The Federal Reserve’s confidence in the economy and its need to continue to gradually increase interest rates stands in sharp contrast to most of the other major central banks. The European Central Bank will finish its asset purchases at the end of the year, but it is in no position to begin to normalize interest rates. Indeed, the risk is that it may feel compelled to off another Targeted Long-Term Repo, which would, in effect, allow the borrowers to extend the maturities of existing funds. The dramatic drop in oil prices–20% since early October’s four-year highs–will, if sustained, dampen headline inflation, making it more difficult for some countries to raise interest rates. In the US, it may be experienced like a

Topics:

Marc Chandler considers the following as important: 4) FX Trends, Brexit, China, equities, Featured, Federal Reserve, GBP, newsletter, Oil, SPX, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The Federal Reserve’s confidence in the economy and its need to continue to gradually increase interest rates stands in sharp contrast to most of the other major central banks. The European Central Bank will finish its asset purchases at the end of the year, but it is in no position to begin to normalize interest rates. Indeed, the risk is that it may feel compelled to off another Targeted Long-Term Repo, which would, in effect, allow the borrowers to extend the maturities of existing funds. The dramatic drop in oil prices–20% since early October’s four-year highs–will, if sustained, dampen headline inflation, making it more difficult for some countries to raise interest rates. In the US, it may be experienced like a tax break that boosts discretionary household spending and extends the business cycle.

Some critics blame Fed Chair Powell for scaring market participants by noting last month that was monetary policy was still accommodative, and there was some distance before neutrality was reached. Should we really harken back to the good old days, when Fed Chair Greenspan purposely sought to obfuscate? Legend has it that he had a sign in his office that said, “If you think you understood what I said, you misunderstood.”

United StatesThe Fed has been clear. Four hikes are likely this year and three next. The market is not persuaded. In fact, interpolating from the fed funds futures strip, the market is not convinced the Fed will raise rates more than two more times. In some ways, this is nothing new. Throughout this cycle, Fed officials often have had to lead the market by the nose help it prepare for an imminent hike. In any, even the market is largely pricing in a rate increase next month and another one in Q1 19. During this period, of the major central banks, only the Bank of Canada and Sweden’s Riksbank are likely to hike rates. To be sure, the divergence in monetary policy reflect economic and/or financial differentiation. Consider industrial output figures that the US, EMU, and Japan will report in the coming days. Through September, US industrial production has increased by a monthly average of almost 0.3%. It is expected to have risen by 0.2% in October. EMU’s September IP is expected to have also risen by 0.2%, but it has averaged a 0.2% decline in the first eight months of the year. |

Economic Events: United Stetes, Week November 12 - Click to enlarge |

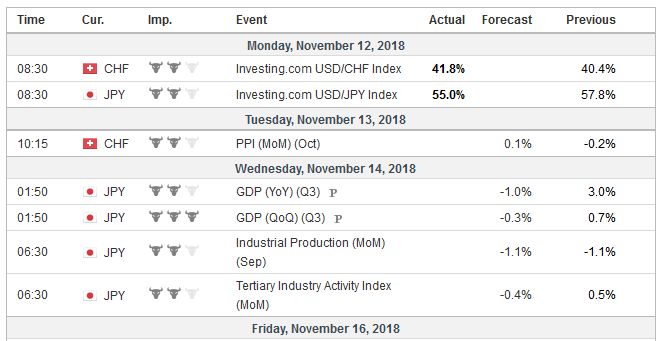

JapanJapan will report a final September industrial output figure. Using preliminary data, including the 1.1% contraction in September, Japan’s IP has fallen by an average of 0.4% this year. Before the outsized decline in September, which appears a function of natural disasters, industrial. |

