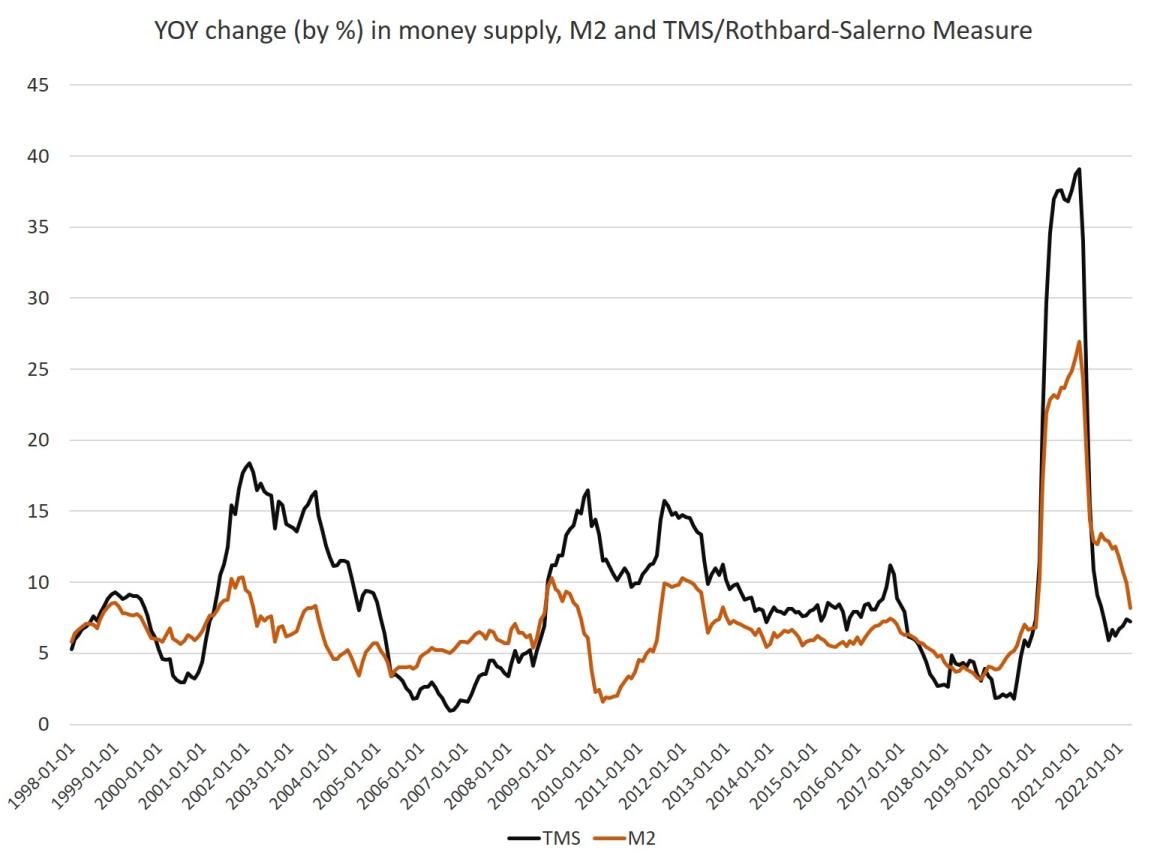

Money supply growth fell slightly in April, falling below March’s eight month high. Even with March’s bump in growth, though, money supply growth remains far below the unprecedented highs experienced during much of the past two years. During thirteen months between April 2020 and April 2021, money supply growth in the United States often climbed above 35 percent, well above even the “high” levels experienced from 2009 to 2013. As money supply growth returns to “normal,” however, this may point to recessionary pressures in the near future. During April 2022, year-over-year (YOY) growth in the money supply was at 7.23 percent. That’s down from March’s rate of 7.41 percent, and down from the April 2021’s rate of 36.8 percent. The growth rate peaked in February 2021

Topics:

Ryan McMaken considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Money supply growth fell slightly in April, falling below March’s eight month high. Even with March’s bump in growth, though, money supply growth remains far below the unprecedented highs experienced during much of the past two years. During thirteen months between April 2020 and April 2021, money supply growth in the United States often climbed above 35 percent, well above even the “high” levels experienced from 2009 to 2013. As money supply growth returns to “normal,” however, this may point to recessionary pressures in the near future.

During April 2022, year-over-year (YOY) growth in the money supply was at 7.23 percent. That’s down from March’s rate of 7.41 percent, and down from the April 2021’s rate of 36.8 percent.

The growth rate peaked in February 2021 at 23.12 percent. Historically, the growth rates during most of 2020, and through April 2021, were much higher than anything we’d seen during previous cycles, with the 1970s being the only period that comes close.

| The money supply metric used here—the “true” or Rothbard-Salerno money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. The Mises Institute now offers regular updates on this metric and its growth. This measure of the money supply differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits and retail money funds).

