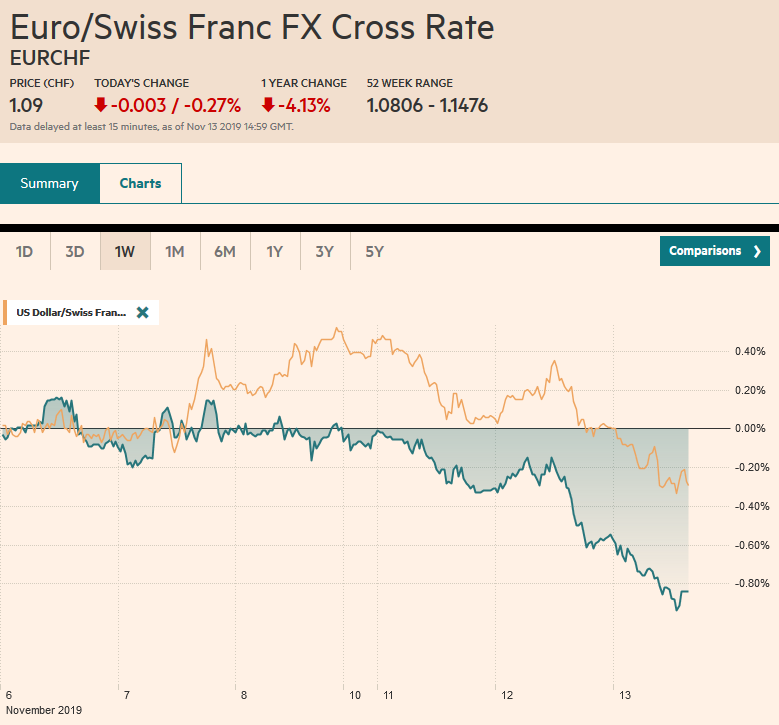

Swiss Franc The Euro has fallen by 0.27% to 1.09 EUR/CHF and USD/CHF, November 13(see more posts on EUR/CHF, USD/CHF, ) Source: market.ft.com - Click to enlarge FX Rates Overview: The recent rise in equity markets and backing up in yields spurred many observers to upgrade their macroeconomic outlooks rather than the other way around. Yet we continue to see may worrisome signs. It is not just trade, though, of course, that is part of it. Sentiment itself is fragile and will likely follow prices. Led by Hong Kong, where the confrontation is intensifying, and the Hang Seng’s 1.8% drop, regional markets tumbled. The MSCI Asia Pacific Index fell for the third time in four sessions. In Europe, shares are also moving lower. The Dow Jones Stoxx 600 is off by around

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Currency Movement, EUR/CHF, Eurozone Industrial Production, Featured, Federal Reserve, FX Daily, New Zealand, newsletter, U.S. Consumer Price index, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.27% to 1.09 |

EUR/CHF and USD/CHF, November 13(see more posts on EUR/CHF, USD/CHF, ) Source: market.ft.com - Click to enlarge |

FX RatesOverview: The recent rise in equity markets and backing up in yields spurred many observers to upgrade their macroeconomic outlooks rather than the other way around. Yet we continue to see may worrisome signs. It is not just trade, though, of course, that is part of it. Sentiment itself is fragile and will likely follow prices. Led by Hong Kong, where the confrontation is intensifying, and the Hang Seng’s 1.8% drop, regional markets tumbled. The MSCI Asia Pacific Index fell for the third time in four sessions. In Europe, shares are also moving lower. The Dow Jones Stoxx 600 is off by around 0.6% in the morning session, which, if sustained, would be the largest loss in a month. Financials and energy are the largest drags. US shares are trading lower, and a decline today by the S&P 500 would be the second in three sessions. Bond yields are easing 2-4 basis points, though New Zealand, where the central bank kept rates steady, saw a big jump in rates (11 bp in the 10-year yield). The New Zealand dollar is also the strongest of the major currencies, rallying a little more than 1%. The US dollar is mixed, and those currencies usually sensitive to risk and growth sentiment, like the other dollar-bloc currencies, Scandis, and emerging market currencies are trading heavily. The euro briefly dipped below $1.10 for the first time since mid-October has recovered slightly. Gold is around 0.5% higher, which is the most in nearly two weeks, and oil is off for the third consecutive session. |

