Swiss Economicblogs.org

Swiss Economicblogs.org

The CIO's view of the week ahead.The global economy is a bag of mixed signals. Last week, US retail sales for July came out stronger than expected, proving the US consumer remains in good shape. Hopefully, this will buoy the US economy, as it suffers elsewhere, including manufacturing and business investment. Meanwhile, data out of China and Germany, the world’s second and fourth largest economies, proved more worrying, underlining concerns about global industry as trade tensions continue to...

Read More »Italy: Back to polls in Q4 2019?

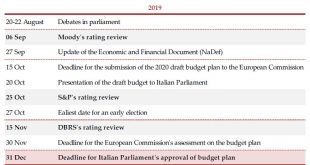

Recent developments in Italy’s political landscape have increased the probability of early elections in Q4 2019, but the situation is not so straightforward. Last week, political tensions in Italy intensified as Matteo Salvini, the League’s leader triggered a no confidence vote against Prime Minister Giuseppe Conte. PM Conte will address the Senate on 20 August. A confidence vote will likely follow the speech, though further delays remain a possibility. Once the...

Read More »Italy: Back to polls in Q4 2019?

Recent developments in Italy’s political landscape have increased the probability of early elections in Q4 2019, but the situation is not so straightforward. Last week, political tensions in Italy intensified as Matteo Salvini, the League’s leader triggered a no confidence vote against Prime Minister Giuseppe Conte.PM Conte will address the Senate on 20 August. A confidence vote will likely follow the speech, though further delays remain a possibility.Once the government dissolves, the...

Read More »New monetary policies for new challenges

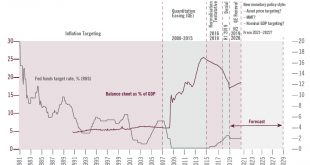

As central banks try (yet again) to bolster faltering growth and inflation, it is important to grasp how the ‘style’ and aims of monetary policy-making have changed over time and how they need to evolve in the future. The world is being disrupted by structural trends such as populism, demographic and climate change and technological innovation. Likewise, with previous approaches producing fewer results, we believe it is time to envisage monetary policies that address...

Read More »New monetary policies for new challenges

As central banks try (yet again) to bolster faltering growth and inflation, it is important to grasp how the ‘style’ and aims of monetary policy-making have changed over time and how they need to evolve in the future.The world is being disrupted by structural trends such as populism, demographic and climate change and technological innovation. Likewise, with previous approaches producing fewer results, we believe it is time to envisage monetary policies that address these sources of...

Read More »The case for fiscal stimulus strengthens in Germany

German real GDP shrank in the second half of the year, reinforcing our view of a significant ECB action in September.The German economy shrank by 0.1% quarter-on-quarter (q-o-q) in Q2. Today’s report contained some positives news, notably regarding the resilience of domestic demand.Nevertheless, the ongoing trade disputes between China and the US, China weakness, the threat of auto tariffs and the threat of a no-deal Brexit to supply chains, in addition to the auto sector’s own issues are...

Read More »Developed market equities update: a fairly reassuring reporting season

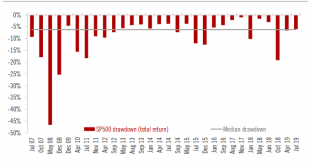

There is an ongoing tug-of-war between trade tensions and fundamentals Due to renewed trade tensions, the S&P 500 corrected by 6.0% and the Stoxx Europe 600 by 5.8% from the late July peak to the 5 August low. Because the pullback was clustered around just a few days, its intensity was reminiscent of the worst market days of past major crises. Safe haven assets benefitted significantly, with gold gaining 7.4% from the late July equity market peak to the 5 August...

Read More »Developed market equities update: a fairly reassuring reporting season

There is an ongoing tug-of-war between trade tensions and fundamentalsDue to renewed trade tensions, the S&P 500 corrected by 6.0% and the Stoxx Europe 600 by 5.8% from the late July peak to the 5 August low. Because the pullback was clustered around just a few days, its intensity was reminiscent of the worst market days of past major crises.Safe haven assets benefitted significantly, with gold gaining 7.4% from the late July equity market peak to the 5 August low and 10-year US...

Read More »Weekly View – Dot-com bond?

The CIO Office's view of the week ahead.The knock-on effects of Trump’s tweets have jumped from the equity and bond markets to the economy to central banks and now currency markets. Indeed, the trade war turned tech war now increasingly resembles a currency war and a race to the bottom. The Chinese currency depreciated below CNY 7/USD after the Chinese authorities seemingly let the currency weaken on the back of Trump’s latest tariffs announcement, earning them the ‘currency manipulator’...

Read More »Update on gold – bad news is good news

Increased trade tensions have boosted the gold price to above USD 1,500.The increased trade tensions following Trump’s 1 August tweet threatening additional tariffs on Chinese goods has boosted the gold price above USD 1,500 per troy ounce.The recent developments are supportive of gold investment demand because of a lower opportunity cost associated with holding gold and greater demand for safe haven assets. Coupled with strong demand from central banks, the medium-term outlook of the yellow...

Read More »