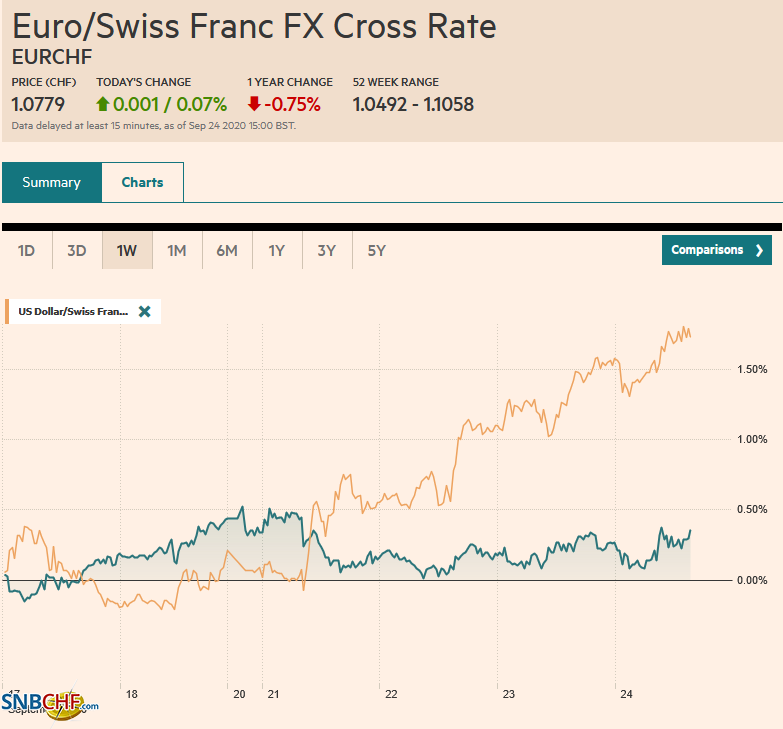

Swiss Franc The Euro has risen by 0.07% to 1.0779 EUR/CHF and USD/CHF, September 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The two recent market developments, push lower in stocks, and higher in the dollar is continuing. Tuesday’s gains in the S&P 500 and NASDAQ were unwound on Wednesday and this is helping drag global markets lower. The MSCI Asia Pacific Index fell for the fourth consecutive session today and many markets (India, Shenzhen, Taiwan, and Korea) fell more than 2% and most others were off more than 1%. Europe’s Dow Jones Stoxx 600 is giving back the past two days’ gains. The S&P 500 could gap lower at the open. Benchmark 10-year yields are a little softer but have remained subdued in

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Currency Movement, ECB, EUR/CHF, Featured, Japan, Mexico, newsletter, TLTRO, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.07% to 1.0779 |

EUR/CHF and USD/CHF, September 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The two recent market developments, push lower in stocks, and higher in the dollar is continuing. Tuesday’s gains in the S&P 500 and NASDAQ were unwound on Wednesday and this is helping drag global markets lower. The MSCI Asia Pacific Index fell for the fourth consecutive session today and many markets (India, Shenzhen, Taiwan, and Korea) fell more than 2% and most others were off more than 1%. Europe’s Dow Jones Stoxx 600 is giving back the past two days’ gains. The S&P 500 could gap lower at the open. Benchmark 10-year yields are a little softer but have remained subdued in the face of the dramatic moves inequities. The US yield is little changed near 0.66%. Practically no currency could escape the clutches of the rebounding dollar, though the yen and sterling are little changed. The JP Morgan Emerging Market Currency Index is lower for the fifth consecutive session. Gold remains heavy and is approaching the (38.2%) retracement of this year’s rally which is found near $1837. Crude oil is consolidating at lower levels. November WTI is in a narrow range below $40 a barrel. |

FX Performance, September 24 - Click to enlarge |

Asia Pacific

Hong Kong and New Zealand report trade figures. Economists did a good job forecasting New Zealand imports and exports. As expected, the formers rose a little and the latter slipped. The takeaway is that New Zealand reported its first trade deficit (~NZD353 mln), snapping a six-month period of trade surpluses. Economists had a harder time with HK figures. Exports pared their decline to 2.3% year-over-year from 3%, but the bigger miss was in the weakness of imports. These fell 5.7% year-over-year after a 3.4% decline in July. The net result was that HK’s trade surplus was halved from the HKD29.8 bln to HKD14.6 bln.

