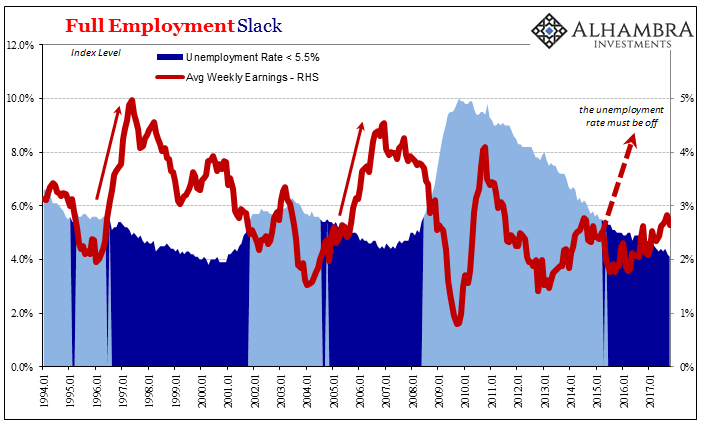

As a natural progression from the analysis of one historical bond “bubble” to the latest, it’s statements like the one below that ironically help it continue. One primary manifestation of low Treasury rates is the deepening mistrust constantly fomented in markets by the media equivalent of the boy who cries recovery. That narrative “has ruffled a few feathers,” BMO Capital Markets strategists Ian Lyngen and Aaron Kohli wrote in a note last week. “Growth is moving at a solid clip and the labor market is ostensibly at full employment — so why aren’t we in an environment with a steeper curve and higher yields?” Full Employment Slack, Jan 1994 - 2017 - Click to enlarge If solid growth plus full employment equals a

Topics:

Jeffrey P. Snider considers the following as important: China Industrial Production, currencies, economy, Featured, Federal Reserve/Monetary Policy, Markets, newslettersent, The United States, they really don't know what they are doing, U.S. Trade Balance, U.S. unemployment rate

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

As a natural progression from the analysis of one historical bond “bubble” to the latest, it’s statements like the one below that ironically help it continue. One primary manifestation of low Treasury rates is the deepening mistrust constantly fomented in markets by the media equivalent of the boy who cries recovery.

|

Full Employment Slack, Jan 1994 - 2017 - Click to enlarge |

| If solid growth plus full employment equals a steeper yield curve and higher long rates, and they do, then a flatter curve at lower nominal rates must then equal what? The answer is far easier than the media makes it out to be. In what is pure Aristotelian sophistry, they try very hard to ignore their own logic where the answer to this “conundrum” is clearly choppy, lackluster growth that has left the (global) economy considerable hangover slack. |

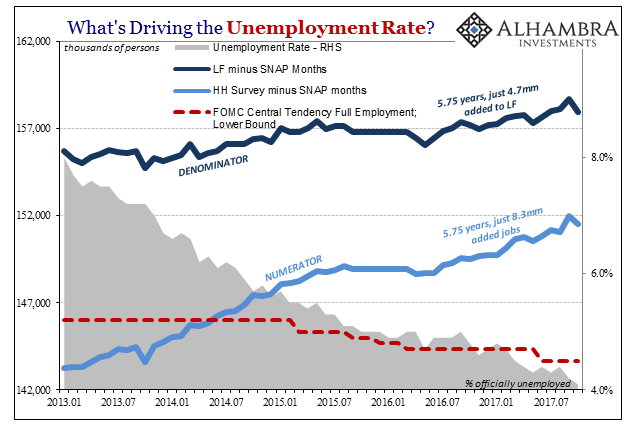

US Unemployment Rate, Jan 2013 - Jul 2017(see more posts on U.S. Unemployment Rate, ) - Click to enlarge |

| That’s what the yield curve continues to say, the only thing it has said for many years now.

