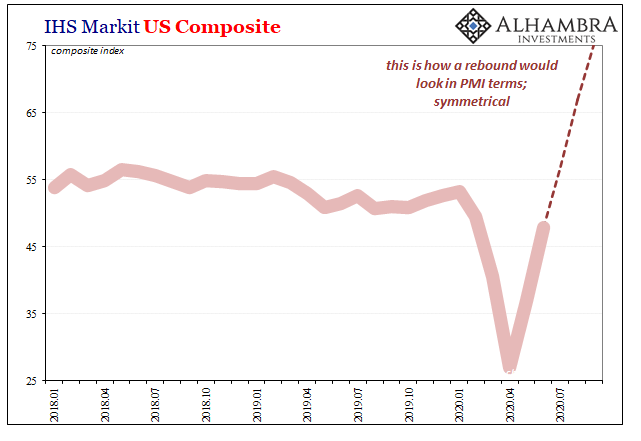

It’s just not fast enough. And with the labor market spitting out numbers across a broad economic cross-section that look increasingly tired suggesting an economy running out of momentum, there’s the added urgency of time. Late summer figures still aren’t close to where they need to be even though when you view them in isolation they can look tremendous. Start with PMI’s, a bunch of them from last week and early this week. Many are the highest in many months, years for quite a few. But matching up with early 2019 or late 2018, not even coming up as high as 2017, that’s actually trouble. And it would be that way even if following a normal downturn. After the one from Q2, it’s downright curious this absence of an unambiguously sharp upturn. IHS Markit US

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments

This could be interesting, too:

Joseph Y. Calhoun writes Weekly Market Pulse: Questions

Joseph Y. Calhoun writes Weekly Market Pulse: It’s An Uncertain World

Joseph Y. Calhoun writes Market Morsel: SLOOSing

Joseph Y. Calhoun writes Market Morsel: How “The Market” Is Really Doing

| It’s just not fast enough. And with the labor market spitting out numbers across a broad economic cross-section that look increasingly tired suggesting an economy running out of momentum, there’s the added urgency of time. Late summer figures still aren’t close to where they need to be even though when you view them in isolation they can look tremendous.

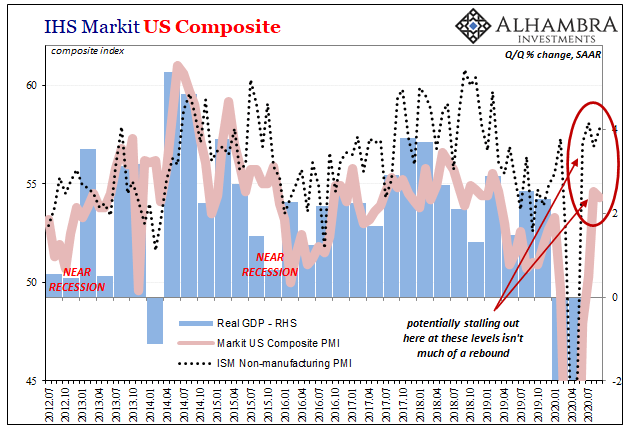

Start with PMI’s, a bunch of them from last week and early this week. Many are the highest in many months, years for quite a few. But matching up with early 2019 or late 2018, not even coming up as high as 2017, that’s actually trouble. And it would be that way even if following a normal downturn. After the one from Q2, it’s downright curious this absence of an unambiguously sharp upturn. |

IHS Markit US Composite, 2012-2020 - Click to enlarge |

| Take the best of the bunch relating to the US economy, the ISM’s Non-manufacturing index. The service sector was just slammed shut earlier this year, but now it’s been reopened for four months and more. Yet, the ISM’s estimate for it can only manage 57.8, or about the same territory as January and March 2019 – not exactly a couple of good months to be compared with.

