Extrapolating The Recent Past Can Be Hazardous To Your Wealth “Those who cannot remember the past are condemned to repeat it,” remarked George Santayana over 100 years ago. These words, as strung together in this sequence, certainly sound good. But how to render them to actionable advice is less certain. Aren’t some facets of the past – like the floppy disk – not worth remembering? And aren’t others – like a first taste of romance – worth repeating… if only it were possible? Where investing is concerned, remembering the past – and discerning what to make of it – can actually be a handicap. Where does the past begin? How does it influence the future? How does one invest one’s capital accordingly? These are

Topics:

MN Gordon considers the following as important: 6) Gold and Austrian Economics, 6b) Austrian Economics, Bill Gross, Featured, George Santayana, newsletter, On Economy, On Politics

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Extrapolating The Recent Past Can Be Hazardous To Your Wealth“Those who cannot remember the past are condemned to repeat it,” remarked George Santayana over 100 years ago. These words, as strung together in this sequence, certainly sound good. But how to render them to actionable advice is less certain. Aren’t some facets of the past – like the floppy disk – not worth remembering? And aren’t others – like a first taste of romance – worth repeating… if only it were possible? Where investing is concerned, remembering the past – and discerning what to make of it – can actually be a handicap. Where does the past begin? How does it influence the future? How does one invest one’s capital accordingly? These are today’s questions. What follows, with purpose and intent, is an attempt to scratch out an answer. Where to begin? Many investment gurus in the early 1980s were predicting the future while projecting the past. After a decade of raging price inflation, the popular dogma was to pack one’s portfolio with gold coins, fine art, and antiques. This was the proven, surefire way to preserve hard earned wealth. The United States, remember, was just a year or two away from going full Weimar Republic circa 1921-23. The dollar was going to quickly turn to hyper-inflationary ash, like conifer trees in a California wildfire. Everyone just knew it. You could darn near count down the days. |

George Santayana – purveyor of eminently quotable wise words by the wagon-load, but what shall one do with them in practice? [PT] |

Right On The MoneyConventional wisdom, when it comes to the economy, markets, and investing, eventually leads to trouble. While everyone is busy watching the status quo unfold with Swiss watch like precision, the conditions that first brought this state of affairs to fruition subtly changes. Yet almost no one takes notice. In the late 1970s, A. Gary Shilling had a hunch. Rather than the consensus view that inflation would persist forever, Shilling suspected that the U.S. was entering a long-term era of lower and lower rates of price inflation – and an equally long-term decline in interest rates. Under this backdrop, traditional inflation hedges would be disastrous. Shilling, having conviction and wanting to warn investors, wrote a book about his insight. The book was first published in the early 1980s, and its title asked two significant questions: Is Inflation Ending? Are You Ready? The book’s sales were an utter flop. No one, save a handful of shrewd individuals, could actually fathom that price inflation was dissipating. But the book’s forecast was right on the money. In September of 1981, 20-year Treasury Note yields peaked at 15.32 percent. After that, they commenced a 35 year decline that likely ended in July 2016 at just 1.5 percent. Shilling, in addition to his book, also put his money behind his convictions. By the mid-1980s Shilling achieved financial independence through aggressive investment in the long bond. Shilling’s big forecast and financial windfalls were recounted in John Mauldin’s 2006 book, Just One Thing. |

US 30-year treasury bond yield, 1942 – present day.(see more posts on US Treasury, ) At the height of the late 1970s inflation scare a great time to buy bonds had arrived. - Click to enlarge |

Is Inflation Beginning? Are You Ready?Shilling’s astute call and capital deployment into the long-term decline in interest rates starting in the early 1980s is remarkable. But what is also remarkable is Shilling’s ability to successfully ride out this trend long after other big investors bailed out. Bill Gross, the bond king, was also one of the early savants to recognize and exploit this trend. Employing the total return bond strategy that he pioneered, Gross built Pimco into a $1.7 trillion money manager and amassed his own personal fortune. But in the decade that followed the Great Financial Crisis, Gross lost his magic touch. Between a bitter public confrontation with colleague Mohamed El-Erain and emitting cans of fart spray in his ex-wife’s Laguna Beach home (and formerly his home), Gross heavily bet against the price of U.S. government debt. This mistake marked the beginning of the end of Gross’ otherwise notable career, which officially ended last month. |