It’s amazing that after more than a decade now of these markets (UST’s, eurodollar futures, swaps, FX, etc.) declaring that “something” is wrong how easily it is for these people to simply set it all aside because their highly optimistic view on the economy, derived exclusively from central bank forecasts and actions, just has to be right. They are actually saying that markets need to conform to their opinions without evidence, and without recognizing the market prices are evidence, as if theirs is the only correct possibility. Time plays a significant component of that backwards view because it is extremely hard to believe the global economy could ever be stuck in such an awful place for so long. It just seems so impossible, completely out of our own experience. Even if by random luck you would think enough would have gone right in just monetary policy by now that what is claimed for the economy in the mainstream might actually have come true. But this set of circumstances is not absent from all experience, just the modern one. |

Bond Bubble Comparisons, Jan 1926 - 1961 - Click to enlarge |

| The point of failure is right where it shouldn’t be. |

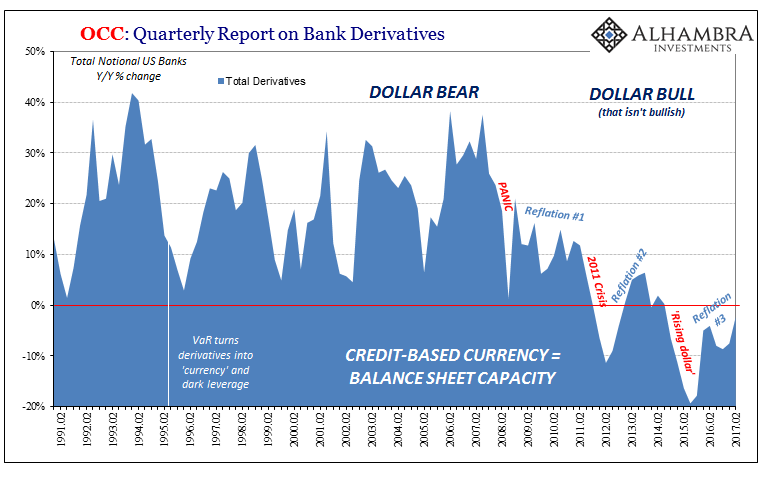

Quarterly Report on Bank Derivatives, Feb 1991 - Feb 2017 - Click to enlarge |

| That’s what’s making it so difficult. Even the bond market (as eurodollar futures and the rest) is declaring this to be the case. |

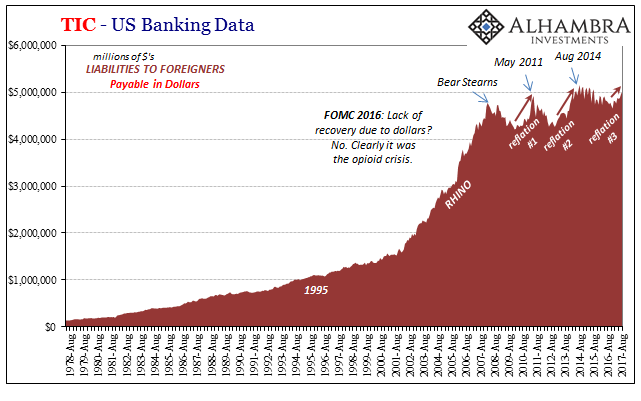

US Banking Data, Aug 1978 - 2017 - Click to enlarge |

| The issue is central banks and central bankers who have done nothing right, failed to achieve any positive offsets, and left the global economy to stand naked against the intermittent forces (three so far) of negative monetary decay. |