China continues to harass Taiwan with incursions into its air defense zone. The bullying practice has escalated in the past week or so. Beijing’s aggressiveness comes as the US some European countries have stepped up their interactions, including high-level visits. It is hard to say that it is having an economic impact but as a potential flashpoint, it is drawing attention.

Japan may have a new prime minister, but the government’s assessment of the economy remained little changed from last month. The economy is said to be in a severe place but some areas, namely, exports, production, business failures, and jobs, are improving (four of 14 categories). The median forecast in the Bloomberg survey expects the economy to expand 15% this quarter, the first expansion since Q3 19.

The dollar is in less than a third of a yen range today above JPY105.20. The $1.4 bln in expiring options between JPY105.10 and JPY105.25 have been neutralized. The next set is for almost the same amount at JPY105.70-JPY105.75. A four-day uptrend on the hourly bar charts comes in a little above JPY105.20 by the North American open. A break could see JPY104.60-JPY104.80. The Australian dollar is lower for the fifth consecutive session. It dipped below $0.7030 for the first in two months. A break of $0.7000 could see $0.6950 quickly. The $0.7080 area now offer resistance. The PBOC set the dollar’s reference rate a little softer than the bank models in the Bloomberg survey anticipated. Although some observers see it as a sign that officials are seeking to stop the yuan from strengthening, the fact of the matter is that the dollar remained bid. The greenback is at its best level since the start of last week, a little below CNY6.83. Note that after the US market close today, FTSE-Russell will announce whether it will include Chinese bonds in its indices. A year ago, it refused, but China has reduced barriers to enter and exit.

Europe

European banks took 174.5 bln euros from the ECB’s latest Targeted Long-Term Refinancing Operation. These are loans that can have a rate of as much as minus 100 bp providing the funds are lent to households and businesses. It was at the high end of expectations and follows a 1.3 trillion operation a few months ago. This will lead to another jump in the ECB’s balance sheet. Recall that the ECB’s balance sheet has been slowing increasing as it continues to buy bonds under its APP and PEPP operations. The extra liquidity in the Eurosystem is a factor that is pushing the three-month Euribor a little below the minus 50 bp deposit rates. When observers say that central banks are out of ammo, few anticipated the deeply negative loans offered and the introduction of the dual rates.

Neither the Swiss National Bank nor Norway’s Norges Bank altered policy at today’s meetings. The pullback in the Swiss franc in recent weeks is too small to register for officials, who remain concerned about its strength. The OECD regards it as the most over-valued currency in its universe. The threat of being identified by the US as a “currency manipulator” is not a strong enough deterrent as intervention remains one of its key tools. Some had expected the Norges Bank to bring forward its first hike from the end of 2022, but it did not. On the other hand, Hungary raised the one-week deposit rate 15 bp to 75 bp, catching the market by surprise and giving the forint a lift.

The German September IFO survey edged higher. The current assessment rose to 89.2 from 87.9, while the expectations component firmed to 97.7 from a revised 97.2 (from 97.5 initially). The overall assessment of the business climate rose to 93.4 from 92.6. The preliminary PMI data showed the manufacturing sector continues to rebound, while the service sector is stalled.

In the UK, Chancellor Sunak canceled the fall budget and is expected to present a new job support program to Parliament today. Speculation in the press is for a German-like arrangement, where the government picks up some of the wage bills for employees that are retained but on shorter hours. Meanwhile, the British Chamber of Commerce estimate suggests over half of UK firms have not completed the government’s recommended steps to prepare for the end of the standstill agreement with the EU.