Former “bond king” Bill Gross, lately better known as a vengeful wielder of canned flatulence [PT] |

Shilling, however, has continued his propensity for predicting turns in the economy. And he’s going on record again. In a recent Bloomberg article, Shilling offered the following:

How Shilling derived a two-thirds probability of a business downturn starting this year is a question of methodology. We put the probability of a business downturn starting this year at three-thirds – or 100 percent. But it is what comes after which you should keep a watchful eye on. At the moment, bad news for the economy is good news for stocks. The conventional wisdom is that a weakening economy ensures more stimulative juice from the Fed. Without question, and as demonstrated by the Fed’s decision this week to hold rates steady, the Fed can be counted on to comply. But when days darker than the darkest days of a decade ago arrive, and the Fed comes to the rescue with helicopter money drops, something unexpected will happen. Rather than bond yields falling and stock prices rising, the opposite will happen. Stock prices will fall and interest rates will rise, along with consumer prices. Is Inflation Beginning? Are you ready? These questions may seem absurd today. Tomorrow their answers will be obvious. Having a gold coin or two in hand when tomorrow arrives will be of critical importance. |

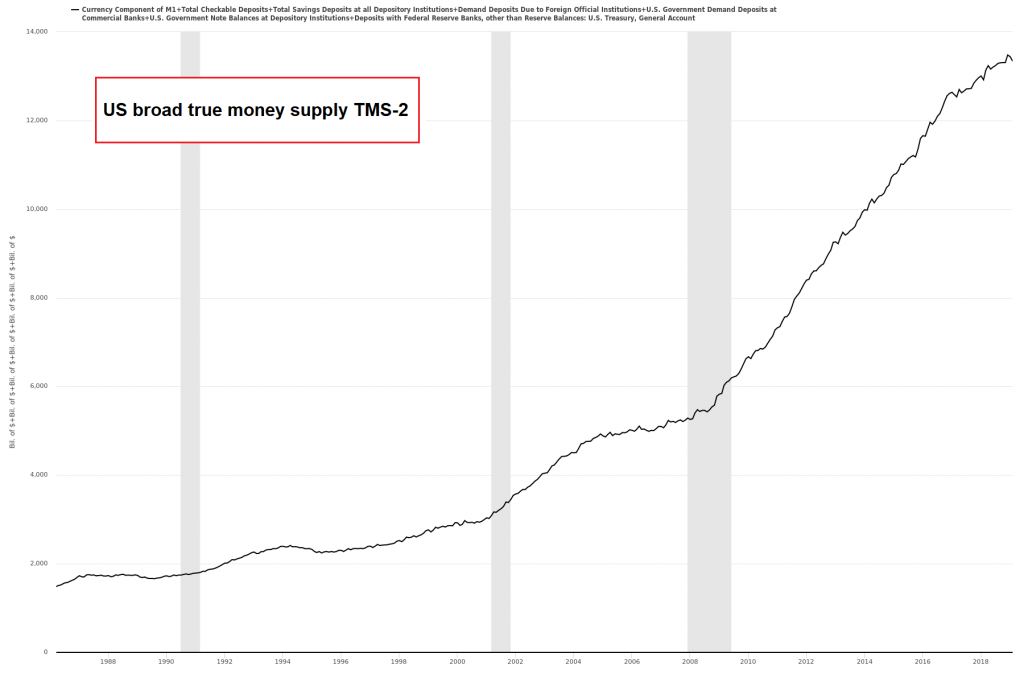

US money supply TMS-2, 1988-2019 US money supply TMS-2: using the (correct) classical definition of “inflation” as an increase in the money supply, it has arrived long ago. [PT] - Click to enlarge |

Charts by: StockCharts, St. Louis Fed

Chart and image captions by PT

Tags: Bill Gross,Featured,George Santayana,newsletter,On Economy,On Politics