Economic Events: Japan, Week November 12 - Click to enlarge |

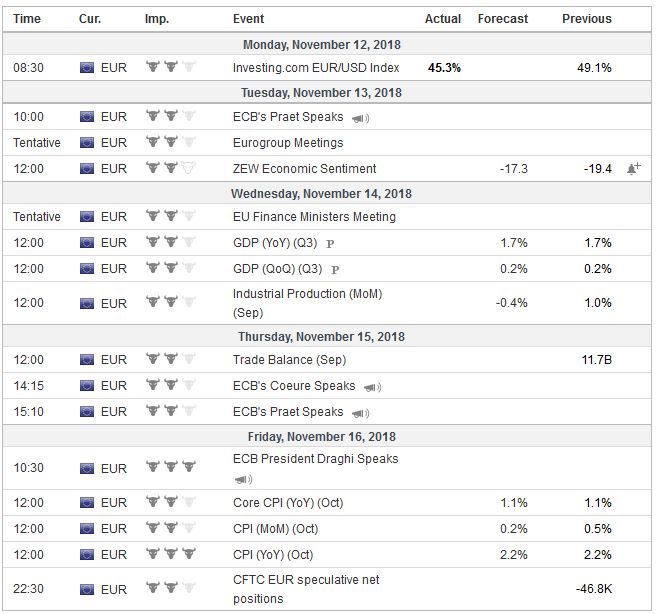

EurozoneSeparately, the eurozone is expected to confirm that Q3 GDP rose 0.2%. This follows a 0.4% expansion in Q1 and Q2. Last year, the eurozone economy expanded by 0.7% each quarter. Growth in the past three quarters is the slowest since 2014. |

Economic Events: Eurozone, Week November 12 - Click to enlarge |

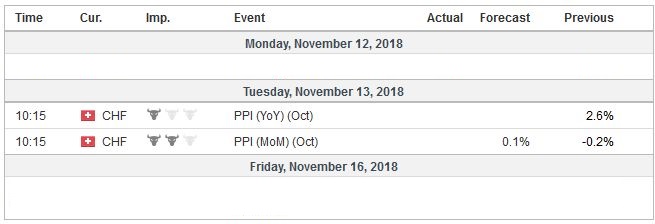

Switzerland |

Economic Events: Switzerland, Week November 12 - Click to enlarge |

The 20% collapse in the price of oil, if sustained, will have far-reaching implications for the investment climate. The combination of softer growth and a major headwind on prices (though a weaker euro exchange rate can blunt this) may encourage investors to think twice about the 10 bp hike after next summer that has been mostly discounted (via OIS).

Some in the US who are critical of the Fed’s course will argue that the likely lower inflation expectations that will result means that real interest rates are may be higher than assumed that the Fed risks a policy mistake that leads to a recession. However, there is a compelling reason why for policy purposes the Fed targets prices excluding food and energy. Over the past half-century or so, it appears that headline inflation converges to core inflation, not the other way around. Officials in the US are more likely to see the decline in oil prices is the rough equivalent of a tax cut that could boost discretionary spending.

The driver for the decline in oil prices is important in assessing its significance. The soft European and Japanese industrial output, coupled with the slowing of the Chinese economy suggests there has been some weakening of demand. However, that has been a gradual process, and the decline has been sharp after reaching four-year highs in early October.

Rather than demand, supply factors seem paramount. All three of the world’s largest producers, the US, Russia, and Saudi Arabia are producing record amounts of oil. OPEC’s second largest producer, Iraq, has announced plans to continue to boost capacity. The EIA boosted its forecasts for US oil output this year (10.9 mln bpd vs. 9.35 mln bpd in 2017). The estimate of next year’s output was lifted to 12.06 mln barrels from 11.76 previously. Half of the oil the US produced in the first week of November appears to have been stored (rising inventories). Russia is producing more oil since the Soviet Union era. Encouraged by the US, Saudi Arabia boosted output to what appears to be a record.

OPEC met on November 10. Estimates suggest that member countries have “over-complied” with earlier agreements to cut output. The technical arm of OPEC estimated that OPEC production was October was four percent less than agreed, despite the increase in Saudi output. In September, production was 11% less than agreed. The goal apparently is to be 100% compliant, which would still increase supply. However, the real signal is that a consensus appears to be forming among OPEC towards a cut in output next year of around one million barrels a day. A formal decision is possible next month, though Saudi Arabia is signaled intentions on cutting oil exports by as much as 500k bpd next month. Russia has not shown its hand, but the Saudi’s move may help support prices in the days ahead. This may boost prices, which after a 10-day and a five-week losing streak, were technically over-extended. The weekend decision could provide the fundamental impetus of the technical bounce we anticipated.

The collective wisdom in the market favors two compromises–one between the US and China on trade later this month when Trump and Xi meet, and the other is on Brexit. On both scores, we are not as convinced and suspect the opposite is increasingly likely. The risk is that many investors have been too ready to dismiss the US rhetoric (Trump, Pence, Pompeo, and Navarro) as bombastic but part of the negotiating strategy, which has been seen before. Brexit negotiations seem like a classic scissors dilemma. The closer one side gets (e,g., the UK and EU) the further the other side widens (May and Parliament).