The headlines scream how it’s best in a year and a half, but that’s totally misleading. Worse still, while the highest of the PMI’s this one was actually higher back in July; like a lot of other data, including pretty much all the most recent labor stats save the unemployment rate, they keep indicating something of a stall brewing since then. At around a level or rate that is way, way less than the economy needs. |

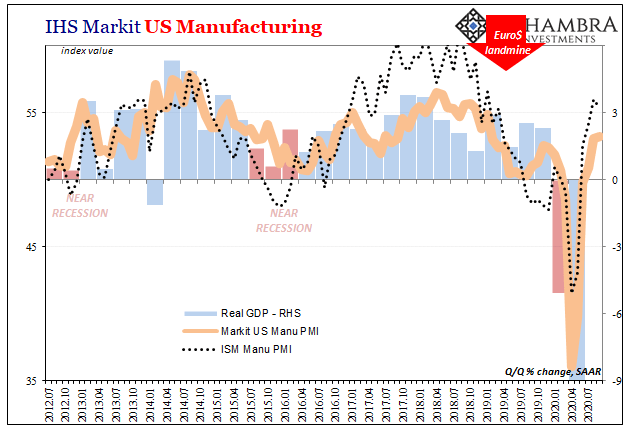

IHS Markit US Manufacturing, 2012-2020 - Click to enlarge |

| It only gets worse in manufacturing which should be flying upward after the massive crunch in between. Being stuck here unable to match even 2018 levels cries out serious deficiency.

Where are all the middle to high 60s for these things? 70s? Soft data, hard data; doesn’t matter. Turning to the latter, outside of BLS estimates and unemployment claims, let’s take a look at something like global trade. US exports continue to be seriously undermined by an entire global economy that’s obviously nowhere near V-like. Unadjusted, exports in August 2020 were still down 15% year-over-year. |

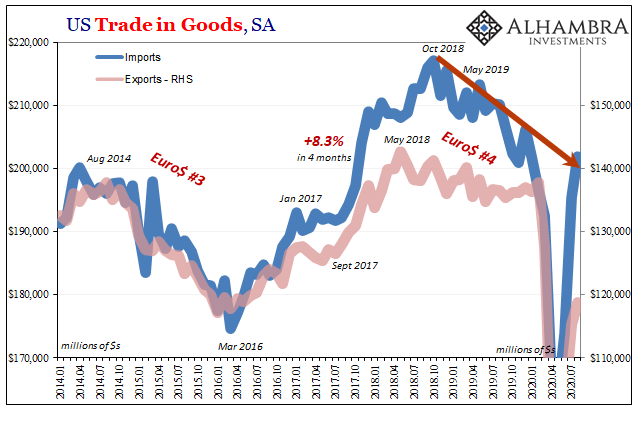

US Trade in Goods, SA 2014-2020 - Click to enlarge |

| That’s utterly atrocious; it does begin to explain some of the low 50s for manufacturing PMI’s.

Import activity has been somewhat better, thanks to the federal government’s ultra-loose cash payments. Even so, this isn’t anything like a “V”, either. Unadjusted, the total value of goods imported was down just about 6% year-over-year in August, which continues to be more mild recession than converting toward recovery (and the seasonally adjusted estimate was higher, shown below, out of line with the unadjusted but even still seriously depressed). |

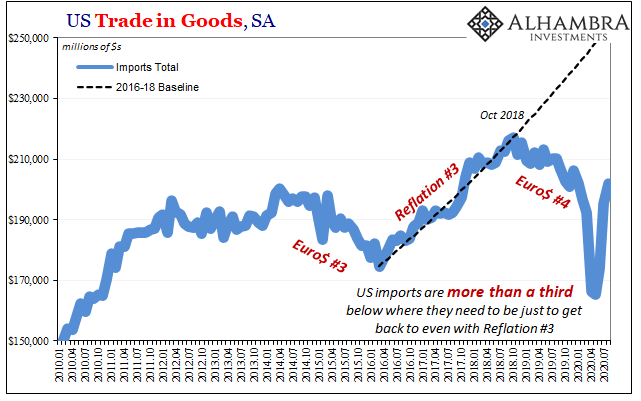

US Trade in Goods, SA 2010-2020 - Click to enlarge |

| The lack of rebound becomes even more apparent when you take into account how US demand for foreign goods (like global demand for US goods) has been stuck in a downturn for just about two years now. How can it be possible that in August 2020, imports are outrageously less than they were twenty-three months ago – and nowhere near where they should’ve been had globally synchronized growth not turned by Euro$ #4 into this globally synchronized downturn.

