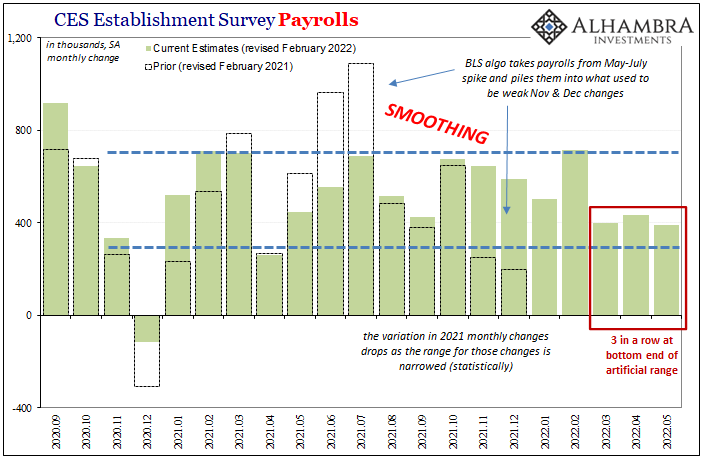

The BLS’s most recent labor market data is, well, troubling. Even the preferred if artificially-smooth Establishment Survey indicates that something has changed since around March. A slowdown at least, leaving more questions than answers (from President Phillips). That as much because of the other employment figures, the Household Survey. April and May, in particular, not just a slowdown but a drop in overall employee count. As I pointed out last Friday, a 2-month negative is highly unusual except when the US already experiencing serious weakness, downturn, maybe more. . Given these, it might be time to revisit jobless claims and unemployment insurance. Quite unlike the unemployment rate, the number of American workers who are filing for initial verification of

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, consumer spending, currencies, economy, employment, Featured, Federal Reserve/Monetary Policy, inflation, Inventory, jobless claims, Labor market, Markets, newsletter, unemployment insurance, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The BLS’s most recent labor market data is, well, troubling. Even the preferred if artificially-smooth Establishment Survey indicates that something has changed since around March. A slowdown at least, leaving more questions than answers (from President Phillips).

That as much because of the other employment figures, the Household Survey. April and May, in particular, not just a slowdown but a drop in overall employee count. As I pointed out last Friday, a 2-month negative is highly unusual except when the US already experiencing serious weakness, downturn, maybe more. |

. |

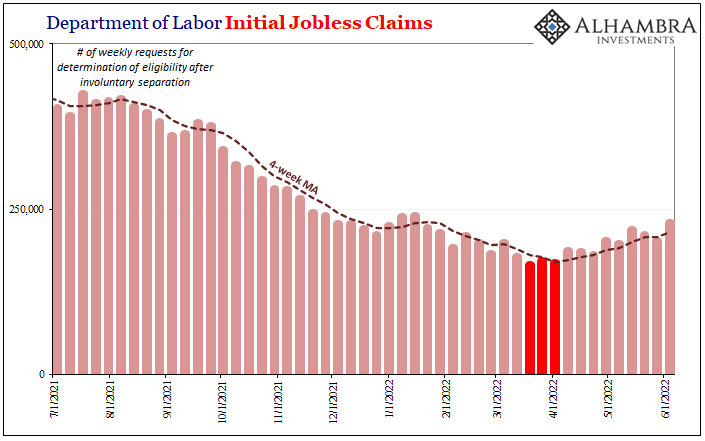

| Given these, it might be time to revisit jobless claims and unemployment insurance. Quite unlike the unemployment rate, the number of American workers who are filing for initial verification of involuntary separation so as to claim insurance benefits has been rising…since March and April. |

. |

| The weekly totals are still extremely low, having dropped to historic lows prior – if only because pretty much the entire American population had exhausted every last benefit. While it might be easy to dismiss claims at less than 250,000 per week, it’s not the level rather the direction and the timing of what may be (so far has been) a hard inflection (especially as it corresponds so closely to other data and more).

It’s the second derivative which stands out here, the clear change in trajectory which so far has lasted several months (ruling out random fluctuation, statistical error, though not yet conclusive). |

. |

| These particular several months:

Rate hikes to blame? Jobless claims bottomed out right about when the FOMC’s first (half) rate action took place. Now that would be some precise timing. |

. |

| Though the Fed Cult would love to stake Jay Powell’s claim to this, trying desperately to carve the Chairman’s face next to the unearned statue of Volcker, even its members can’t sell this pure coincidence. A single 25 bps rate hike from zero (25bps upper bound) would never, in any universe, cause a rip-roaring inflationary economy operating a max employment to suddenly go into so serious a reverse.

