January was the last month in which China’s National Bureau of Statistics (NBS) specifically mentioned Fixed Asset Investment (FAI) of state holding enterprises (or SOE’s). For the month of December 2017, the NBS reported accumulated growth (meaning for all of 2017) in this channel of 10.1%. Through FAI of SOE’s, Chinese authorities in early 2016 had panicked themselves into unleashing considerable “stimulus.” There were already signs early in 2017 that enthusiasm for it was waning. In some ways, that was to be expected since even Chinese “stimulus” isn’t meant to be permanent. It was widely believed, however, that the effort would produce economic acceleration in China and therefore the rest of the world.

Topics:

Jeffrey P. Snider considers the following as important: 5) Global Macro, China, currencies, economy, EuroDollar, fai, Featured, Federal Reserve/Monetary Policy, fixed asset investment, industrial production, IP, Markets, newsletter, Retail sales, state-owned fai, stimulus

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

January was the last month in which China’s National Bureau of Statistics (NBS) specifically mentioned Fixed Asset Investment (FAI) of state holding enterprises (or SOE’s). For the month of December 2017, the NBS reported accumulated growth (meaning for all of 2017) in this channel of 10.1%. Through FAI of SOE’s, Chinese authorities in early 2016 had panicked themselves into unleashing considerable “stimulus.”

There were already signs early in 2017 that enthusiasm for it was waning. In some ways, that was to be expected since even Chinese “stimulus” isn’t meant to be permanent. It was widely believed, however, that the effort would produce economic acceleration in China and therefore the rest of the world. Convention always assumes, no matter how much evidence piles up to the contrary, that “stimulus” works without question. Specifically, the private economy over there was figured to more than pick up the slack as the official effort wound down.

It didn’t happen. I wrote in June 2017 of the potential consequences:

It raises further questions about official “stimulus” in the SOE channel of FAI. There are monetary as well as credit reasons for believing China’s government is being restricted by these factors in a way it probably does not want to be. Taken altogether among the three data points, we therefore have to consider the negative possibilities vis-à-vis what we already see of eroding “reflation.”

We wrote about those “negative” possibilities all throughout the latter half of last year. Primary among them was the Chinese government throwing in the towel – for good. In other words, as private FAI and even the whole Chinese economy failed to further accelerate as everyone, and I mean everyone, was anticipating, it seemed inconceivable that the government would just allow that to happen.

A lot of the re-evaluating of financial and monetary risk in later 2017, I believe, traces back to this one crucial element missing from the globally synchronized growth narrative. Not only is it missing, the activities of Chinese political authorities in the months since last spring suggest they have been actually and actively preparing for the consequences.

Of the three monthly NBS press releases pertaining to the main economic statistics (IP, RS, and FAI) for 2018, none have mentioned SOE FAI, state holding fixed asset investment, or any other variation of the term. It has been, purposefully it seems, written out of official communications. The NBS hasn’t even updated the English language database for it since the last entry for December 2017.

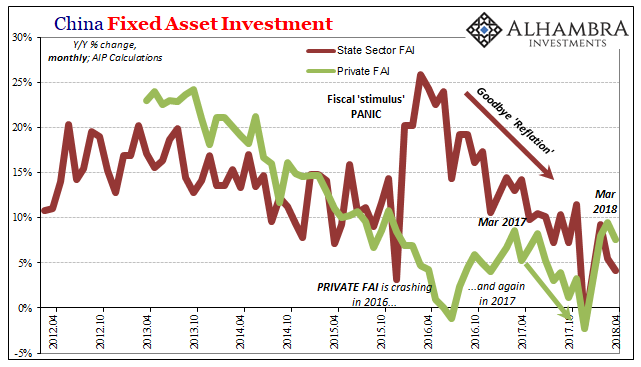

| In April 2018, total FAI decelerated further as the beginning-of-year burst in private FAI starts to fade again just as it has the last three years. We have to do some calculations to work backward to SOE FAI, but when we do we get an idea as to why the NBS may not want to highlight this segment anymore. The (recovery/acceleration) towel has been tossed into the ring. |

China Fixed Asset Investment, Apr 2012 - 2018(see more posts on China Fixed Asset Investment, ) - Click to enlarge |

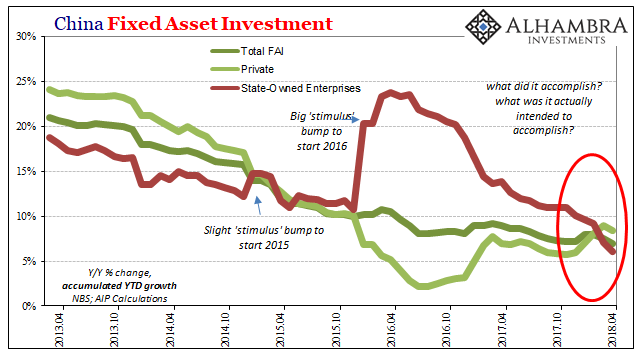

| The net result is total FAI, the backbone of China’s economy, and therefore the world’s, is growing now at the slowest pace (a new low) in nearly two decades. This will not stop the repeated characterizations of the Chinese economy as “strong” and “robust”, but as noted in prior months these are pretty blatantly dishonest attempts to stay on message. |

China Fixed Asset Investment, Apr 2013 - 2018(see more posts on China Fixed Asset Investment, ) - Click to enlarge |

