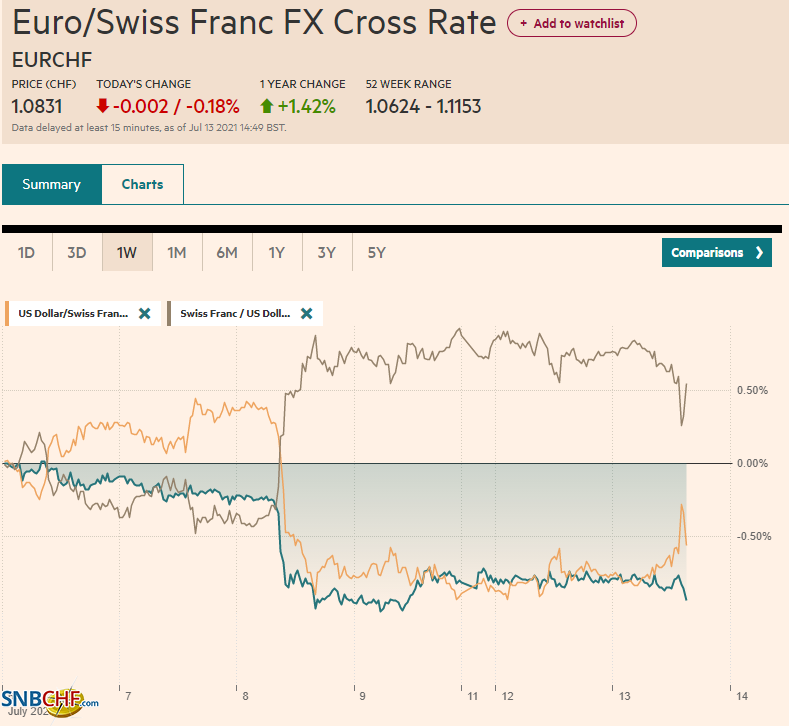

Swiss Franc The Euro has fallen by 0.18% to 1.0831 EUR/CHF and USD/CHF, July 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: New record highs in the US S&P 500 and NASDAQ coupled with China allowing Tencent to acquire a search engine helped lift Asia Pacific equities. It is the first back-to-back by MSCI’s regional index for more than two weeks. Australia’s market was a notable exception. The lockdown in Sydney is weighed on new confidence measures and prompts economists to cut growth forecasts for Q3. European equities are softer. Weakness in health care and utilities is offsetting the gains in information technology and materials. US futures are slightly lower as well. The US 10-year Treasury yield is

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Canada, Chile, China, Currency Movement, Featured, newsletter, Nord Stream 2, RBNZ, tax reform, trade, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.18% to 1.0831 |

EUR/CHF and USD/CHF, July 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: New record highs in the US S&P 500 and NASDAQ coupled with China allowing Tencent to acquire a search engine helped lift Asia Pacific equities. It is the first back-to-back by MSCI’s regional index for more than two weeks. Australia’s market was a notable exception. The lockdown in Sydney is weighed on new confidence measures and prompts economists to cut growth forecasts for Q3. European equities are softer. Weakness in health care and utilities is offsetting the gains in information technology and materials. US futures are slightly lower as well. The US 10-year Treasury yield is little changed near 1.36%. European yields are marginally lower, while China’s 10-year bond yield of 2.92% is a new three-month low. Only the yen and Australian dollar are posting minor gains against the greenback. The other major currencies are slightly lower, though the Norwegian krone is off 0.3%. Emerging market currencies are mixed, with social unrest continuing to weigh on the South African rand. It fell by 1.3% yesterday and is off another 1.2% today. The Russian ruble leads the advancers ahead of tomorrow’s CPI, which is expected to set the stage for a potentially large rate hike next week. The JP Morgan Emerging Market Currency Index is giving back most of yesterday’s 0.2% gain. Gold is holding above $1800 for the first session since June 16. August WTI is firm but sitting on the $74-handle, inside yesterday’s range. Iron ore rose 2%, while copper is softer pinned near yesterday’s low (~$429). September lumber posted an outside down day, falling for the fourth consecutive session. Yesterday’s 5.5% drop brings the four-day slide to a cumulative 14% decline. The US Department of Agriculture cut its projection of the soy, oat, and wheat harvests while boosting corn. The CRB Index rose for the third consecutive session yesterday. |

