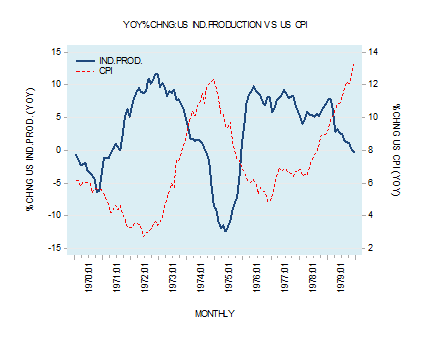

The occurrence of stagflation is associated with a situation of general strengthening in the momentum of prices while at the same time the pace of economic activity is declining. A famous stagflation episode occurred during the 1974û75 period, as year-on-year industrial production fell by nearly 13 percent in March 1975 while the yearly growth rate of the Consumer Price Index (CPI) jumped to around 12 percent. Likewise, a large fall in economic activity and galloping price inflation was observed during 1979. By December of that year, the yearly growth rate of industrial production stood close to nil while the yearly growth rate of the CPI closed at over 13 percent. According to popular thinking of that time, the central bank influences the pace of economic

Topics:

Frank Shostak considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The occurrence of stagflation is associated with a situation of general strengthening in the momentum of prices while at the same time the pace of economic activity is declining. A famous stagflation episode occurred during the 1974û75 period, as year-on-year industrial production fell by nearly 13 percent in March 1975 while the yearly growth rate of the Consumer Price Index (CPI) jumped to around 12 percent. Likewise, a large fall in economic activity and galloping price inflation was observed during 1979. By December of that year, the yearly growth rate of industrial production stood close to nil while the yearly growth rate of the CPI closed at over 13 percent.

According to popular thinking of that time, the central bank influences the pace of economic expansion through monetary policies. This influence however, carries a price, which is inflation. Many economists believe that if the goal is to reach a faster rate of economic growth and a lower unemployment rate, then citizens should be ready to experience higher rates of inflation. The belief was that there is a tradeoff between inflation and unemployment. The lower the unemployment rate, the higher is the rate of inflation. Conversely, the higher the unemployment rate the lower the rate of inflation is going to be. The stagflation of 1970s, then, was a big surprise to most economic commentators. In the late 1960s, Edmund Phelps and Milton Friedman (P-F) challenged the popular view that there can be a sustainable tradeoff between inflation and unemployment. In fact, over time, according to P-F, loose central bank policies set the platform for lower economic growth and a higher rate of inflation; i.e., stagflation. |

. |

The P-F Explanation of Stagflation

Starting from a situation of equality between the current and the expected rate of inflation, the central bank decides to boost the rate of economic growth by raising the growth rate of money supply. As a result, a greater supply of money enters the economy and each individual now has more money at his disposal. Because of this increase, every individual believes he has become wealthier. This raises the demand for goods and services, which in turn sets in motion an increase in the production of goods and services.

This increases producers’ demands for workers and, subsequently, unemployment falls below the equilibrium rate, which both Phelps and Friedman labeled the natural rate. Once the unemployment rate falls below the equilibrium rate, this exerts upward pressure on price inflation. According to P-F, individuals realize there has been a general loosening of the money supply, so people form higher inflation expectations, and individuals realize that their previous increase in purchasing power now is dwindling.

This weakens overall demand for goods and services which, in turn, weakens overall demand, which then slows production of goods and services, pushing unemployment higher. Note that we are now back with respect to unemployment and economic growth to where we were prior to the central bank’s decision to loosen its monetary stance, but now with a much higher rate of inflation.

Consequently, we have a decline in production of goods and services and a rise in unemployment, along with an increase in price inflation: stagflation. From this, P-F concluded that as long as the increase in the money supply growth rate is unexpected, the central bank can engineer an increase in the rate of economic growth.

However, once people learn about the increase in the money supply and assess the implications of this increase, they adjust their conduct accordingly. Not surprisingly, the temporary boost to the economy from the increase in the money supply disappears. In order to overcome this hurdle and strengthen the rate of economic growth, the central bank would have to surprise individuals through a much higher pace of monetary pumping.

However, after a time lag, people learn about this increase and adjust their conduct accordingly. Consequently, the effect of the higher growth rate of money supply on the economy will likely vanish again and a much higher inflation rate is all that remains. From this, P-F concluded loose monetary policies can only temporarily generate economic growth, and over time, such policies will result in higher price inflation. Thus, according to P-F, there is no long-term tradeoff between inflation and unemployment.

Money Supply Increases Always Undermine Growth

In a market economy, a producer exchanges his product for money and then exchanges that money for other products. Alternatively, we can say that exchanges of something for something take place by means of money. Also, in order for the exchange among producers to take place, these producers must have produced useful goods and services.

However, things are different once money is generated out of “thin air” due to central bank policies and fractional reserve banking. Once money out of “thin air” is employed, it sets in motion an exchange of nothing for something, amounting to a diversion of wealth from wealth generators to the holders of newly generated money.

Increases in money supply in the modern world implies increases in the money out of nothing, and the supplier of new money obtains it by exchanging nothing for it, no goods or services. Hence, we have here an exchange of nothing for money. Once the money out of “thin air” is exchanged for the products of wealth generators, it amounts to an exchange of nothing for something.

The holder of such money obtains final goods and services without contributing directly or indirectly to the pool of such goods and services or to the pool of wealth. This means that wealth is diverted from wealth producers to the holders of newly created money. Thus, the holders of new money consume goods and services without any contribution to the production of goods and services. In the process, genuine wealth generators are left with fewer goods and services at their disposal, which in turn weakens their ability to grow the economy.

Note that an exchange of nothing for something creates a diversion of wealth, and is going to take place regardless of whether the increase in money supply is expected or unexpected. This means that even if money expansion is expected, it still is going to undermine economic growth.