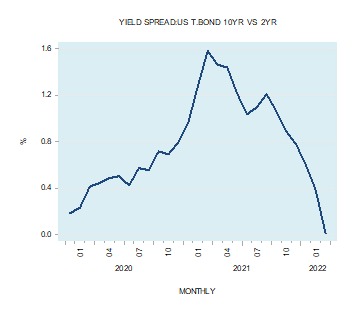

In a contrast with TMS, M2 growth rates have continued to fall over the past five months, with the growth rate in April falling slightly to 8.20 percent. That’s down slightly from March’s growth rate of 9.92 percent. April’s rate was well down from April 2021’s rate of 18.52 percent. M2 growth peaked at a new high of 26.91 percent during February 2021. Money supply growth can often be a helpful measure of economic activity, and an indicator of coming recessions. During periods of economic boom, money supply tends to grow quickly as commercial banks make more loans. Recessions, on the other hand, tend to be preceded by periods of slowing rates of money supply growth. However, money supply growth tends to begin growing again before the onset of recession. As recession nears, the TMS growth rate typically climbs and becomes larger than the M2 growth rate. This occurred in the early months of the 2002 and the 2009 crises. A similar pattern appeared before the 2020 recession. Money-supply growth fell throughout much of 2019, and the economy appeared headed toward recession. However, the “lockdowns” and stay-at-home orders of the covid panic accelerated this process and ensured a sizable drop in economic activity. Massive stimulus then pushed money-supply growth up to record levels. Trends in money supply growth also appear to be connected to the shape of the yield curve. As Bob Murphy notes in his book Understanding Money Mechanics, a sustained decline in TMS growth often reflects spikes in short-term yields, which can fuel a flattening or inverting yield curve. Murphy writes:

In other words, a sizable drop in the TMS growth levels often precedes an inversion in the yield curve which itself points to an impending recession. Indeed, we may be seeing that right now in mid June 2022. |

