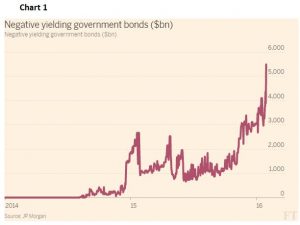

When the central banks of three European countries and the European Central Bank (ECB) itself introduced negative interest rates (NIR) in mid -2014, many considered it be a temporary measure, a new experiment in monetary policy. But when the Bank of Japan did the same in January 2016 and when the ECB pushed rates further into negative territory in March 2016, the international investment world stood up and took notice. Policy makers are now prepared to test this unconventional technique in an effort to stimulate growth and tackle deflation.

The financial press is full of articles on the dangers of this policy. These unconventional moves have provoked a lot of criticism, especially from the banking community who fear a strangulation of normal banking activities. A lot has been written about the dangers that NIR pose to the stability of banks and to the possible harm to savers and investors alike. This article is an attempt to put the whole question of NIR into a more balanced perspective. To begin with, it is important to have some background to why and how NIRs have come to characterize so much of government debt.

Understanding Negative Interest Rates

October 1, 2016