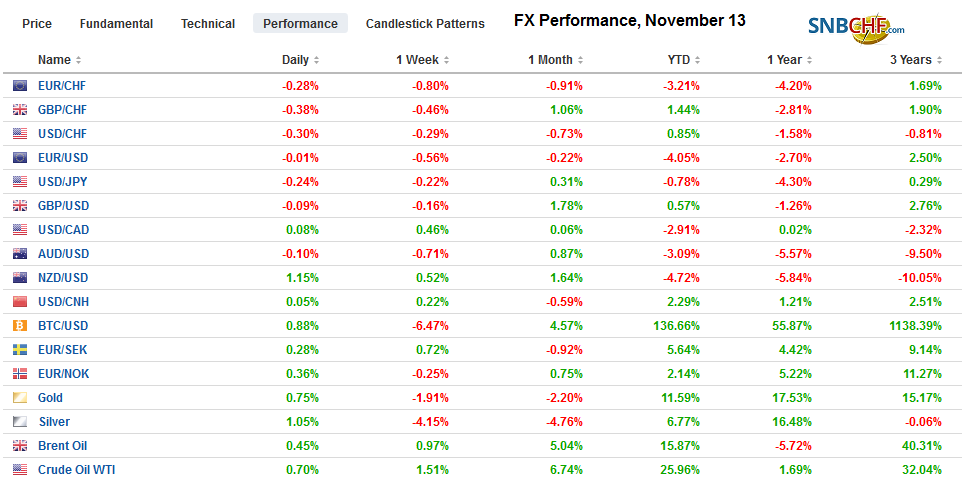

FX Performance, November 13 - Click to enlarge |

Asia Pacific

The New Zealand dollar fell every day last week amid speculation the central bank was going to cut rates this week. We thought the Kiwi’s decline was partly a correction to the previous week when it rose in every session. It also seemed as if sentiment shifted a bit at the start of the week. Still, the dramatic response to the Reserve Bank of New Zealand’s decision to stand pat earlier today shows the extent of the entrenched expectations. Even as it left rates unchanged (1.0% cash rate), it lowered its GDP forecast for the year through March to 2.2% from 2.7%. However, it also judged that the economic slowdown may be ending, and inflation will likely pick up. Monetary policy is already stimulative after the 75 bp rate cuts this year, including the unexpected 50 bp move in August. The 1% gain today looks to be the largest in at least five months. The two-year yield jumped 16 bp, and as we noted, the 10-year yield is up 11 bp.

Japan’s producer prices fell 0.4% in October year-over-year. It is the fifth consecutive month of deflation. Traded goods are leading the way. Import prices are off 10.5% year-over-year and export prices down 6.3%. The appreciation of the yen may be an under-appreciated factor. Over the past year (12-months), the yen is the only major currency to appreciate against the US dollar (~5.2%).

The dollar remains in a narrow range against the yen but testing four-day lows in the European morning below JPY108.90. There is an option for about $405 mln at JPY108.75 and another set for around $875 mln at JPY108.50-JPY108.60 that expires today. Bearish divergences with some technical indicators that did not confirm the recent new highs appear to leave the market vulnerable to a setback. That said, a convincing break of the JPY108.65 area is needed to signal anything of importance. The Australian dollar is extending its slide. The day-to-day decline is minor, but it is the fourth consecutive losing session, and the Aussie is at levels not seen more than 2 1/2 weeks. It is pushing through the (38.2%) retracement objective near $0.6830 of the rally from the start of last month. The next retracement target (50%) is $0.6800. The Chinese yuan is breaking its five-week advance that took the dollar back below CNY7.0. Today the dollar is a little above CNY7.02, its highest level since August 4.

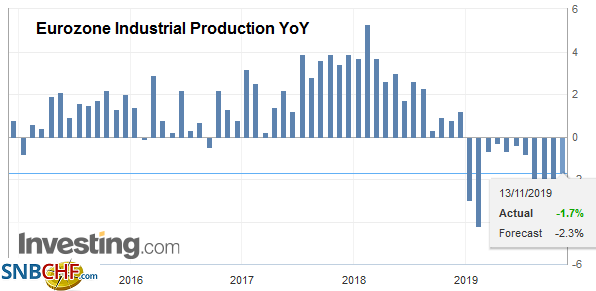

EuropeThe eurozone offered a rare pleasant economic surprise today. Weighed down by disappointing German data, EMU industrial output was expected to have declined by 0.2% in September. Instead, it eked out a 0.1% gain. It does not sound like much, but it is the first back-to-back increase in EMU industrial output since July-August 2017. Separately, tomorrow, Germany is expected to confirm that the world’s fourth-largest economy contracted in Q3 for the second quarter in a row. Although this is widely tipped and apparently reflected in prices already, it does not change the fact that negative interest rates are no prophylactic against recession. |

Eurozone Industrial Production YoY, September 2019(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

UK price pressures were softer than expected in October. Headline CPI fell by 0.2% to bring the year-over-year rate to 1.5% from 1.7%. CPIH, which includes owner-occupied housing costs, also eased to 1.5%. It is a three-year low. Input and output producer prices were even softer than expected, with the former falling 1.3% and posting the third consecutive monthly decline and bringing the year-over-year decline to -5.1%, also a three-year low. Output prices slipped 0.1% to shave the year-over-year increase to 0.8% from 1.2%, the weakest since 2016. The recent series of economic data have been disappointing. Tomorrow the UK reports retail sales.

The euro briefly traded below $1.10 before bouncing back. It nearly met the (61.8%) retracement target of last month’s rally (~$1.0995). The measuring objective of the potential double top is a bit lower near $1.0980. A move above $1.1040 would lift the technical tone, but there is an option for roughly 535 mln euros struck there that expires today. There is also an option for 550 mln euros at $1.1015 that is in play. Sterling is consolidating. It is inside yesterday’s range, which was inside Monday’s range. The market does not appear to have much near-term conviction. The Tories continue to lead opinion polls, but whether it gets an outright majority of seats remains up in the air.

