Jeffrey P. Snider

May 10, 2018

SNB & CHF

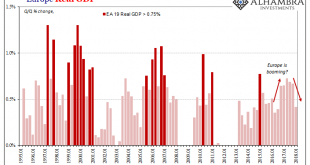

The primary example of globally synchronized growth has been Europe. Nowhere has more hope been attached to shifting fortunes. The Continent, buoyed by the persistence of central bankers like Mario Draghi, has not just accelerated it is actually booming. Or so they say.

Last September, politicians were lining up to confidently declare as much, often deploying that specific word.

When Jean-Claude Juncker gave his annual...

Read More »

Joseph Y. Calhoun

May 9, 2018

SNB & CHF

The yield on the 10 year Treasury note briefly surpassed the supposedly important 3% barrier and then….nothing. So, maybe, contrary to all the commentary that placed such importance on that level, it was just another line on a chart and the bond bear market fear mongering told us a lot about the commentators and not a lot about the market or the economy. As I said last month, despite the recent run up in rates, the...

Read More »

Jeffrey P. Snider

May 1, 2018

SNB & CHF

Thomas Hoenig was President of the Federal Reserve’s Kansas City branch for two decades. He left that post in 2011 to become Vice Chairman of the FDIC. Before that, Mr. Hoenig as a voting member of the FOMC in 2010 cast the lone dissenting vote in each of the eight policy meetings that year (meaning he was against QE2, too). This makes him, apparently, the hawk of all hawks.

In January 2011, in his capacity as still...

Read More »

Jeffrey P. Snider

April 28, 2018

SNB & CHF

The term itself gives it away. They called it quantitative easing for a specific reason. Both words mean to convey substantial concepts.

The first part, quantitative, was used because it sounds deliberate, even scientific. It implies a program where great care and study was employed to come up with the exact right amount. It’s downright formulaic, where you intend that by doing X you can predictably create Y.

The...

Read More »

Joseph Y. Calhoun

April 27, 2018

SNB & CHF

How quickly things change in these markets. In the report two weeks ago, the markets reflected a pretty obvious slowing in the global economy. In the course of two weeks, what seemed obvious has been quickly reversed. The 10-year yield moved up a quick 20 basis points in just a week, a rise in nominal growth expectations that was mostly about inflation fears. The economic news over the last two weeks does not appear to...

Read More »

Jeffrey P. Snider

April 26, 2018

SNB & CHF

Beginning with its very first issue in May 1915, the Federal Reserve’s Bulletin was the place to find a growing body of statistics on US economic performance. Four years later, monthly data was being put together on the physical volumes of trade. From these, in 1922, the precursor to what we know today as Industrial Production was formed.

The index and its components have changed considerably over its near century of...

Read More »

Jeffrey P. Snider

April 22, 2018

SNB & CHF

Retail sales rose (seasonally adjusted) in March 2018 for the first time in four months. Related to last year’s big hurricanes and the distortions they produced, retail sales had surged in the three months following their immediate aftermath and now appear to be mean reverting toward what looks like the same weak pre-storm baseline. Exactly how far (or fast) won’t be known until subsequent months.

US Retail Sales, Jan...

Read More »

Marcelo Perez

April 20, 2018

SNB & CHF

[embedded content]

Related posts: Global Asset Allocation Update: The Certainty of Uncertainty

Why Trade Wars Ignite and Why They’re Spreading

The Genie’s Out of the Bottle: Eight Defining Trends Are Reversing

Bi-Weekly Economic Review: Investing Is Not A Game of Perfect

US-China Trade War Escalates As Further Measures Are Taken

Less Retail Jobs,...

Read More »

Jeffrey P. Snider

April 19, 2018

SNB & CHF

Last month Chinese trade statistics left us with several key questions. Export growth was a clear outlier, with outbound trade rising nearly 45% year-over-year in February 2018. There were the usual Golden Week distortions to consider, made more disruptive by the timing of it this year as different from last year. And then we have to consider possible effects of tariffs and restrictions at the start of what is called a...

Read More »

Joseph Y. Calhoun

April 18, 2018

SNB & CHF

There is no change to the risk budget this month. For the moderate risk investor, the allocation to bonds is 50%, risk assets 45% and cash 5%. Stocks continued their erratic ways since the last update with another test of the February lows that are holding – for now. While we believe growth expectations are moderating somewhat (see the Bi-Weekly Economic Review) the change isn’t sufficient to warrant an asset...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org