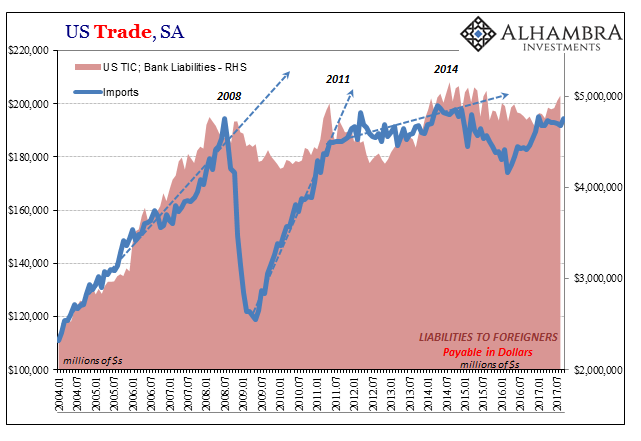

US Trade Balance, Jan 2004 - Jul 2017(see more posts on U.S. Trade Balance, ) - Click to enlarge |

| So the real problem in the mainstream is over who to believe; the central bank technocrats who most people have been thoroughly schooled to trust without question, or these markets where actual discipline is the order of operation? |

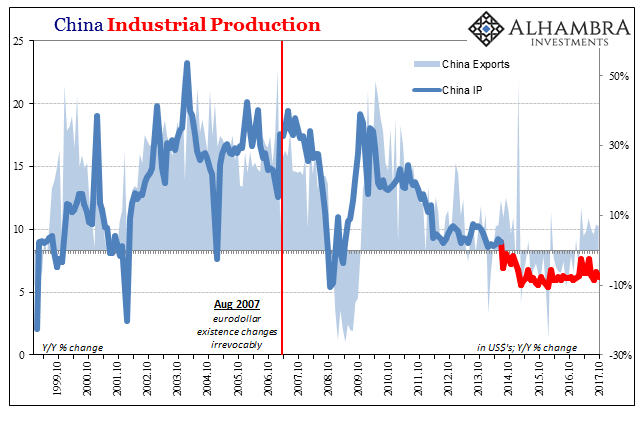

China Industrial Production, Oct 1999 - 2017(see more posts on China Industrial Production, ) - Click to enlarge |

| As hard as it may be to believe, I once gave central bankers the benefit of the doubt, too (though perhaps not as stridently as some still today). I had come to expect in early 2007 that the Fed, though clearly behind the curve, would catch up and fix the problem before it got out hand. Greenspan’s reputation had lost a lot of luster in my eyes as a result of lingering unanswered questions about the dot-com era and “jobless recovery” after that (mild) recession, but surely he wasn’t grossly incompetent. He couldn’t have been, could he? |

China Industrial Production, Oct 1999 - 2017(see more posts on China Industrial Production, ) - Click to enlarge |

| It was really difficult to accept that it was all smoke and mirrors, one of those viral kind of things where you tend to believe something is true simply (solely) because everyone else does. It becomes such hardened “fact” that to even think about challenging it makes people wonder what’s wrong with you. The wisdom of the crowd is perhaps just as often that sort of mass delusion wrapped in an impenetrable bubble.

Then August 9 happened, and similar days happened afterward in repeating fashion. Then 2008. That should have been more than enough to dispel any notions of competence on any subject related and not; monetary as well as economic. The panic itself and the enormous global economic consequences should have ended Economics. |

ABS Commercial Paper Outstanding, Jan 2001 - 2017(see more posts on Commercial Paper, ) - Click to enlarge |

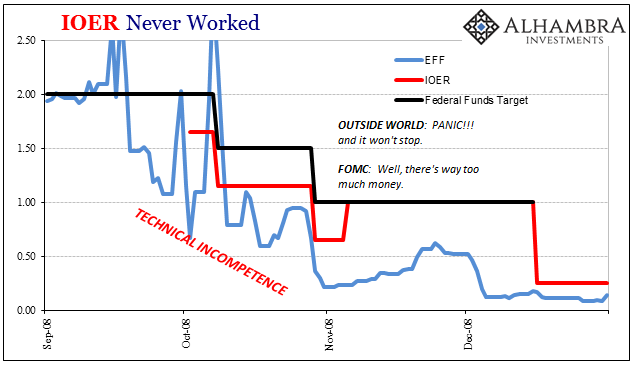

They really don’t know what they are doing. They never have. The central bank holds only one specialty to which it is any good, a capability that Milton Friedman pointed out in one of the last interviews he ever gave more than a decade ago just prior to the onset of all this trouble.