America

President Trump’s speech to the Economic Club of NY was an extended stump speech. The strength of the US economy was hailed without the slightest mention of the $3 trillion increase in debt that it has cost. He indicated that making good on the handshake deal of what is heralded a phase 1, is still possible, but the US President did seem to make explicit what was previously implicit, namely, without an agreement, the tariff battle will escalate. Trump’s swipes at the Federal Reserve and his repeated call for negative interests, as if it gives Germany and Japan, for example, some sort of advantage, caused the audience to titter. They understand that there is no God-given right that the US has to the lowest interest rates in the world no matter how much Giscard d’Estaing’s concept of “exorbitant privilege” is misused and abused.

Chairman Powell speaks to the Joint Economic Committee of Congress at around 11:00 ET. He is bound to repeat his assessment that the “economy is in a good place” and that it will take a “material change” in the Fed’s outlook to change policy. This was part of the signal that the end of the mid-course correction was at hand. The Fed always forecasts business cycles that last forever, as if trees grow to the sky. He is unlikely to lecture Congress that negative interest rates are a symptom of something gone terribly wrong or compare negative interest rates to the fever that is both the symptom and the attempt of the body to cure itself. With 1.7% headline PCE deflator, which the Fed targets coupled with the 3.6%, the unemployment rate that is is below where all officials estimate is the long-run sustainable path (3.7%-4.0%), and growth slightly above trend, it seems quite obvious why US rates are not at the zero bound, let alone below it. Lastly, the Federal Reserve acknowledges that regulations encumber excess reserves and shape the incentive structure for some large banks to prefer cash to securities. However, it seemed to prefer providing more excess reserves than de-regulating, to which Treasury Secretary Mnuchin is more sympathetic.

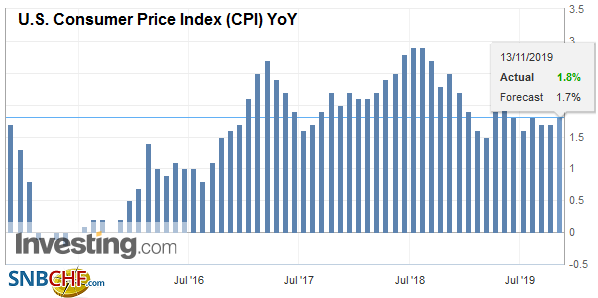

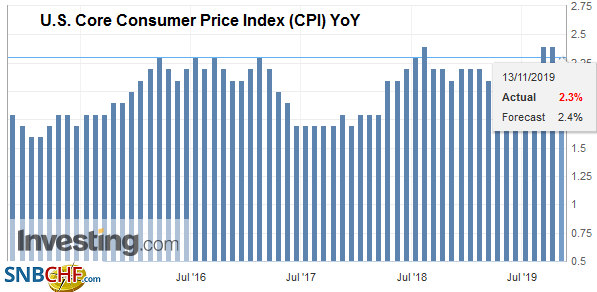

| The US reports October CPI figures today. The year-over-year pace is expected to be steady at 1.7% on the headline and 2.4% on the core. |

U.S. Consumer Price Index (CPI) YoY, October 2019(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

| Looking forward, the base effect warns that the headline pace may tick up in November and December. Last year, both months were flat. The core rate rose 0.2% in November and December 2018. This suggests that the headline rate may converge with the core rate rather than the other way around. Canada and Mexico’s economic calendars are empty. Mexico’s central bank meets tomorrow and is expected to deliver a 25 bp cut (to 7.5%). Brazil reports September retail sales and modest gains are expected. |

U.S. Core Consumer Price Index (CPI) YoY, October 2019(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The US dollar continues to trend higher against the Canadian dollar. The greenback has fallen in only one of the past seven sessions. It is near CAD1.3265 in the European morning, which is its best level in a little more than a month and is approaching the 200-day moving average just above CAD1.3275. Short-term US rates have risen back above Canadian rates, and the decline in oil and risk appetites weigh on the Loonie. A move above CAD1.3300 targets last month’s highs near CAD1.3350. The dollar jumped higher against the Mexican peso yesterday, perhaps as a proxy for angst in the region (e.g., Bolivia, Chile). The dollar has been trading roughly MXN19.00-MXN19.25 since mid-October and jumped above MXN19.36 yesterday and has moved closer to MXN19.40 today. A move above there could see MXN19.50, though there may be some intermittent resistance near MXN19.44. We note that the JP Morgan Emerging Market Currency Index has been trending lower and is at its lowest level since October 2 today. It is extending its two-week slide into the third week.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,Currency Movement,EUR/CHF,Eurozone Industrial Production,Featured,federal-reserve,FX Daily,New Zealand,newsletter,U.S. Consumer Price Index,USD/CHF