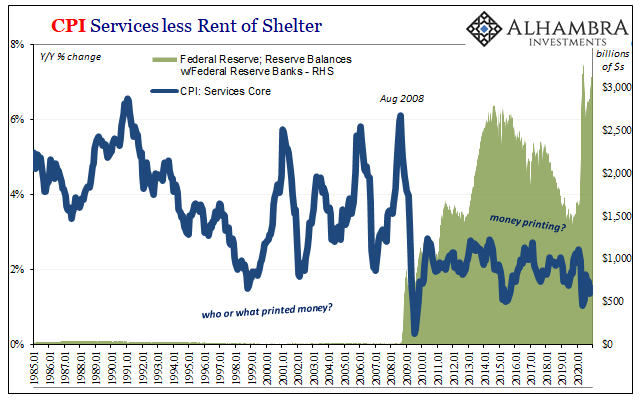

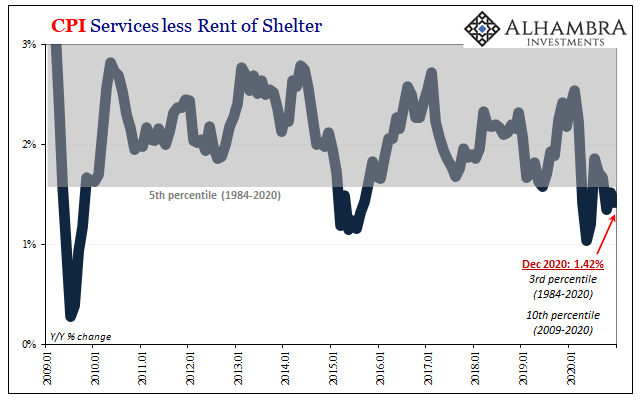

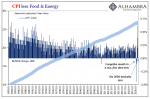

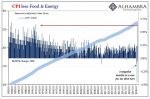

It’s not just that there isn’t much inflation evident in consumer prices. Rather, it’s a pretty big deal given the deluge of so much “money printing” this year, begun three-quarters of a year before, that consumer prices are increasing at some of the slowest rates in the data. Trillions in bank reserves, sure, but actual money can only be missing. U.S. CPI Services Core Fed, Jan 1985 - -2020 - Click to enlarge U.S. CPI Services Core percentile, Jan 2009 - 2020 - Click to enlarge OK, fine. What about commodities? If the Fed’s monetary fires haven’t fed through to corporate pricing power for the stuff going out the door, then perhaps it just hasn’t gotten that far yet. Given the huge move in especially industrial metals (and others) led by Dr. Copper,

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, commodities, Consumer Prices, Copper, CPI, currencies, Dollar, economy, Featured, Federal Reserve/Monetary Policy, inflation, jay powell, Markets, Metals, money printing, newsletter, PPI, producer prices, QE

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| It’s not just that there isn’t much inflation evident in consumer prices. Rather, it’s a pretty big deal given the deluge of so much “money printing” this year, begun three-quarters of a year before, that consumer prices are increasing at some of the slowest rates in the data. Trillions in bank reserves, sure, but actual money can only be missing. |

U.S. CPI Services Core Fed, Jan 1985 - -2020 - Click to enlarge |

U.S. CPI Services Core percentile, Jan 2009 - 2020 - Click to enlarge |

|

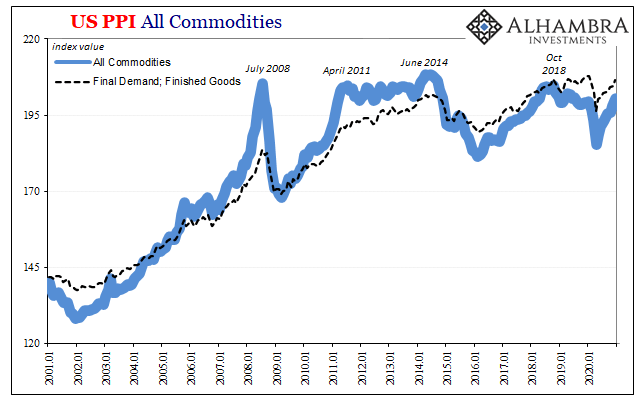

| OK, fine. What about commodities? If the Fed’s monetary fires haven’t fed through to corporate pricing power for the stuff going out the door, then perhaps it just hasn’t gotten that far yet. Given the huge move in especially industrial metals (and others) led by Dr. Copper, though companies aren’t raising prices on the goods (and services) they’re sending out maybe that’s just because they haven’t yet passed along the rapidly rising prices of the materials coming in.

