There are only two ways to survive a decline in income and net worth: slash expenses or default on debt. In post-World War II America, the cultural zeitgeist viewed frugality as a choice: permanent economic growth and federal anti-poverty programs steadily reduced the number of people in deep economic hardship (i.e. forced frugality) and raised the living standards of those in hardship to the point that the majority of households could choose to be frugal or live large by borrowing money to enable additional spending. Either way, rising income and net worth would raise all ships, frugal and free-spending alike. For everyone above the bottom 20%, frugality was viewed as a sliding scale of choice: if you couldn’t increase your income fast enough, then borrow

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

There are only two ways to survive a decline in income and net worth: slash expenses or default on debt.

In post-World War II America, the cultural zeitgeist viewed frugality as a choice: permanent economic growth and federal anti-poverty programs steadily reduced the number of people in deep economic hardship (i.e. forced frugality) and raised the living standards of those in hardship to the point that the majority of households could choose to be frugal or live large by borrowing money to enable additional spending.

Either way, rising income and net worth would raise all ships, frugal and free-spending alike.

For everyone above the bottom 20%, frugality was viewed as a sliding scale of choice: if you couldn’t increase your income fast enough, then borrow whatever money you needed. If you chose to be frugal, in moderation (i.e. clipping coupons and shopping for the cheapest airline seats, etc.) this was viewed as admirable fiscal prudence; if pushed beyond moderation then it was dismissed as counter to the American spirit of everlasting expansion: tightwad is not an endearment.

Thus none of us immoderately frugal folks ever fit in. Our frugality raised eyebrows and drew derogatory exhortations from indebted free-spenders to “get out there and live a little,” i.e. blow hard-earned money on aspirational gewgaws or status-enhancing fripperies, including the oh-so-precious “experiences” that have now replaced gauche physical markers of status-climbing.

We are now entering a new era of forced frugality in which incomes and net worth stagnate or decline while the cost of living rises and borrowing is no longer frictionless.

To say that these changes will shock the system is putting it mildly. Here’s the key dynamic in forced frugality: income can drop precipitously without any ratcheting to slow the decline, but costs only ratchet higher, or decline by nearly imperceptible degrees; that is, costs are “sticky” and refuse to slide down as easily as income.

The second key dynamic in forced frugality is the tightening of lending and the rising cost of borrowed money. When lenders could assume that almost every household’s income would increase as a byproduct of ceaseless economic expansion, and assets such as stocks, bonds and houses would always increase in value (any spots of bother are temporary), then the odds of a nasty default (in which the borrower stiffs the lender–no monthly payments to you, Bucko)–were low.

But once incomes and asset valuations are more likely to fall than rise, the door to lending slams shut. Why would lenders extend loans to households and enterprises that are practically guaranteed to default? Any lender that self-destructive would soon be stripped of their capital and solvency.

The general assumption is that since central banks are buying bonds, interest rates for borrowers can only go down. This assumption is misguided. The base assumption of all lenders is that a very thin layer of borrowers will default. Once this layer thickens, it makes no sense to lend to everyone who can fog a mirror.

Unwary lenders are about to learn a very painful lesson about the creditworthiness of supposedly solvent middle-class households: since income isn’t “sticky,” households that had high credit scores for years can quite suddenly default on their loans once their incomes plummet.

As for the borrower’s assets, those too can plummet in value, leaving the lender with zero collateral or an asset for which there is no buyer, regardless of the appraised value.

The income/assets slope is greased while the cost slope is on a resistant ratchet. Income can slide down effortlessly while costs stubbornly refuse to fall.

The net result of this dynamic is forced frugality. For the first time in decades, households and enterprises cannot count on a resumption of growth in a few months and higher incomes and asset valuations.

To the dismay of living-large-on-debt households and enterprises, the only way to get more than you have now will be to save, save, save cash. Earning more from one’s labor will be difficult, as will reaping easy speculative gains from simply owning assets.

| The debt-free frugal may be forgiven for indulging in a bit of schadenfreude toward those who scorned frugality in favor of living large in the moment. Now who’s living large? Not the extremely frugal, because squandering money gives them no pleasure, and they prefer the anti-status “status” of old cars and trucks, tools that have lasted decades and assets that look like everyone else’s except they’re debt-free.