Like the PMI’s, these are not robust figures – though they can sound like they are and appear to be optimistic even gigantic at times if we ignore how they got that way. |

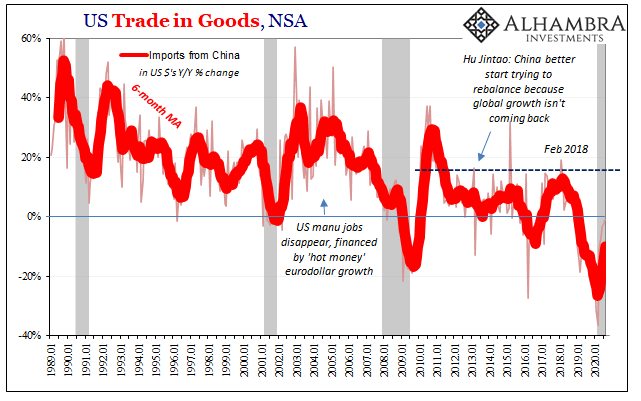

US Trade in Goods, NSA 1989-2020 - Click to enlarge |

| For instance, US imports from China were nearly flat year-over-year (unadjusted) in August. That’s the best result, the smallest contraction since December 2018. All good, right?

But being slightly less than August 2019 which had been a massive 14% less than August 2018, somehow the US is buying 15% fewer goods from China this summer than it did two summers ago even though the Chinese economy had reopened back in March after an enormous collapse, and the US economy supposedly roaring its way toward full recovery since then. These figures just don’t square with that. And China’s the best case where US imports/demand are concerned. |

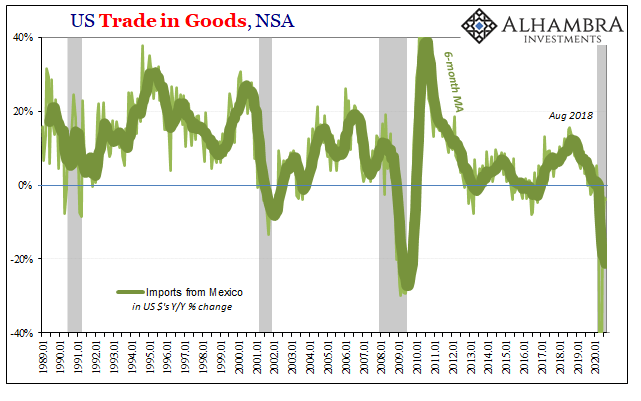

US Trade in Goods, NSA 1989-2020 - Click to enlarge |

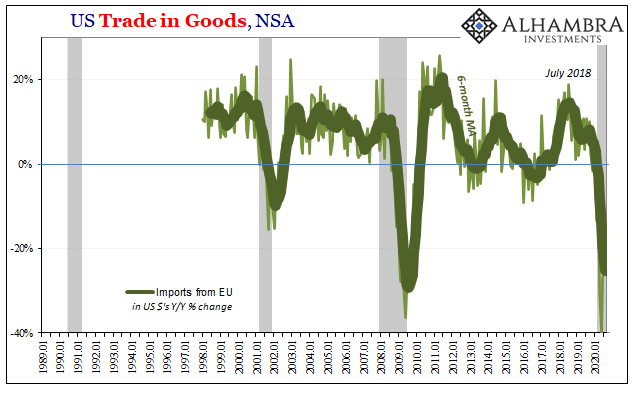

| Those coming from Mexico are still dropping this late into the summer, while inbound trade from Europe was down more than 20% year-over-year in August. No wonder Christine Lagarde is pleading for more coordinated Continental action as well as hinting at playing around with NIRP again (as if that would do anything).