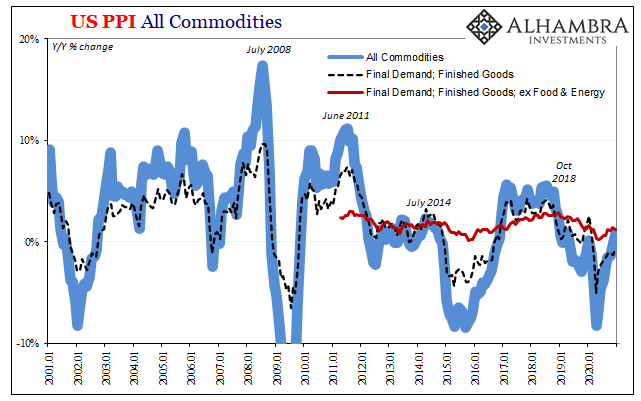

Cost-push. After all, it would stand to reason that if commodities are on their way up – for inflationary reasons of imminent currency “devaluation” – we should be able to see it by now at least in the form of widespread producer price inflation. |

Copper Futures, Continuous Front Month, Jan 2002 - 2021 - Click to enlarge |

| And if so, that would have to eventually feed through to what consumers end up paying, too.

It’s not here, either. Though commodity prices are absolutely rising and have made a pretty substantial move, so far it has been limited to just those as serious pricing pressures have yet to materialize in any other input prices around both the goods and services sector. The BLS’s PPI is rebounding and is moving higher along with copper and its metal mates, even after nine months (through December) the increase – more importantly the rate of increase – isn’t the kind you’d associate with even modest inflation let alone the first obvious stages indicating soon to be out-of-control prices driven by unbelievable monetary excess. In fact, like consumer prices in the CPI and PCE Deflator, finished goods commodity prices (excluding food and energy) in the PPI have decelerated quickly over the final three months of 2020 (up just 0.2% during Q4 as a whole). The same three months that retail sales have declined, jobless claims have picked up, and at least one month of headline payroll negative. Most of the increase in overall producer prices during December had been driven by gasoline. The fact that industrial metal prices have continued to rise, copper setting another multi-year high recently, suggests more of its own fundamental properties like supply – including those linked to China, rather than anything of US inflationary currency. |

U.S. PPI, Jan 2001 - 2020 - Click to enlarge |

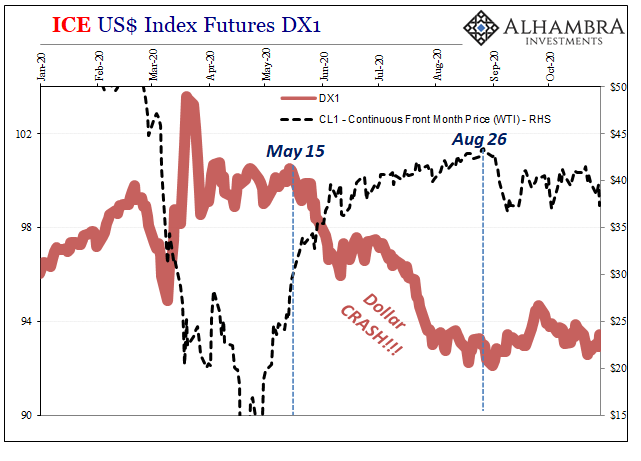

| In other words, the PPI is consistent with the CPI as well as metals prices rising rapidly due to supply not currency factors (short and long run). So far as the Fed killing the dollar, spiking the inflationary collapse in it, like bond yields that haven’t moved all that much or even the dollar’s exchange value itself (outside EUR and GPB), why haven’t these prices/indices moved so much more than they have?

The metals, like oil, we can account for on physical factors. The rest of the system, both in and out, it’s the same disinflationary. Inflation, uncontrolled and otherwise, is not a small group of prices or a narrow sector of asset classes experiencing even large increases. |

U.S. PPI Index Commodities Finished Goods, Jan 2001 - 2020 - Click to enlarge |

| It’s when everything, or nearly everything, goes up at the same time and in a sustained fashion.

What we see here, which is only slightly less worrisome than the historically low consumer price increases, is the same limited, constrained rebound from the latest trough. That it isn’t anything more than this is another tally on the lengthening list of evidence against Jay’s “flood.” |

Federal Reserver: H.10 Foreign Exchange Rates, Jan 2008 - 2021 - Click to enlarge |

Episode 41; Part 2: Professor Copper’s Got Other Courses To Teach

You Might Also Like

Where Is It, Chairman Powell?

Where Is It, Chairman Powell?

2020-11-15

Where is it, Chairman Powell? After spending months deliberately hyping a “flood” of digital money printing, and then unleashing average inflation targeting making Americans believe the central bank will be wickedly irresponsible when it comes to consumer prices, the evidence portrays a very different set of circumstance.

Fama 2: No Inflation For Old Central Banks

Fama 2: No Inflation For Old Central Banks

2020-08-14

The Bureau of Labor Statistics reported that the core CPI in July 2020 jumped by the most (+0.62%) in almost thirty years. After having dropped month-over-month for three months in a row for the first time in its history, it has posted back to back gains the latest of which pushing the index back above its February level.

What’s Going On, And Why Late August?

What’s Going On, And Why Late August?

2020-10-29

This isn’t about COVID. It’s been building since the end of August, a shift in mood, perception, and reality that began turning things several months before even then. With markets fickle yet again, a lot today, what’s going on here?

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

2020-10-02

It’s always something. There’s forever some mystery factor standing in the way. On the topic of inflation, for years it was one “transitory” issue after another. The media, on behalf of the central bankers it holds up as a technocratic ideal, would report these at face value. The more obvious explanation, the argument with all the evidence, just couldn’t be true otherwise it’d collapse the technocracy right down to the ground.And so it was also in the bond market. Inflation and their yields very much related, the lack of the former wasn’t ever used to explain the curious absence of the BOND ROUT!!! No, the US Treasury market has been beset by its own set of “transitory” factors, too. As ridiculous as some of the inflation excuses had been, Verizon’s unlimited wireless data plans the

Part 2 of June TIC: The Dollar Why

Part 2 of June TIC: The Dollar Why

2020-08-21

Before getting into the why of the dollar’s stubbornly high exchange value in the face of so much “money printing”, we need to first go back and undertake a decent enough review of the guts maybe even the central focus of the global (euro)dollar system.

Not This Again: Too Many Treasuries?

Not This Again: Too Many Treasuries?

2020-08-27

Tomorrow, the Treasury Department is going to announce the results of its latest bond auction. A truly massive one, $47 billion are being offered of CAH4’s notes dated August 31, 2020, maturing out in August 31, 2027. In other words, the belly of the belly, the 7s.We’ve already seen them drop for two note auctions this week, both equally sizable.

This Has To Be A Joke, Because If It’s Not…

This Has To Be A Joke, Because If It’s Not…

2020-08-28

After thinking about it all day, I’m still not quite sure this isn’t a joke; a high-brow commitment of utterly brilliant performance art, the kind of Four-D masterpiece of hilarious deception that Andy Kaufman would’ve gone nuts over. I mean, it has to be, right?I’m talking, of course, about Jackson Hole and Jay Powell’s reportedly genius masterstroke.

Deflation Returns To Japan, Part 2

Deflation Returns To Japan, Part 2

2020-11-23

Japan Finance Minister Taro Aso, who is also Deputy Prime Minister, caused a global stir of sorts back in early June when he appeared to express something like Japanese racial superiority at least with respect to how that country was handling the COVID pandemic.

Tags: commodities,Consumer Prices,Copper,CPI,currencies,dollar,economy,Featured,Federal Reserve/Monetary Policy,inflation,jay powell,Markets,Metals,money printing,newsletter,PPI,producer prices,QE