This forces them to choose between presumed rate hike power and admitting the economy isn’t all that great, which would undercut the justification for rate hikes. The other explanation more and more put forward is the benign-sounding end of “pandemic spending” on the part of consumers. That wouldn’t sell jobless claims let alone Establishment and Household Surveys of softness. It barely counts for what retailers are doing with their ungodly levels of inventory (Target will only be the first). Besides, below doesn’t sound like Americans shifting their spending habits back toward normal, presuming before 2020 was normal. It sounds exactly like broad-based, economy-harming retrenching:

|

. |

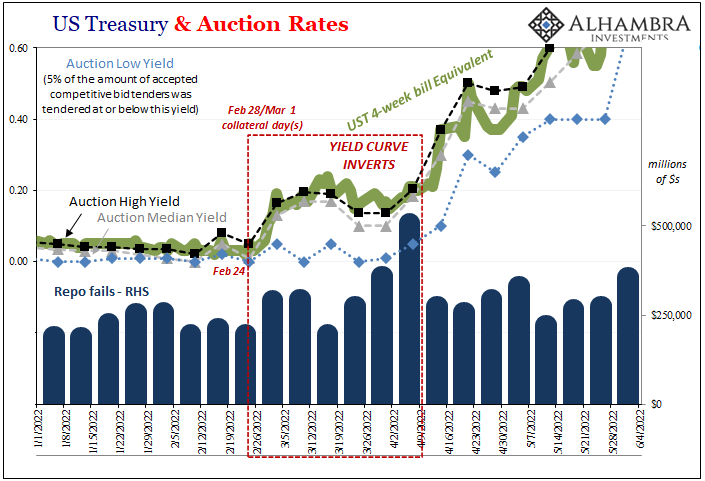

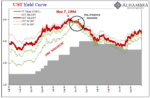

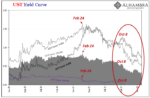

| This BMO/Harris survey from the end of May, like jobless claims, pictures a serious amount of distress which can be more closely associated with gasoline meaning oil prices finally going a step (or two) too far. When? March.

Remember March was also the month filled with the major financial fireworks, Treasury curve inversion to go with ridiculously low T-bill rates meaning monetary tightening in a very real sense the Fed’s rate hikes can only jealously envy. It all went down in March, which now seems to mean jobless claims going up. Rather than the FOMC, the markets just may have nailed the economy’s (and it’s more than just this, remember Target and Walmart, applying far wider to more than just America) transition from weak but still reopening rebound to, perhaps, more squarely recession dynamics. It sure seems so to this point. Confirmation, of course, still required and pending. While any honest inquiry will take that possibility very seriously, the politics of rate hike theater will continue without doing so for the foreseeable future, for as long as possible (repeating the same pattern like policy cycles of the recent past). Yet, even that future is in doubt, markets very much trying to judge just how bad it might get before the theater closes its run for lack of audience. Unfortunately for Jay, more so the world, it all continues to add up. And the math just isn’t inflationary. Never was. |

. |

You Might Also Like

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.

2022-06-06

The fact that German retail sales crashed so much in April 2022 is significant for a couple reasons. First, it more than suggests something is wrong with Germany, and not just some run-of-the-mill hiccup. Second, because it was this April rather than last April or last summer, you can’t blame COVID this time.

Is It Recession?

Is It Recession?

2022-04-30

According to today’s advance estimate for first quarter 2022 US real GDP, the third highest (inflation-adjusted) inventory build on record subtracted nearly a point off the quarter-over-quarter annual rate. Yes, you read that right; deducted from growth, as in lowered it. This might seem counterintuitive since by GDP accounting inventory adds to output.

Not Good Goods

Not Good Goods

2022-04-24

The goods economy in the United States is – maybe was – the lone economic bright spot. That in and of itself should’ve provoked more caution, instead there was the red-hot recovery to sell under the cover of supply shock pricing changes. The sheer spending on goods, and how they arrived, each unabashedly artificial from the get-go.

The Short, Sweet Income Case For Ugly Inversion(s), Too

The Short, Sweet Income Case For Ugly Inversion(s), Too

2022-04-04

A nod to just how backward and upside down the world is now. The economic data everyone is made to pay attention to, payrolls, that one is, in my view, irrelevant. As is the consumer price estimates from earlier this week, the PCE Deflator. That’s another one which receives vast amounts of interest even though it is already old news.

We Can Only Hope For Another (bond) Massacre

We Can Only Hope For Another (bond) Massacre

2022-03-30

To begin with, the economy today is absolutely nothing like it had been almost thirty years ago. That fact in and of itself should end the discussion right here. However, comparisons will be made and it does no harm to review them.I’m talking about 1994, or, more specifically, the eleven months between late February 1994 and early February 1995.

Inversion Is The Real March Madness, Just Don’t Take It Literally

Inversion Is The Real March Madness, Just Don’t Take It Literally

2022-03-22

With such low levels of self-awareness, it isn’t surprising that the FOMC’s members continue to pour gasoline on the already-blazing curve fire. March Madness is supposed to be on the courts of college basketball, instead it is playing out more vividly across all financial markets.

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

2022-01-29

The first time I can consciously remember using the term landmine was probably here in February 2019. I had described the same process play out several times before, I had just never applied that term. There was all sorts of market chaos in the final two months of 2018, including a full-on stock market correction, believe it or not, leaving the inflation and recovery narrative in near complete tatters.

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**

2022-01-28

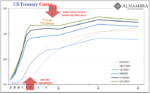

It’s not hard to reason why there continues to be this conflict of interest (rates). On the one hand, impacting the short end of the yield curve, the unemployment rate has taken a tight grip on the FOMC’s limited imagination. The rate hikes are coming and the markets like all mainstream commentary agree that as it stands there’s nothing on the horizon to stop Jay Powell’s hawkishness.

Tags: Bonds,consumer spending,currencies,economy,employment,Featured,Federal Reserve/Monetary Policy,inflation,Inventory,jobless claims,Labor Market,Markets,newsletter,unemployment insurance,Yield Curve