Swiss Economicblogs.org

Swiss Economicblogs.org

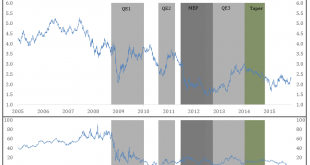

SWAP spreads recently took a nosedive and are once again trading at negative levels, even for shorter maturities. As can be seen from the chart below, treasury yields, here represented by the 10 year maturity, rose during QE policies programs contradicting the very raison d’être spouted by the central bankers. Interestingly enough we also see the same pattern in SWAP spreads. As QE programs were enacted SWAP spreads started to move upwards, just to rollover as the central bank program...

Read More »What a Negative SWAP Spread Really Means