Officials’ lack of ideas is an outgrowth of what really is a lack of return to growth. |

US Trade in Goods, NSA 1989-2020 - Click to enlarge |

| Things are getting better, that much is clear and that’s not really the problem. We’ve already suffered the recession, and the world remains stuck inside of it. The original “V” scenario has already been tossed by the wayside; the idea that since this had been a non-economic shutdown, turning everything off at the flip of a (government) switch it would be just as easy to turn everything right back on.

Well, that didn’t happen. But even now as the “V” has been bent downward more on its right, what does that actually mean? For one, turning everything back on hasn’t been so easy; there are, obviously, things standing in the way. |

US Dollar / Brazilian Real - Click to enlarge |

| COVID, yes, but also changed behavior as well as the same stupid global dollar shortage hardly anyone accounts for given Jay Powell’s outrageous public behavior (as an outright liar). Why is global trade, especially US exports, the ultimate laggard here? That’s one key reason, the biggest. |

US Dollar / Japan Yen, 2018-2020 - Click to enlarge |

|

|

| But the effects of global monetary problems are not strictly for the rest of the world to sort out. As we’ve seen and documented countless times, the US economy suffers these ill-effects, too, if not always quite to the same degree nor under the same timing as everyone else.

Positive numbers, or those above 50 in the case of PMI’s, they are certainly better than alternative of negatives or sub-50. But are they enough positive and better? As of late summer, August and September, they wouldn’t even be enough if Euro$ #4 had produced a “normal” downturn and recession – let alone something like March. |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

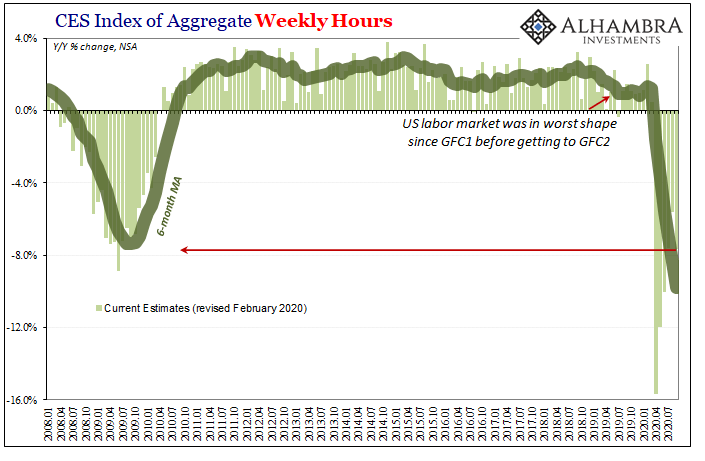

| That’s why the economy remains in a ten-figure jobs deficit after this many months with a growing list of evidence suggesting whatever momentum there had been from reopening alone it just wasn’t ever going to be enough to overcome all these other (and unnecessary) negative factors. |

CES Index of Aggregate Weekly Hours, 2008-2020 - Click to enlarge |

Inflation Expectations, 2003-2019 - Click to enlarge |

You Might Also Like

From QE to Eternity: The Backdoor Yield Caps

From QE to Eternity: The Backdoor Yield Caps

So, you’re convinced that low rates are powerful stimulus. You believe, like any good standing Economist, that reduced interest costs can only lead to more credit across-the-board. That with more credit will emerge more economic activity and, better, activity of the inflationary variety. A recovery, in other words. Ceteris paribus. What happens, however, if you also believe you’ve been responsible for bringing rates down all across the curve…and then no recovery.

What Did Everyone Think Was Going To Happen?

