AMERICA’S MAIN financial regulator is taking an interest in climate change—and wants everyone to know. The Securities and Exchange Commission (SEC) has created a task-force to examine environmental, social and governance (ESG) issues, appointed a climate tsar and said it will “enhance its focus” on climate-related disclosures for listed firms. It looks poised to introduce, among other things, rules forcing firms to reveal how climate change or efforts to fight it may affect their business. Since September regulators in Britain, New Zealand and Switzerland have said they plan to make such climate-related disclosures mandatory. So, too, have stock exchanges in Hong Kong, London and South Korea. The EU may follow suit. The flurry of rulemaking stems from a concern

Topics:

Business considers the following as important: 3.) Global News on Switzerland, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The flurry of rulemaking stems from a concern that climate change poses a threat to financial stability. Whether this is true or not is hard to say. The data are shoddy and climate-risk reporting is largely voluntary. Firms tend to cherry-pick the most flattering numbers and methodologies. The reporting seldom reveals anything about a firm’s risk in the future—which is where the financial threats from climate change mostly reside.

Many watchdogs are pinning their hopes on the Task Force on Climate-Related Financial Disclosures (TCFD), set up in 2015 by the Financial Stability Board (FSB), a global group of regulators. The TCFD has recommended a reporting standard made up of 11 broad categories, from carbon footprints to climate-risk management. Regulators like it because it focuses on material risks rather than environmental impacts, and because it asks for information about firms’ future plans. That includes “scenario analysis”, in which a company’s strategy is tested against potential futures, such as a hotter world or higher carbon prices.

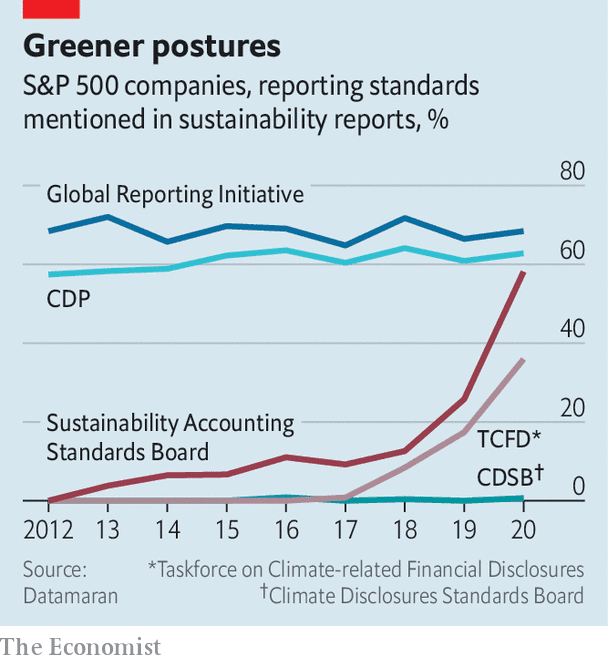

| These qualities also appeal to financiers. Financial firms make up almost half of the 1,800 or so companies that back the TCFD‘s recommendations. Together they hold assets worth over $150trn and include the world’s ten biggest asset managers and eight of its ten biggest banks. Their clients and regulators are egging them on to adopt the standard, so the financial firms in turn are prodding companies to do so, too, causing an uptick in its use (see chart).

Not all companies are happy about this. It means compliance with one more ESG measure, and a tricky one at that. Many bosses claim their firms lack the expertise to do climate-based scenario analysis (the TCFD’s recent 133-page how-to guide may help). Only 7% of big firms disclose such exercises, according to a review of 1,700-odd companies by the TCFD. Those that do often use different scenarios, making their efforts hard to compare . Another problem is that disclosures may scare off investors. This, of course, is the point. But until reporting is mandatory for everyone, firms risk being punished for being early adopters. That is the evidence from France, which made climate-risk disclosures obligatory for asset managers, insurers and pension funds in 2016. A study by its central bank compared those firms with French banks and non-French financial firms. It found that the firms which had to disclose climate risks held 40% fewer bonds, stocks and other securities in fossil-fuel firms by value than those that did not have to disclose risks. |

Greener postures - Click to enlarge |

Such a shift may drive up capital costs for polluting projects and lead to fewer emissions. But more climate disclosure will not by itself cut carbon, notes Remco Fischer of the UN Environment Programme. Regulatory climate risk can, in theory, be mitigated by moving carbon-heavy assets somewhere with laxer environmental rules. And sophisticated risk assessments do not always result in decarbonisation. Last year AGL Energy, an Australian utility, published an analysis of scenarios. The one it has chosen to follow involves keeping one of its coal-fired power stations open until 2048. ■

For more coverage of climate change, register for The Climate Issue, our fortnightly newsletter, or visit our climate-change hub

This article appeared in the Business section of the print edition under the headline “Telling all”

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-03-15

Update March 15 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

Swiss Voters Approve ‘Burqa Ban’

Swiss Voters Approve ‘Burqa Ban’

2021-03-13

Swiss voters have narrowly approved a proposal to ban face coverings in public spaces. The measure comes just over a decade after citizens voted to ban the construction of minarets, the tower-like structures on mosques that are often used to call Muslims to prayer.

Swiss To Vote In Referendum On Government’s Emergency COVID-19 Measures

Swiss To Vote In Referendum On Government’s Emergency COVID-19 Measures

2021-02-25

Via 21stCenturyWire.com,After mounting a national campaign, and the work of determined local organisations, Swiss campaigners have managed to trigger a referendum for ending the government’s destructive COVID regulations.

The Death Of Logic

The Death Of Logic

2021-02-24

Authored by Matthew Piepenburg via GoldSwitzerland.com,Just over four years ago, as Bitcoin was making its first big moves in both price and public perception, John Hussman of Hussman Investment Trust penned a lengthy as well as seminal report entitled, “Three Delusions: Paper Wealth, a Booming Economy, and Bitcoin.

Unhappy Endings: Deception Has Gone Global

Unhappy Endings: Deception Has Gone Global

2021-02-16

Looking Behind the LabelsRegardless of one’s politics, most would agree that extremely complex issues are typically given extremely misleading titles.Not all those of the extreme left, for example, are all that “woke” and not everyone on the far right, to be fair, is a “domestic terrorist.

Second Covid Wave in Europe, Rest of the World still Unaffected

Second Covid Wave in Europe, Rest of the World still Unaffected

2020-10-21

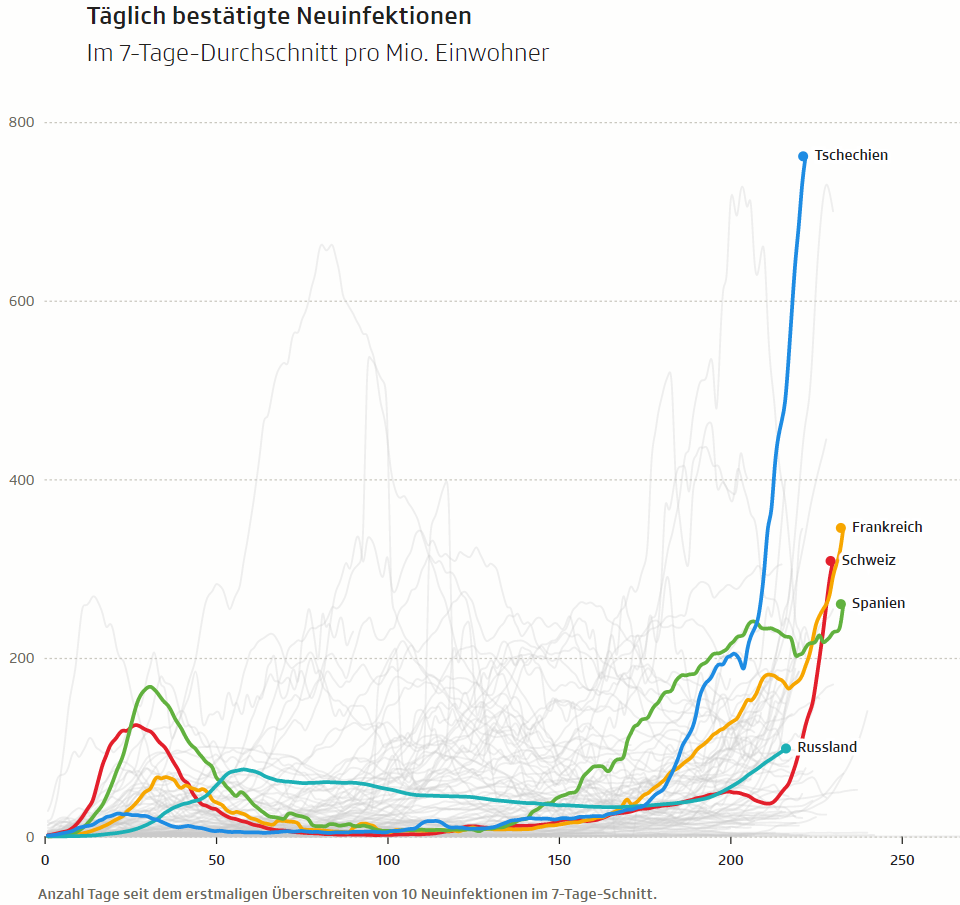

The second wave of the Coronavirus is currently raging in Europe. The attached image shows the number of newly infected people in European countries on a linear scale. In particular in the Czech republic, but also in Switzerland, France or Spain, one can see a tendency of exponential growth.

Aktualisierte Sanktionsmeldung

Aktualisierte Sanktionsmeldung

2020-10-16

Das Eidgenössische Departement für Wirtschaft, Bildung und Forschung WBF hat eine Änderung des Anhangs 3 der Verordnung vom 27. August 2014 über Massnahmen zur Vermeidung der Umgehung internationaler Sanktionen im Zusammenhang mit der Situation in der Ukraine (SR 946.231.176.72) publiziert.

Swiss return frozen CHF36 million to South American football federation

Swiss return frozen CHF36 million to South American football federation

2020-10-16

Swiss authorities have returned about CHF36.6 million ($40 million) in funds frozen in Swiss bank accounts amid football corruption investigations into the South American football confederation CONMEBOL.

Tags: Featured,newsletter