Just as the rewards of central-bank bubbles have not been evenly distributed, the pain created by the collapse of the bubbles won’t be evenly distributed, either. We’ve reached an interesting juncture in history, and I don’t mean the pandemic. I’m referring to the normalization of extremes in the economy, in social decay and in political dysfunction and polarization. Let’s ask a very simple question. The S&P 500 stock index went up five-fold from its 2009 low at 667 to a recent high around 3,400. Did your income rise five-fold since 2009? Probably not. Houses that sold for 0,000 in 2000 are now valued at 0,000, a six-fold increase since 2000. Did your income rise six-fold since 2000? Probably not. State university tuition has risen about 2.5 times from

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

Just as the rewards of central-bank bubbles have not been evenly distributed, the pain created by the collapse of the bubbles won’t be evenly distributed, either. We’ve reached an interesting juncture in history, and I don’t mean the pandemic. I’m referring to the normalization of extremes in the economy, in social decay and in political dysfunction and polarization. Let’s ask a very simple question. The S&P 500 stock index went up five-fold from its 2009 low at 667 to a recent high around 3,400. Did your income rise five-fold since 2009? Probably not. Houses that sold for $150,000 in 2000 are now valued at $900,000, a six-fold increase since 2000. Did your income rise six-fold since 2000? Probably not. State university tuition has risen about 2.5 times from 2004 to 2019. Did your income rise 2.5-fold since 2004? Probably not. Even burritos from the local taco truck have tripled in price in the past 15 years. Did your income triple? Probably not. The average household income in 2000 was about $42,000. To match the six-fold increase in urban housing valuations, that household would have to earn $252,000 this year. How many households saw their income soar from $42,000 to $252,000? Not many. The average household income in 2009 was about $50,000. To match the five-fold increase in stock market valuations, that household would have to earn $250,000 this year. How many households saw their income soar from $50,000 to $250,000? Not many. |

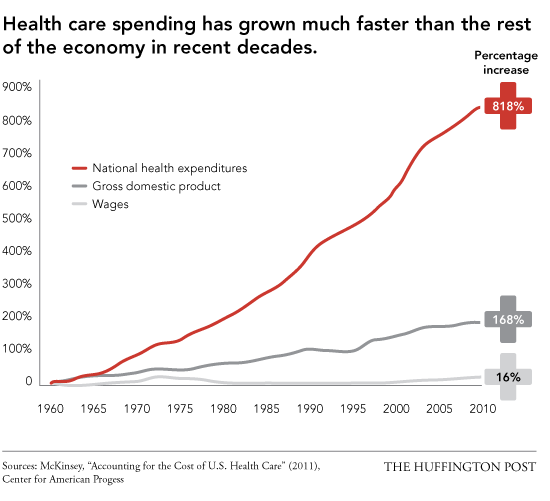

US Health care, 1960-2010 - Click to enlarge |

| To keep up with tuition (never mind healthcare insurance), the household earning $45,000 in 2004 would have to bring home $112,000 this year.

The household earning $100,000 in 2004 would need to boost its income to $250,000 to keep up with college tuition. How many households boosted their income from $100,000 to $250,000 in the past 15 years? Not many. In other words, what’s been normalized over the past 20 years is the total subjugation of labor by central-bank inflated asset bubbles that benefit the top 0.1%. Labor has lost ground while assets have soared, leaving those whose income is earned less able to buy over-valued assets and more prone to borrowing money to maintain their lifestyle– a situation I call debt serfdom. Two generations ago, nobody knew the name of the Federal Reserve’s chairperson. Now that chairperson is in the news virtually daily. The media exposure of the Fed chair far exceeds that of elected officials such as the Speaker of the House of Representatives or the Senate Majority Leader, or the Chief Justice of the Supreme Court. In effect, the nation has become dependent on its central bankers and their limited agenda (expand the wealth and power of the financial sector). The elected government and the real-world production of goods and services both have taken a back seat to conjured “wealth.” The ascendance of finance and the decay of labor’s value is the result of the ascendance of monetary stimulus as the core driver of “wealth” and thus “growth.” It was once expected that consumption would be funded by wages earned by labor, and investment would be funded by savings set aside from earnings. That era is long past. What’s been normalized is a systemic reliance on debt to fund consumption and on the euphoric “animal spirits” of the wealth effect generated by soaring assets such as homes and stocks. History offers a number of parallels to the ascendance of borrowed capital over labor and central bank money-printing over the creation of productive value. History suggests eras that have normalized economic and financial extremes–extremes of inequality, policy, and decay–haven’t ended well for anyone. Just as the rewards of central-bank bubbles have not been evenly distributed, the pain created by the collapse of the bubbles won’t be evenly distributed, either. |