Then What Causes Stagflation?

Increases in money supply set in motion an exchange of nothing for something which, in turn, diverts wealth from wealth generators to non–wealth generators. This weakens the wealth generation process, which weakens economic growth.

Note that the price of a good is the amount of money paid for the good. When new money enters a market, it means that more money is paid for the good in this market, which increases the price of this good. Once the good is perceived as fully valued, the money leaves to other markets. Hence, money moves from one market to another market. Over time, an increase in money supply manifests itself through increases in prices of goods and services.

This creates a situation in which increases in money supply undermine the process of wealth generation, damaging economic growth. At the same time, we have more money per goods, which means that prices of goods are higher than before the increase in money supply took place. Thus, the increase in goods prices along with weaker economic growth, which we define as stagflation.

Stagflation is the end result of monetary pumping. Therefore, whenever the central bank adopts an easy monetary stance, it also sets in motion stagflation in the future. Now, for P-F and most economists, the criteria for accepting a theory is a supporting statistical correlation. It is because of the visible stagflation of 1970s that the P-F’s theory of stagflation gained wide support.

The fact that over time a strengthening in the monetary growth may not always manifest through a visible stagflation does not refute what we conclude regarding the consequences of increases in monetary pumping upon economic growth and prices.5 A theory that relies only on observed correlations is simply an exercise in curve fitting. What matters for the state of an economy is not the manifestation of stagflation, but rather increases in the money supply out of “thin air.”

The severity of stagflation depends upon the condition of the current pool of wealth. If the wealth pool is declining, then a visible decline in economic activity is likely to ensue. Moreover, because of past monetary pumping and the consequent increase in price inflation, we see visible stagflation. Conversely, if the pool of wealth is still growing, some economic activity is likely to follow. Given the rising momentum of prices, there will be positive correlation between economic activity and price inflation.

We conclude that if we do not observe the symptoms of stagflation after the central bank has pumped new money into the economy, this means that the pool of wealth is still growing. Conversely, if we stagflation, then most likely the pool of wealth is declining.

Conclusions

Increases in the money supply set in motion an exchange of nothing for something, transferring resources from wealth generators to non–wealth generators. Consequently, this weakens both the wealth generation process and the pace of economic activity. When new money enters goods markets, it means there is more money per goods, which increases their prices. Therefore, we have an increase in goods prices along with weakening of economic growth.

This is what stagflation is about. Monetary pumping over time always results in stagflation, although it often is not immediately visible. As the pool of wealth comes under pressure, however, the phenomenon of stagflation becomes all too real.

- 5. Guido Jorg Hulsmann, “Facts and Counterfacts in Economic Law,” Journal of Libertarian Studies 17, no. 1 (Winter):57-102.

You Might Also Like

To Fight Russia, Europe’s Regimes Risk Impoverishment and Recession for Europe

To Fight Russia, Europe’s Regimes Risk Impoverishment and Recession for Europe

2022-04-23

European politicians are eager to be seen as "doing something" to oppose the Russian regime following Moscow’s invasion of Ukraine. Most European regimes have wisely concluded—Polish and Baltic recklessness notwithstanding—that provoking a military conflict with nuclear-armed Russia is not a good idea.

Achtung Inflation: Wohlstand in Gefahr!

Achtung Inflation: Wohlstand in Gefahr!

2022-04-14

“So act that your principle of action might safely be made a law for the whole world.”

| Immanuel Kant (1724–1804)

Heavy Sanctions against Russia Could Usher in a Wider Economic War

Heavy Sanctions against Russia Could Usher in a Wider Economic War

2022-04-11

Vladimir Putin’s invasion of Ukraine was met with unprecedented economic sanctions by the United States and its allies in order to cripple Russia’s capacity to wage war. Never before in post–World War II history has an economy of Russia’s size been reprimanded with such force. Moreover, the sanctions could remain in place after the war ends and reach other major economies too, in particular China. In this case, current sanctions could be the harbinger of a longer-term economic war with dire consequences for global productivity and welfare.

Sweeping Sanctions Invite Countersanctions

The round of sanctions imposed on Russia following the annexation of Crimea in 2014 were limited to travel bans, freezing of the assets of certain Russian officials, and a prohibition of credit and technology

When Higher Prices Are Not Inflation

When Higher Prices Are Not Inflation

2022-01-19

Back to 2020, the federal government’s covid-mandated shutdown of meat production plants hobbled the nation’s meat production capabilities, leaving farmers with nowhere to send their beef. This resulted in them having to cull cattle and other livestock. The uncertainty caused farmers to scale back their production at the time, which Arun Sundaram told CNBC “can affect production more than a year, year and a half down the road.”

How Easy Money Inflated Corporate Profits

How Easy Money Inflated Corporate Profits

2022-01-13

In the incessant media discussion about whether inflation is transitory there is a big elephant in the room about which all are silent. Perhaps strangely some do not see it. Others for whatever reason pretend it is not there. The elephant is the fantastic surge in US corporate profits that monetary inflation has fueled during the second year of the pandemic.

New York State Has Imposed New Covid Rituals. This Time There’s Some Resistance.

New York State Has Imposed New Covid Rituals. This Time There’s Some Resistance.

2022-01-06

With new mask and vaccine mandates, New York’s Governor Kathy Hochul has reaffirmed the state’s status as the nation’s most zealous practitioner of covid cultism.

True Competition versus the Monopolist “Minimal State”

True Competition versus the Monopolist “Minimal State”

2021-12-31

According to Ayn Rand’s ethics, the only basis for value is an individual’s survival as a rational being. In order to live as a rational being, you must respect the rights of others as rational beings each aiming at his own survival.

Tags: Featured,newsletter