Indeed, the risks of May’s strategy is that she fails to satisfy both the EU and Parliament. That is what appears to be emerging now, and this will likely weigh on sterling next week, after a poor close before the weekend when it finished below $1.30 for the first time last week. The UK Transportation Minister (J. Johnson) resigned, and four other cabinet ministers are considering resigning according to press reports in protest of May’s plan. Over the weekend, senior EU officials rejected May’s plan for an independent mechanism to see how the UK could exit the backstop if Brexit talks fail. A break of the $1.2940 area could signal a return to $1.2660 the lows for year seen at the end of last month.

In three different fronts, the US policy is disruptive. First, the US policy mix is sucking in the world’s savings, making it more difficult to other current account deficits to be funded smoothly. The cost of hedging US bond exposure has spurred a cottage industry of journalists and analysts bemoaning the lack of foreign interest. We resisted such arguments as being short-sighted and under-appreciating the dynamism of global investors.

The August TIC data showed the strongest foreign demand for long-term US assets (~$132 bln) since September 2014, which itself appear to have been a record. The performance in September, which the TIC report out at the end of the week may not match August’s strong showing. US 10-year yields rose by more than 20 bp over the course of the month, and US equities were flat (+0.4%). On the other hand, Japanese balance of payments data, out last week, showed Japanese investors bought $20 bln of US bonds in September, and at least two life insurers announced intentions to boost unhedged purchases of foreign bonds.

Second, the US embargo against Iran is disruptive. The exemptions are for a limited time and many countries, not wanting to incur the US wrath have also begun the adjustment process. News that the SWIFT will honor the embargo, as it did before, demonstrates the US ability and willingness to press its advantage. However, SWIFT was thought of a utility function, and the US policies that have it act as a policy arm spurs hard feelings and the drive for an alternative, which of course will take some time to achieve, the rhetoric (e.g., France) is running ahead of capabilities.

Third, the US aggressive trade stance is also disruptive. NATFA 2.0 is nearly ready to be signed as the last minute details are worked out. The US reportedly is still pressing for additional concessions, and this may have weighed on the Canadian dollar at the end of last week. However, the focus is on US-China trade. Both sides are taking measures to cope with a prolonged confrontation. The risk that it is indeed the leading edge of a new cold war does not seem to be taken with sufficient seriousness by investors.

There is a camp that wants this to simply be about the trade imbalance, and many are hopeful of a deal. Navarro, Trump’s top trade adviser made pointed comments and seem to strike back at some thinly-veiled criticism by former White House economic adviser Cohn. Navarro that if a deal were worked out later this month, it would have the “imprimatur of Goldman Sachs.” He said that “globalist billionaires” were adding pressure on Trump to compromise, and if he did, the agreement would have a “stench around it.” Navarro stopped just short of calling this “full court press” treasonous for being part of China’s “influence operation.”

After dramatic falls in October, most equity markets have begun November on firmer footing. The MSCI Emerging Markets Index is fell 2% last week, which trimmed the previous week’s 6% gain. The MSCI World Index (developed countries) gained 1.3% last week on top 2.7% the previous week. The US S&P 500 rose 2.1% last week after 2.4% the previous week. However, all three benchmarks fell in the second half of last week.

The S&P 500 fell almost 1% before the weekend to test the 200-day moving average after gapping above it the day after the US election and the day before the outcome of the FOMC meeting. That gap was entered but not filled (it extends to about 2756.8). The S&P 500 gapped lower ahead of the weekend. The gap is small (~2794.1-2795.0), but the size of the gap in technical theory then where it takes place and whether it is closed relatively quickly.

We suspect part of the sell-off in several popular US tech names was a function of both S&P and MSCI rejigging their industry classifications to combine internet and media companies into a”communication sector” weighed on benchmarks. Rising interest rates, and ideas that earnings growth is may be near a cyclical peak probably played a role as well. The drop in oil prices represents a shift from producers to consumers. While the firm close to the S&P500 before the weekend despite the loss, investors will want to to see what happens at the start of the week before making new commitments.

Tags: #GBP,#USD,Brexit,China,equities,Featured,Federal Reserve,newsletter,OIL,SPX