|

IOER Never Worker, Sep - Dec 2008 - Click to enlarge |

| Central bankers simply did it again. What was Ben Bernanke’s message at the end of 2008? He was no longer talking about prevention, as had been standard up until Lehman, and accounting for what he had done prior. Bernanke simply began speaking and writing and televising exclusively about “jobs saved”, what the Fed was going to do in the future to cushion the blow that was then some devious, exogenous factor no reasonable person could ever think to blame monetary officials about. No longer would there be much about the past, what they had done prior. All the world’s central banks were suddenly victims, too. |

Dollar Swaps, Jul 2007 - 2008 - Click to enlarge |

| And like the thirties, it was all BS. But “we” let them off the hook to write their books, revise the official history of the crisis so that somehow they come off the heroes when they were seriously, perhaps criminally, as well as obviously (when you look), derelict. The degree of gross incompetence was absolutely staggering – and it never ceased. You require no special training to easily understand that if as a central banker you “need” a second QE (let alone a third or fourth) the whole thing just doesn’t work (how can it be “quantitative” if you don’t know the right quantity?) |

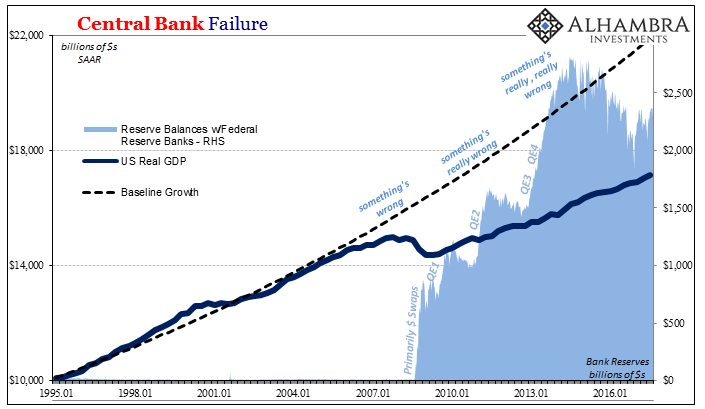

Central Bank Failure, Jan 1995 - 2016 - Click to enlarge |

| Central banks are the epitome of PR and media manipulation. And that’s all they are, certainly no money in monetary policy. They’ve done such a masterful job of it that even today no matter how much market data disagrees, people just refuse to believe it. |

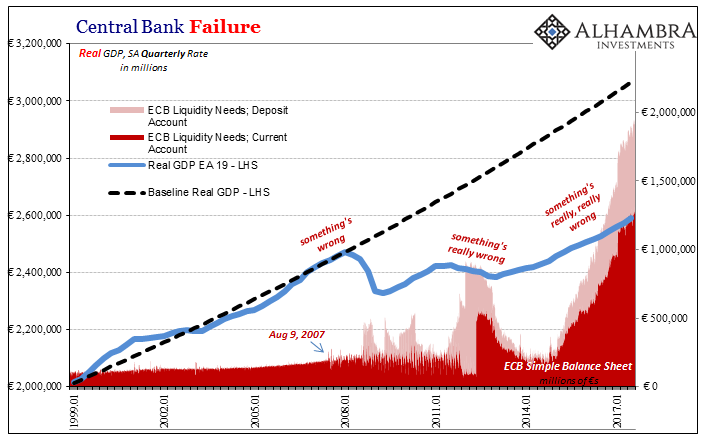

Central Bank Failure, Jan 1999 - 2017 - Click to enlarge |

Tags: China Industrial Production,currencies,economy,Featured,Federal Reserve/Monetary Policy,Markets,newslettersent,they really don't know what they are doing,U.S. Trade Balance,U.S. Unemployment Rate