. |

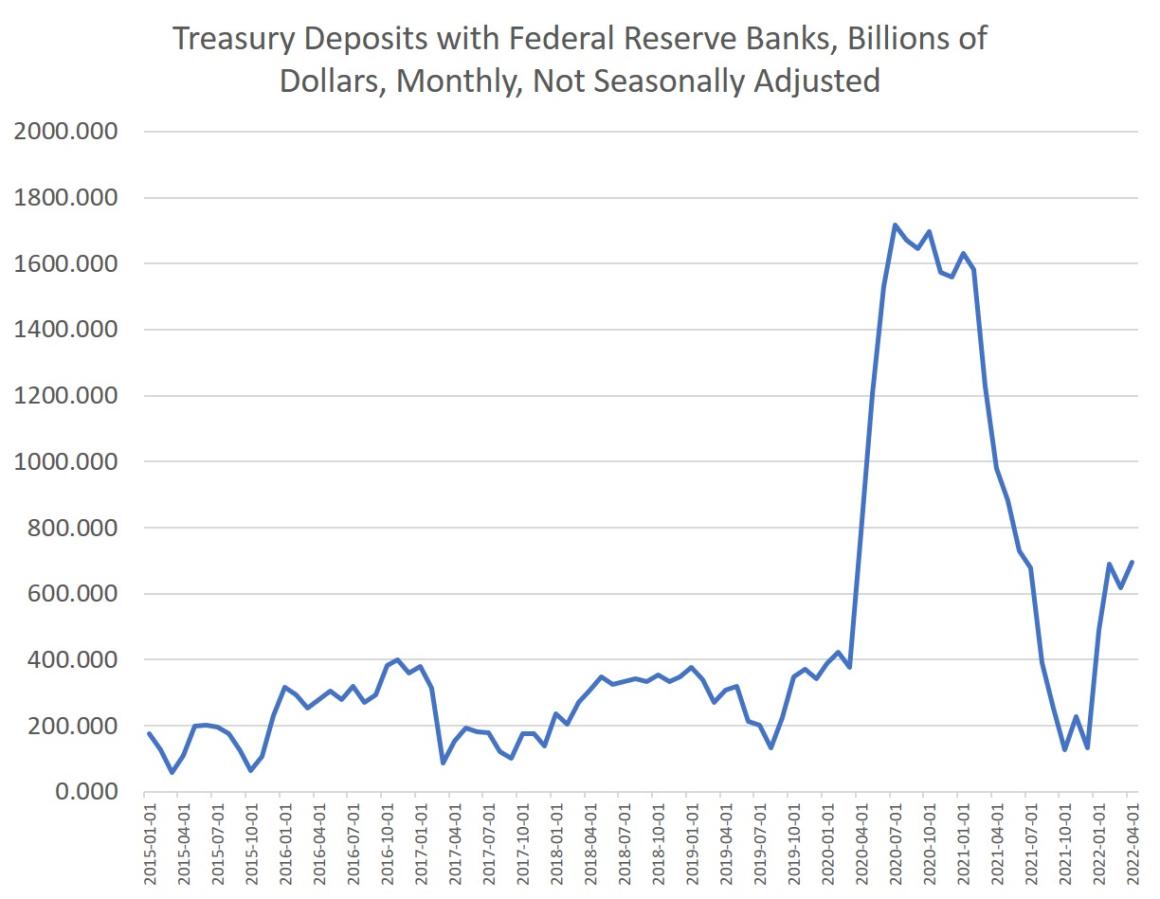

Fed Stimulus and Declining Loan GrowthMoney supply growth was fueled in part by enormous amounts of deficit spending that occurred throughout 2020 and 2021. This led to the “need” for large amounts of monetization by the Federal Reserve. (This was needed to keep interest on the national debt low.) Indeed, as federal deficit spending grew throughout 2020, Fed purchases of government bonds increased substantially as well. Since June 2021, however, federal spending has fallen well below its earlier peaks. This has allowed the Fed to scale back its monthly asset purchases, and the Fed has announced the end of its program of large-scale purchases of US debt. One factor that has buoyed TMS in recent months—in part driving TMS above the M2 growth rate—has been rising levels in Treasury deposits at the Fed. These totals are factored into the TMS money supply measure—but not with M2—and this total has risen from $133 billion in December to $694 billion in April. Overall, such a sizable drop in TMS growth over the past year continues to point toward a weakening economy. With recent trends showing falling real wages, multi-decade price inflation, and a flattening yield curve, we may against soon see the recessionary aftermath of a downward swing in TMS growth levels. |

. |

You Might Also Like

Why Russia’s Authoritarian Regime Continues to Enjoy Public Support

Why Russia’s Authoritarian Regime Continues to Enjoy Public Support

2022-06-05

One of my areas of research in institutional economics is the social behavior of people under different political regimes, what Thomas Schelling called micromotives and macrobehavior. Of course, this topic is directly related to many disciplines, from behavioral economics and political theory to the neurobiology of decision-making and the theory of biological markets.

The Nationalities Question

The Nationalities Question

2022-04-22

[This article was published in in The Irrepressible Rothbard, available in the Mises Store.]

Upon the collapse of centralizing totalitarian Communism in Eastern Europe and even the Soviet Union, long suppressed ethnic and nationality questions and conflicts have come rapidly to the fore. The crack-up of central control has revealed the hidden but still vibrant "deep structures" of ethnicity and nationality.

To those of us who glory in ethnic diversity and yearn for national justice, all this is a wondrous development of what has previously lived only in fantasy or longing: it is a chance in Europe at long last, to begin to reverse the monstrous twin injustices of Sarajevo and Versailles. It is like being back in 1914 or 1919 again, with a chance for the map of Europe and near Asia to be

How the Fed’s Tampering with the Policy Rate Affects the Yield Curve

How the Fed’s Tampering with the Policy Rate Affects the Yield Curve

2022-04-19

At the end of March this year the difference between the yield on the ten-year Treasury bond and the yield on the two-year Treasury bond fell to 0.010 percent from 1.582 percent at the end of March 2021.

Do “Inflationary Expectations” Cause Inflation? Contra Krugman, the Answer Is No

Do “Inflationary Expectations” Cause Inflation? Contra Krugman, the Answer Is No

2022-04-09

In the New York Times article “How High Inflation Will Come Down,” Paul Krugman suggests that the key for future inflation is inflation expectations. Krugman does not think that currently inflation expectations are comparable to the 1980s.

Will Biden Sanction Half the World to Isolate Russia?

Will Biden Sanction Half the World to Isolate Russia?

2022-03-31

The United States is no longer in any position to remake the world in its image. It’s not 1945 or even 1970. Yet the US seems to be gearing up to bully half the world into compliance with the US Russia sanctions.

Governments “Sanction” Their Own Citizens Every Day. The Russia Sanctions Are Just a Natural Evolution.

Governments “Sanction” Their Own Citizens Every Day. The Russia Sanctions Are Just a Natural Evolution.

2022-03-19

Russian president Vladimir Putin’s invasion of Ukraine in the last week of February 2022 was the culmination of decades of transnational statist expansion.

The Divided States of America | A Conversation with Jeff Deist & Tom Woods

The Divided States of America | A Conversation with Jeff Deist & Tom Woods

2022-01-14

Mises Institute President, Jeff Deist, and Tom Woods, author and host of the Tom Woods podcast, join Judge Napolitano to go in-depth on the state of America today.

Why “Macro” Thinking in Economics Is Such a Problem

Why “Macro” Thinking in Economics Is Such a Problem

2021-12-22

As someone who teaches public finance (better termed the economics of government), I can’t count how many times I have heard politicians promise “comprehensive” reforms to some major problem. But what such efforts actually produce is always different from what is promised, because such achievements are beyond government’s competence.

Tags: Featured,newsletter