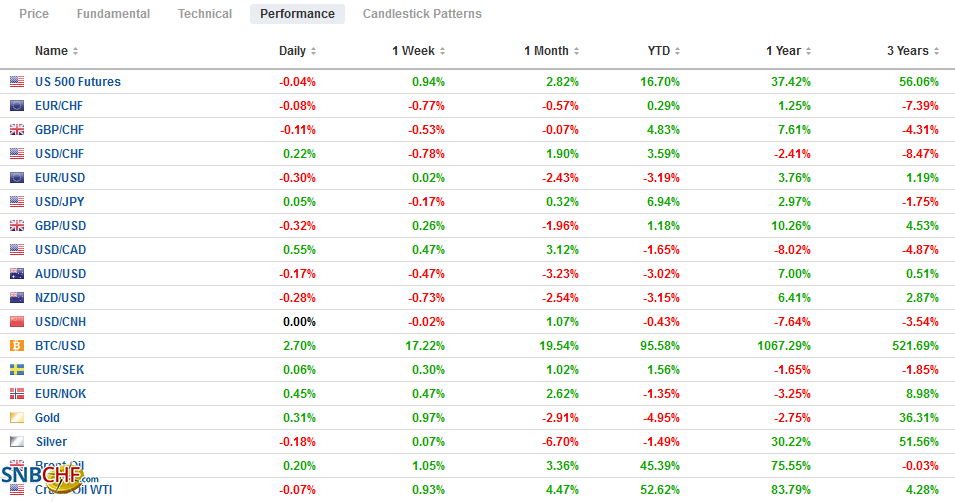

FX Performance, July 13 - Click to enlarge |

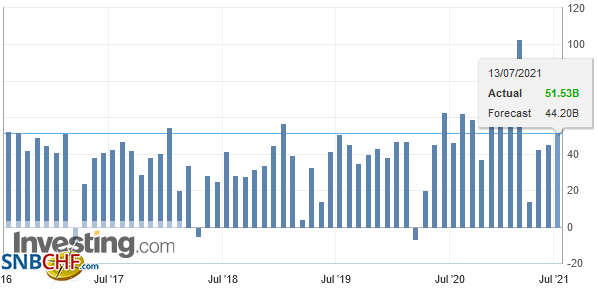

ChinaBooming exports helped to unexpectedly lift China’s June trade surplus by over 13% to $51.53 bln, the most since January. China’s monthly trade surplus averaged $42.5 bln in H1 21, and $27.4 bln in H1 20, and $29.4 bln in H1 19. Exports, which economists had projected to fall, accelerated to 32.2% year-over-year from 27.9% in May. Imports held in better than economists had expected, falling to 36.7% from 51.1%. Export growth to the US slowed (17.8% year-over-year) while the trade surplus widened to $32.6 bln. Exports to East Asia accelerated. Beijing will report Q2 GDP early Thursday, and today’s trade figures seem to limit the risk of a downside surprise, which last week’s unexpected cut in reserve requirements had fanned fears of. |

China Trade Balance, June 2021(see more posts on China Trade Balance, ) Source: Investing.com - Click to enlarge |

Asia Pacific

The Reserve Bank of New Zealand meets first thing tomorrow in Wellington. While the cash target will most likely remain at 25 bp, sentiment has turned hawkish over the last couple of weeks, and the RBNZ statement is being anticipated to validate the shift. The market has discounted roughly 20 bp of tightening in the next six months. In the middle of June, only two basis points of tightening were priced into the money market. Ahead of the weekend, New Zealand will report Q2 CPI. The year-over-year pace is expected to accelerate to 2.7% from 1.5% in Q1.

The dollar has thus far been confined to about a 15-tick range against the Japanese yen above JPY110.30, where a $575 mln option expires today. Nearby resistance is seen near JPY110.60, which corresponds to the 20-day moving average and the (50%) retracement of the drop since the July 2 high near JPY111.65. A break of JPY110.00 sours the tone.

The Australian dollar briefly traded above $0.7500 for the first time in four sessions. There is little conviction ahead of Thursday’s employment report, and the spike in covid cases is dampening the near-term economic outlook. Support is seen near $0.7450. The New Zealand dollar is consolidating after losing about 0.25% yesterday.

We had expressed concern that if Chinese officials are wary of a one-way market, they had helped facilitate a six-week slide in the yuan. As a result, they replaced one one-way market with another in the opposite direction. However, with today’s gains, the yuan rose for the third consecutive session. The price action reinforces the CNY6.49 area as the upper end of the new range for the dollar. The PBOC set the dollar’s reference rate at CNY6.4757. The median projection in Bloomberg’s survey was for CNY6.4747, leaving the fix a little rich to expectations.