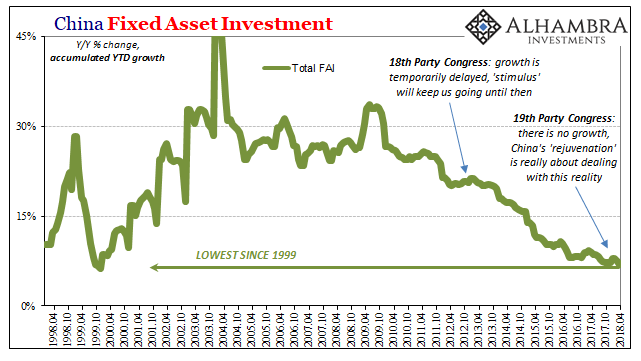

| And it’s a message that Chinese authorities no longer want to convey. That’s the really weird part. The Communists have been far more honest in economic action as well as political maneuvers than is being described in the Western media. To preserve this increasingly unrealistic idea of a successful (global) rebound, they have constructed a Potemkin economy on behalf of a Chinese government that really doesn’t want it!

What a world. |

China Fixed Asset Investment, Apr 1998 - 2018(see more posts on China Fixed Asset Investment, ) - Click to enlarge |

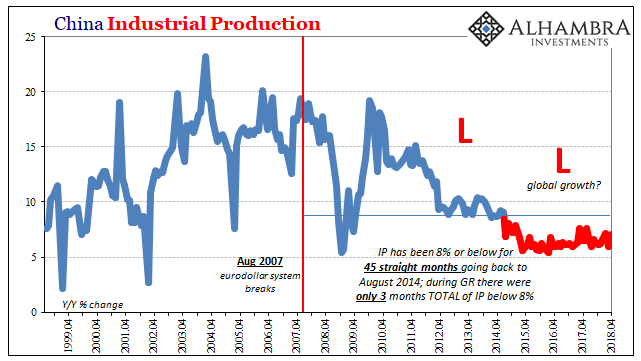

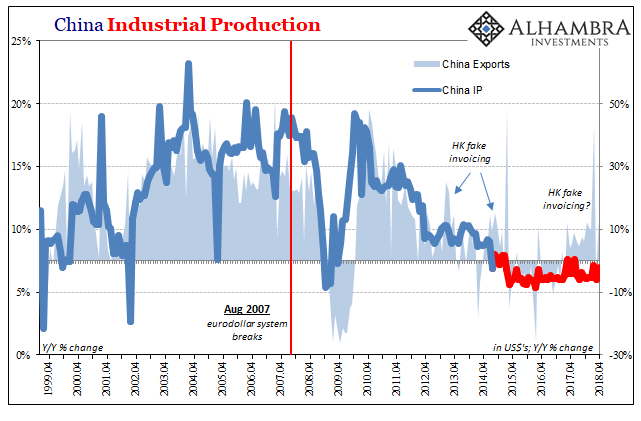

| The rest of China’s Big 3 numbers are equally dismal. Industrial Production (IP) expanded by 7% year-over-year in China, better than 6% growth in March but not meaningfully so. |

China Industrial Production, Apr 1999 - 2018(see more posts on China Industrial Production, ) - Click to enlarge |

| It was the 45th consecutive month of IP expansion less than 8%, a level that used to suggest major economic problems inside the Chinese economy’s industrial/manufacturing base. |

China Industrial Production, Apr 1999 - 2018(see more posts on China Industrial Production, ) - Click to enlarge |

| Rather than offer evidence for acceleration or even a stabilizing condition, they instead project the overarching “L” economy some of China’s officials have been warning about for several years already.

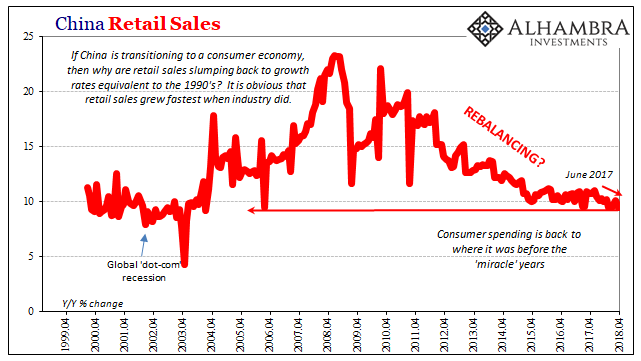

Retail sales growth in April was a dismal 9.4% which ties December 2017 (and February 2006) for the lowest since the recovery after the dot-com recession almost a decade and a half ago. |

China Retail Sales, Apr 1999 - 2018(see more posts on China Retail Sales, ) - Click to enlarge |

This is an important miss since the parallel narrative to globally synchronized growth, China’s economic rebalancing, largely depends upon the continued strength (which has been merely assumed or extrapolated) of Chinese consumers. Retail Sales growth projects instead a similar “L” to Industrial Production, only with a downward bend in its non-contraction leg dating back to last July when it started to become clear about both lack of acceleration and lack of official address to it.

I wrote last October, “It seems more and more that authorities [in China] are battening down the hatches, not opening themselves up in a way that a more optimistic and bright future would lead.” Winding down SOE FAI while no longer talking much if at all about it is pretty consistent with that analysis.

Tags: China,currencies,economy,EuroDollar,fai,Featured,Federal Reserve/Monetary Policy,fixed asset investment,industrial production,IP,Markets,newsletter,Retail sales,state-owned fai,stimulus