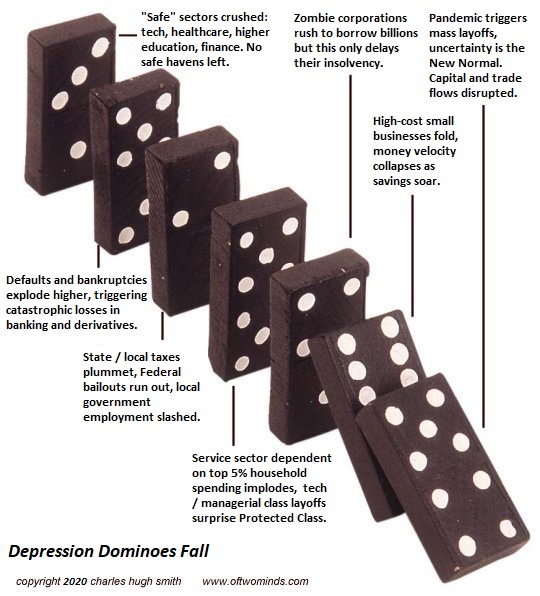

The Fruit of Financialization - Click to enlarge |

You Might Also Like

The Illusion of Control: What If Nobody’s in Charge?

The Illusion of Control: What If Nobody’s in Charge?

The last shred of power the elites hold is the belief of the masses that the elites are still in control. I understand the natural desire to believe somebody’s in charge: whether it’s the Deep State, the Chinese Communist Party, the Kremlin or Agenda 21 globalists, we’re primed to believe somebody somewhere is controlling events or pursuing agendas that drive global responses to events.

Is Data Our New False Religion?

In the false religion of data, heresy is asking for data that is not being collected because it might reveal unpalatably unprofitable realities. Here’s how every modern con starts: let’s look at the data. Every modern con starts with an earnest appeal to look at the data because the con artist has assembled the data to grease the slides of the con.

Forget the V, W or L Recovery: Focus on N-P-B

Forget the V, W or L Recovery: Focus on N-P-B

The only realistic Plan B is a fundamental, permanent re-ordering of the cost structure of the entire U.S. economy. The fantasy of a V-shaped recovery has evaporated, and expectations for a W or L-shaped recovery are increasingly untenable. So forget V, W and L; the letters that will shape the future are N, P, B: there is No Plan B.

Dancing Through the Geopolitical Minefield

Dancing Through the Geopolitical Minefield

The elites dancing through the minefield all have plans, but how many are prepared for the punch in the mouth? Open any newspaper from the past 100 years and you will soon find a newsworthy geopolitical hotspot or conflict.

There are some indexing events this week that could add to market volatility; the IMF will release updated global growth forecasts Wednesday. The regional Fed manufacturing surveys for June will continue to roll out; Fed speaking engagements are somewhat limited this week.

There were minimal changes to the status quo as the week commences. Bangladesh has announced revised trading hours on the local exchanges. No change of status in Nigeria and Kenya as they both continue to face limited liquidity. Please see trading comments below.

Dollar Firm as Risk-Off Sentiment Returns

Dollar Firm as Risk-Off Sentiment Returns

Risk-off sentiment has picked up from reports that the US will impose new tariffs against the EU; there’s also been a messy set of headlines regarding the virus contagion outlook in the US. The IMF will release updated global growth forecasts today; the dollar is benefiting from risk-off sentiment; another round of fiscal stimulus in the US is in the works.

Recent Trade Developments Suggest Some Caution Ahead Warranted

Recent Trade Developments Suggest Some Caution Ahead Warranted

There’s never a good time for a trade war. Yet here we are on the cusp of one between the US and the EU over unfair aircraft subsidies and comes at a time when renewed COVID-19 outbreaks are making the global economic outlook even cloudier. These developments suggest some caution ahead is warranted for risk assets like EM and equities.

Tags: Featured,newsletter