GermanyAhead of German Chancellor Merkel’s meeting in the US with President Biden later this week, two concessions were made that seem to help create a more constructive atmosphere. First, after some hesitancy, the EU indicated it would hold off with the digital tax, which both the Trump and Biden administrations argued was aimed at US companies, pending progress on international coordinated efforts. However, despite the G20 finance ministers’ and central bankers’ endorsement, it remains far from a done deal. First, the US Senate would need to ratify the tax revenue sharing agreement (treaty), which does not appear particularly likely. Also, tax issues require unanimity in the EU, and Ireland, Hungary, and Estonia are balking above the 15% minimum tax. Second, the Nord Stream 2 pipeline, which is nearly completed, is also a bone of contention with the Americans. Yesterday, Merkel committed Europea to do everything to ensure that gas supplies continue to flow through Ukraine and warned Russia against using the pipeline for political leverage. |

Germany Consumer Price Index (CPI) YoY, June 2021(see more posts on Germany Consumer Price Index, ) Source: Investing.com - Click to enlarge |

In the UK, parliament is expected to vote shortly on the government’s decision to cut funding for its official development assistance from 0.7% of gross national income to 0.5%. Although the figure appears in the Tory Party’s manifesto, it was jettisoned by the government to save about GBP4 bln. The international wing of the Tories, which includes former Prime Minister May, is opposed. The vote will be on a statement from the Chancellor of the Exchequer Sunak that the 0.7% target will be restored if the Office for Budget Responsibility confirmed spending is under control and the underlying debt is falling. The net effect would likely limit the international assistance to 0.5% for the next several years.

The euro remains in the range seen last Friday, roughly $1.1825 to $1.1880. There is an option for around 600 mln euros at $1.1875 that expires today and one for about 660 mln euros that expires tomorrow at $1.1810. ECB President Lagarde’s comment that plays up fresh, forward guidance at next week’s central bank meeting and a threat to continue limiting bank dividends may have sapped any near-term enthusiasm for the single currency.

For the third consecutive session, sterling has found offers waiting when it pokes above $1.3900. It is barely holding above yesterday’s low, near $1.3840. Last week’s low is another cent down. The UK reports June CPI figures tomorrow, followed by the May/June employment data on Thursday.

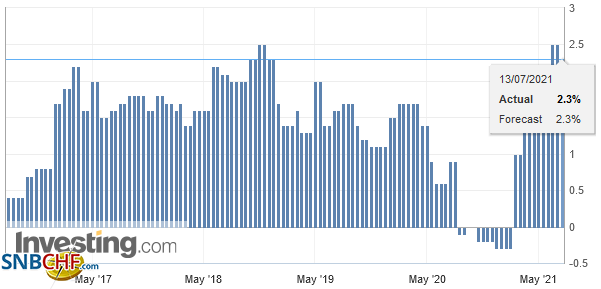

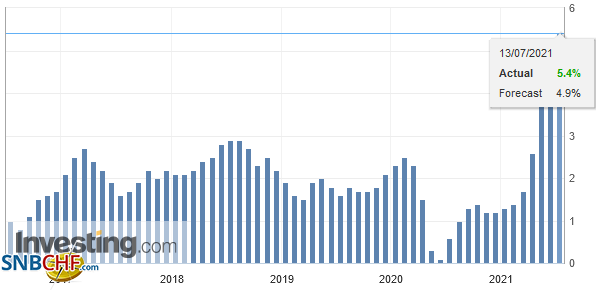

United StatesThe US reports June CPI figures today. It could be the first slippage in the year-over-year headline rate since last May. A 0.5% month-over-month gain could produce a 4.9% year-over-year pace, down from 5.0% in May. |

U.S. Consumer Price Index (CPI) YoY, June 2021(see more posts on U.S. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

| The core rate, which excludes food and energy, may tick up to 4.0% from 3.8%. We don’t expect it to impact expectations that the Federal Reserve will announce its tapering plans at the end of August (Jackson Hole) or the September FOMC meeting (September 22). Separately, US earnings season kicks off with JP Morgan, and Goldman Sachs reports today. |

U.S. Core Consumer Price Index (CPI) YoY, June 2021(see more posts on U.S. Core Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Ahead of the Bank of Canada’s meeting tomorrow, Carolyn Rogers was named Senior Deputy Governor, filling the void left by Carolyn Wilkins who stepped down in December 2020, seemingly after not being chosen as the next Governor. Rogers currently is the Secretary-General of the Basel Committee on Banking Supervision and has experience as the Assistant Superintendent in the Office of the Superintendent of Financial Institutions. Her appointment, however, is not effective until the middle of December.