As for income–those who control and invest their own capital and labor, the class I’ve long called mobile creatives–will have far more opportunities than those chained to the monoculture plantations of corporate cartels and government agencies squeezed by collapsing tax revenues. A great many people who reckoned moderate frugality was more than enough will discover it no longer suffices. A great many other people who reckoned they were rich enough to spurn frugality will discover their income no longer covers their expenses and so expenses will have to be slashed and burned to the ground. And many frugal people who did the best they could with limited income will find that even extreme frugality can’t fix a decline in income. An economy-wide reckoning of what’s essential is just starting. Netflix subscription? Gym membership? Fast food takeout a couple times a week? No, no and no. A thousand no’s as there are only two ways to survive a decline in income and net worth: slash expenses or default on debt. Both are toxic to “growth” in spending and debt. |

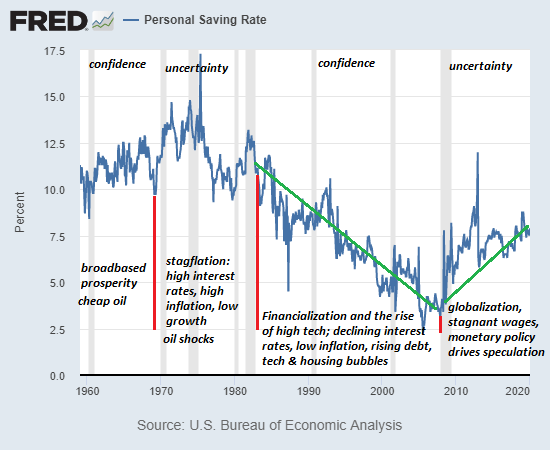

Personal Saving Rate, 1960-2020 - Click to enlarge |

You Might Also Like

Helicopter Money: Short-Term Relief Won’t Cure our Financial Disease

Helicopter Money: Short-Term Relief Won’t Cure our Financial Disease

The collateral supporting the global mountain of debt is crumbling as speculative bubbles deflate. A great many freebies are being tossed in the Helicopter Money basket. That households experiencing declines in income need immediate support is obvious, as is the need to throw credit lifelines to small businesses.

The Pandemic Is Accelerating the Breakdown That Began a Decade Ago

The Pandemic Is Accelerating the Breakdown That Began a Decade Ago

The feedback loop has reversed: by saving more, people will spend, borrow and speculate less, draining the fuel from any broadbased expansion. In eras of confidence and certainty, people save less and spend more freely.

The Wonderful Insanity of Globalization

The Wonderful Insanity of Globalization

So here’s an April Fools congrats to globalization’s many fools. The tradition here at Of Two Minds is to make use of April Fool’s Day for a bit of parody or satire, but I’m breaking with tradition and presenting something that is all too real but borders on parody: the wonderful insanity of globalization.

ECB Approaching its Bazooka Moment

ECB Approaching its Bazooka Moment

The ECB appears to be moving closer to activating Outright Monetary Transactions (OMT). Despite being part of Draghi’s “whatever it takes” moment, OMT has never been used. If the Fed’s open-ended QE is seen as dollar-negative, then OMT should be seen as euro-negative.

RECENT DEVELOPMENTS

At the regularly scheduled March 12 meeting, the ECB delivered a package of easing measures that were in hindsight quite underwhelming. The ECB boosted QE by a total of EUR120 bln by year-end, but gave no details on how the purchases will be spread out. Recall that the ECB restarted QE at the September 2019 meeting by buying EUR20 bln per month. The bank offered unlimited liquidity on a temporary basis through additional longer-term refinancing operations (ordinary LTROs) whilst lowering the rate

Markets continue to digest the implications of the Fed’s bazooka moment last week. The data highlight this week will be March jobs data Friday; key manufacturing sector data will come out earlier in the week. On Friday, BOC delivered an emergency 50 bp rate cut to 0.25% and started QE.

Dollar Bid as Market Sentiment Worsens

Dollar Bid as Market Sentiment Worsens

The virus news stream out of Europe has improved a bit. The US is already taking about the next relief bill; the Fed continues to roll out measures to address dollar funding issues. ADP and ISM manufacturing PMI are the US data highlights. Regulators across Europe are asking banks to stop paying dividends; eurozone and UK reported final manufacturing PMIs.

FINMA unterstützt das Liquiditätspaket des Bundesrats und rollt weitere Massnahmen aus

FINMA unterstützt das Liquiditätspaket des Bundesrats und rollt weitere Massnahmen aus

Die Eidgenössische Finanzmarktaufsicht FINMA begrüsst ausdrücklich das heute vom Bundesrat verabschiedete Massnahmenpaket des Bundes. Dieses sieht eine rasche und unbürokratische Versorgung der Realwirtschaft mit Liquidität via die Banken vor. Um die bestehende Robustheit der Schweizer Finanzinstitute beizubehalten, ruft die FINMA diese zu einer umsichtigen Ausschüttungspolitik auf.

Was mache ich wenn ich 1’000’000 CHF Nettovermögen erreiche? ???♂️

Was mache ich wenn ich 1’000’000 CHF Nettovermögen erreiche? ???♂️

Diese Frage stelle ich mir tatsächlich sehr selten, aber Bekannte und Freunde fragen gerne mal. Was machst du wenn du die 1‘000‘000 CHF Nettovermögen erreichst? Kaufst du dir dann zur Feier etwas? Meine Antwort ist immer etwas ernüchternd, es geht normal weiter wie bisher, es ist nur eine Zahl.

Tags: Featured,newsletter