What Did Everyone Think Was Going To Happen?

Honestly, what did everyone think was going to happen? I know, I’ve seen the analyst estimates. They were talking like another six or seven perhaps eight million job losses on top of the twenty-plus already gone. Instead, the payroll report (Establishment Survey) blew everything away, coming in both at two and a half million but also sporting a plus sign.The Household Survey was even better, +3.8mm during May 2020. But, again, why wasn’t this expected?

Monthly Macro Monitor – June 2020

Monthly Macro Monitor – June 2020

The stock market has recovered most of its losses from the March COVID-19 induced sell-off and the enthusiasm with which stocks are being bought – and sold but mostly bought – could lead one to believe that the crisis is over, that the economy has completely or nearly completely recovered. Unfortunately, other markets do not support that notion nor does the available economic data.

Gratuitously Impatient (For a) Rebound

Gratuitously Impatient (For a) Rebound

Jay Powell’s 2018 case for his economic “boom”, the one which was presumably behind his hawkish aggression, rested largely upon the unemployment rate alone. A curiously thin roster for a period of purported economic acceleration, one of the few sets joining that particular headline statistic in its optimism resides in the lower tiers of all statistics.

A Tactical Update: Whither Goest The Dollar

A Tactical Update: Whither Goest The Dollar

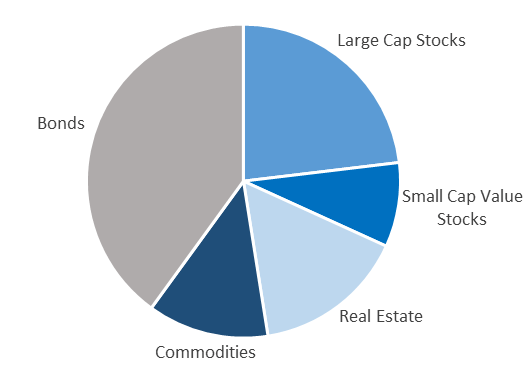

Our Fortress strategic asset allocation includes 5 distinct asset classes: The Fortress allocation has historically produced better risk-adjusted returns than the traditional 60% stocks/40% bonds allocation.

That’s Probably Why Only Half a “V”

That’s Probably Why Only Half a “V”

Why only half a “V?” If the latest PMI’s are anywhere close to accurate, and they don’t have to be all that close, then the production side of the economy may have stalled out somewhere nearer the trough of this contraction. The promise of May’s big payroll report surprise has dissipated in more than just the bond market.

China’s Hole Puzzle

China’s Hole Puzzle

One day short of one year ago, on September 16, 2019, China’s National Bureau of Statistics (NBS) reported its updated monthly estimates for the Big 3 accounts. Industrial Production (IP) is a closely-watched indicator as it is relatively decent proxy for the entire goods economy around the world. Retail Sales in the post-Euro$ #2 context give us a sense of the Chinese economy’s persistent struggle to try to “rebalance” without the pre-2008 boost China had obtained through actual global growth contributing to its export orientation. The third of the Big 3 is Fixed Asset Investment (FAI), the real secret behind the country’s rapid modernization. FAI is how the Chinese view their own future, whether that’s as a rebalanced consumer-led economy leaping off into a brand new paradigm; or one

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

It’s always something. There’s forever some mystery factor standing in the way. On the topic of inflation, for years it was one “transitory” issue after another. The media, on behalf of the central bankers it holds up as a technocratic ideal, would report these at face value. The more obvious explanation, the argument with all the evidence, just couldn’t be true otherwise it’d collapse the technocracy right down to the ground.And so it was also in the bond market. Inflation and their yields very much related, the lack of the former wasn’t ever used to explain the curious absence of the BOND ROUT!!! No, the US Treasury market has been beset by its own set of “transitory” factors, too. As ridiculous as some of the inflation excuses had been, Verizon’s unlimited wireless data plans the

Tags: