Frederik Ducrozet

October 5, 2016

Perspectives Pictet

Tapering is not an immediate issue for the ECB, which we believe is much more likely to announce an extension of QE and measures to deal with the scarcity of bonds it can purchase. Spokespersons for the ECB have been anxious to beat back a Bloomberg story that the bank was attempting to “build a consensus” around the tapering of its bond purchases, saying the Governing Council (GC) had not even discussed this issue at its last policy meeting in September.The timing of the story is a...

Read More »

Luc Luyet

October 4, 2016

Perspectives Pictet

Central bank stance supports AUD in the short term, but a number of factors should weigh on currency over coming year. At its 4 October monetary policy meeting, the Reserve Bank of Australia (RBA) left monetary policy stance broadly unchanged, with the cash rate remaining at 1.50%. This was the first monetary policy meeting under the RBA’s new governor, Philip Lowe.The broadly unchanged statement the RBA released at the end of its meeting suggested that the central bank is in no hurry to...

Read More »

Dong Chen

October 3, 2016

Perspectives Pictet

Recent data points to possibility of upside surprise in third-quarter GDP, but momentum may not last. September purchasing manager indices (PMIs) provided the latest evidence pointing to relatively strong Q3 GDP growth in China (the GDP report will be released later this month). However, we believe the structural downward trend in Chinese growth will resume as property investment loses momentum and the government continues to cut industrial overcapacity.China’s official manufacturing PMI...

Read More »

Bernard Lambert

September 30, 2016

Perspectives Pictet

Data released on 30 September continued to tally with our forecast of 1.5% GDP growth in the US for 2016 and a slow rise in core inflation to 1.9%. According to the Bureau of Economic Analysis (BEA), real consumer spending in the US fell 0.1% m-o-m in August, below consensus expectations. However, the figure for July was left unchanged, so that between Q2 and July-August, US personal consumption grew by 2.9% annualised.Other US data published in recent days has been mixed. Pending home...

Read More »

Frederik Ducrozet and Nadia Gharbi

September 30, 2016

Perspectives Pictet

Macroview Headline inflation in the euro area doubled in September as the impact of weaker energy prices declined, but core inflation was stable. As expected, euro area flash HICP inflation rose to 0.4% year on year (y-o-y) in September, from 0.2% in August as the impact of weak energy prices continued to fade. But measures of core inflation were slightly weaker than expected, remaining stable at 0.8% y-o-y against expectations of a small rise.Weaker industrial goods inflation in particular...

Read More »

Frederik Ducrozet and Nadia Gharbi

September 27, 2016

Perspectives Pictet

Macroview Credit flows to households and corporations slackened in August, so domestic demand may be less of a factor in near-term growth. But we are sticking to our full-year growth forecast for the euro area. Credit to euro area households increased in August. Although at a slower pace than the previous month, August was the 23th straight month of positive credit flows. By contrast, bank credit to euro area non-financial corporations (NFCs) declined by EUR1 bn in August (adjusted for sales...

Read More »

Luc Luyet

September 26, 2016

Perspectives Pictet

While gold prices may not fall back to their end-2015 levels, there are few compelling reasons for a fresh acceleration in the near term. After a strong performance in the first half of this year, gold has been moving within a range of USD1300- USD1375 per troy ounce. While physical supply and demand favour a gradual rise in gold prices over time, some of the main drivers of investment demand (financial stress, inflation, real interest rates, the USD) do not suggest significant upside...

Read More »

Frederik Ducrozet and Nadia Gharbi

September 23, 2016

Perspectives Pictet

Macroview September Flash PMIs were a mixed bag, but a closer look provides grounds for optimism. Markit’s euro area flash PMI indices for September were mixed, with France outperforming but business confidence declining in the German services sector as well as in the rest of the currency union. However, details of the PMI readings were generally better than the headlines. New orders rose in September and labour market dynamics remained supportive. Perhaps the best news from the Markit PMIs...

Read More »

Bernard Lambert

September 22, 2016

Perspectives Pictet

While the Fed stood pat at its September meeting, we continue to expect one quarter-point rise in rates this year, and two more in 2017. The Federal Open Market Committee (FOMC) left interest rates unchanged at the end of its latest policy meeting on September 21. However, the Fed adopted a more hawkish tone, reintroduced in its statement a sentence saying risks in the US economy were roughly balanced, and affirmed that the case for a rate hike has strengthened. Significantly, three voting...

Read More »

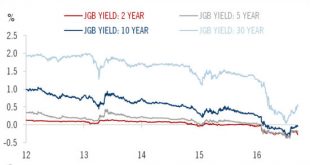

Dong Chen and Luc Luyet and Jacques Henry

September 21, 2016

Perspectives Pictet

While possibly helping to alleviate margin pressure on banks, raising inflation expectations remains a difficult task The Bank of Japan (BoJ) today shifted its monetary stimulus framework towards yield-curve control and away from rigid targeting of asset purchases. In essence, the BoJ will purchase sufficient Japanese government bonds (JGBs) to ensure that 10-year JGB yields are capped at about zero. The BOJ also announced that it aims to overshoot its 2% inflation target, committing itself...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org