The US dollar has formed a near-term base near CAD1.2440. It briefly traded to almost CAD1.2515 yesterday and has held below CAD1.2485 so far today but is near session highs near midday in Europe. The intraday momentum indicators are stretched, suggesting the scope for only limited gains in early North American turnover.

Mexico and Brazil have light economic diaries today. The greenback eased slightly against the peso yesterday and is firmer today, around MXM19.91. Yesterday, it traded a little through MXN20.01 before coming off. The dollar snapped an eight-session rally against the Brazilian real yesterday. During the advance, the greenback rose by almost 7%. It fell 1.6% yesterday. The dollar posted an outside down day against the Chilean peso yesterday. It was the second consecutive decline after a four-day advance. The central bank meets late tomorrow and is widely expected to hike its overnight target rate by 25 bp to 0.75%.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 12: Markets Adrift ahead of Key Events

FX Daily, July 12: Markets Adrift ahead of Key Events

2021-07-12

The new week has begun quietly. The dollar is drifting a little higher against most major currencies, with the Scandis and dollar-bloc currencies the heaviest. The yen and Swiss franc’s resilience seen last week is carrying over.

SNB Sight Deposits: Inflation Fear Decreasing, SNB Selling Euros

SNB Sight Deposits: Inflation Fear Decreasing, SNB Selling Euros

2021-07-12

Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

FX Daily, July 09: PBOC Cuts Reserve Requirements after Inflation Measures Ease

FX Daily, July 09: PBOC Cuts Reserve Requirements after Inflation Measures Ease

2021-07-09

The capital markets are winding down what has been a challenging week that has seen equity markets slide and the dollar and bonds rally. The MSCI Asia Pacific fell for the fourth consecutive session, but the more interesting story may be the intrasession recovery that could set the stage for a better performance next week.

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

2021-06-10

The ECB meeting and the US May CPI report is at hand. The US dollar is consolidating at a higher level against most of the major currencies. Softer than expected, inflation readings are weighing on the Scandis, which are bearing the brunt. The US 10-year yield closed below 1.50% for the first time in three months yesterday, and this may have helped underpin the Japanese yen.

FX Daily, April 26: Big Week Begins Quietly, with the Greenback Still Under Pressure

FX Daily, April 26: Big Week Begins Quietly, with the Greenback Still Under Pressure

2021-04-26

Overview: What promises to be a notable week has begun off quietly: the US, EMU, and South Korea report Q1 GDP. The eurozone also provides its first estimate of April inflation. Corporate earnings feature tech and financial firms. Equities are mostly firmer in the Asia Pacific region and Europe.

FX Daily, February 23: Dramatic Market Adjustment Continues

FX Daily, February 23: Dramatic Market Adjustment Continues

2021-02-23

Overview: Rising rates continue to spur a rotation and retreat in stocks. Yesterday the NASDAQ sold-off by nearly 2.5% while the Dow Industrials eked out a minor gain. Equities are mostly higher in the Asia Pacific region while Japanese markets were on holiday.

FX Daily, January 20: The Dollar Slips to New Lows against Sterling and the Mexican Peso

FX Daily, January 20: The Dollar Slips to New Lows against Sterling and the Mexican Peso

2021-01-20

Global equities are moving higher today. Led by continued strong buying of Hong Kong shares, the MSCI Asia Pacific Index rose to new highs. The Hang Seng is up 6% this year and is approaching the 2019 record high. Australia’s shares set a new record today. Japan and Taiwan bucked the trend.

FX Daily, January 18: US is on Holiday, but the Dollar has Legs

FX Daily, January 18: US is on Holiday, but the Dollar has Legs

2021-01-18

Overview: The new week has begun like last week ended. Equities are a bit heavy. The MSCI Asia Pacific Index fell for the second session, its first back-to-back loss since before Christmas. China and Hong Kong were the notable exceptions, perhaps helped by stronger than expected GDP.

Tags: #USD,Canada,Chile,China,Currency Movement,Featured,newsletter,Nord Stream 2,RBNZ,tax reform,Trade,U.K.