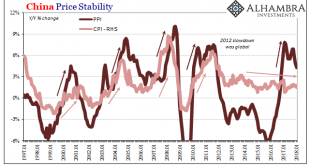

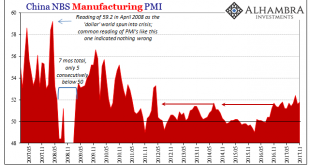

Jeffrey P. Snider

December 13, 2017

SNB & CHF

China’s National Bureau of Statistics reported last week that the official manufacturing PMI for that country rose from 51.6 in October to 51.8 in November. Since “analysts” were expecting 51.4 (Reuters poll of Economists) it was taken as a positive sign. The same was largely true for the official non-manufacturing PMI, rising like its counterpart here from 54.3 the month prior to 54.8 last month.

China Manufacturing...

Read More »

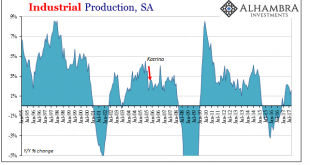

Jeffrey P. Snider

October 20, 2017

SNB & CHF

Industrial Production rose 1.6% year-over-year in September 2017. That’s up from 1.2% growth in August, both months perhaps affected to some degree by hurricanes. The lack of growth and momentum, however, clearly predated the storms. The seasonally-adjusted index for IP peaked in April 2017, and has been lower ever since. This pattern, the disappointment this year is one we see replicated nearly everywhere on both sides...

Read More »

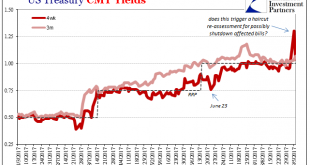

Jeffrey P. Snider

September 30, 2017

SNB & CHF

Eleven days ago, we asked a question about Treasury bills and haircuts. Specifically, we wanted to know if the spike in the 4-week bill’s equivalent yield was enough to trigger haircut adjustments, and therefore disrupt the collateral chain downstream.

US Treasury, Jan - Sep 2017(see more posts on U.S. Treasuries, ) - Click to enlarge

Within two days of that move in bills, the GC market for UST 10s had gone...

Read More »

Jeffrey P. Snider

September 7, 2017

SNB & CHF

The payroll report for August 2017 thoroughly disappointed. The monthly change for the headline Establishment Survey was just +156k. The BLS also revised lower the headline estimate in each of the previous two months, estimating for July a gain of only +189k. The 6-month average, which matters more given the noisiness of the statistic, is just +160k or about the same as when the Federal Reserve contemplated starting a...

Read More »

Jeffrey P. Snider

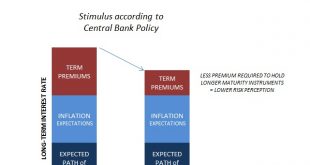

September 1, 2017

SNB & CHF

According to orthodox theory, if interest rates are falling because of term premiums then that equates to stimulus. Term premiums are what economists have invented so as to undertake Fisherian decomposition of interest rates (so that they can try to understand the bond market; as you might guess it doesn’t work any better). It is, they claim, the additional premium a bond investor demands so as to hold a security that...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org