The euro is extending its decline for a fifth consecutive session. It has dipped below $1.1635 in European turnover. For the first time this quarter, the skew in the one- and two-month options (risk-reversals) favor euro puts over calls. The $1.16 area corresponds to a (50%) retracement of the Q3 gains. The $1.1600-$1.1610 area holds about 1.6 bln euro in options that expire today. There is another option for nearly 525 mln euro at $1.1625 that also will be cut today. A move above $1.17, where an 845 mln option is struck (expiring today) would help stabilize the tone. Sterling is firm within yesterday’s range when it tested $1.2675. It is near $1.2750 in late London morning turnover. A push above $1.28 is needed to begin repairing some of the recent technical damage.

America

The US reports a new home sale (August) and the KC Fed manufacturing survey (September), but it will be the weekly jobless claims that capture the attention. Seasonal factors encourage expectations for a continued gradual decline. However, note that around November, the seasonal adjustment will add rather than subtract. The markets will be particularly sensitive to an unexpected increase in weekly jobless claims, especially given the lack of fresh measures by either the Fed or Congress. In fact, some observers attribute the Fed’s somber assessment to prompt more stimulus as a factor that helped spur the down move inequities.

Canadian Prime Minister Trudeau unveiled funding for a wide range of initiatives, including daycare, pharma, housing, and the environment. None of the three major opposition parties endorsed it. Trudeau leads a minority government and the budget needs to be approved or it could potentially trigger new elections.

Mexico’s central bank meets today. Yesterday’s retail sales report showed a solid 5.5% increase in July, but it was still less than expected. Inflation is running just north of the upper end of Banxico’s 2-4% target. The cash rate target is 4.5%. The peso’s six-week rally is ending with a bang this week and it is off over 5%. After five 50 bp rate cuts, Banxico is widely expected to cut 25 bp today. We suspect the odds of standing pat is greater.

The US dollar poked above CAD1.34 today for the first time since early August. The next important chart area is near CAD1.3440. Initial support is likely around CAD1.3360. If the equity market stabilizes the Canadian dollar will likely strengthen. After jumping over 3% yesterday, the greenback extended its gains to MXN22.53 in Asian turnover but has gradually firmed through the European morning. The first area of support is seen in the MXN22.00-MXN22.20 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, May 26: Fear is Still on Holiday

FX Daily, May 26: Fear is Still on Holiday

Overview: The heightened tensions between the US and China sapped risk-appetites before the weekend, but appear to be missing in action today. Equity markets have rebounded strongly. Nearly all the equity markets in the Asia Pacific region rose (India was a laggard) led by an almost 3% rally in Australia, which was seen as particularly vulnerable to the Sino-American fissure.

FX Daily, March 25: Relief, but…

FX Daily, March 25: Relief, but…

Overview: Global equities are marching higher. While the Dow Jones Industrials posted its biggest advance since 1933, the US is lagging behind other leading benchmarks. The MSCI Asia Pacific advanced, led by Japan’s Nikkei’s 8% gain. It was third consecutive gain, during which time the Nikkei has rallied 17%. Europe’s Dow Jones Stoxx 600 is up about 3.5% after bouncing 8.4% yesterday.

FX Daily, April 2: Optimism on Oil Deal Steadies Risk Appetites…for the Moment

FX Daily, April 2: Optimism on Oil Deal Steadies Risk Appetites…for the Moment

Overview: After US stocks dropped more than 4% yesterday, investor sentiment has improved, apparently sparked by ideas that the pain will force oil producers to find a way to reduce supply. Oil prices have surged, with the May WTI contract rallying around 7%. Asia Pacific equities were mostly higher, with Japan and Australia the notable exceptions.

FX Daily, May 27: China and Hong Kong Pressures are Having Limited Knock-on Effects

FX Daily, May 27: China and Hong Kong Pressures are Having Limited Knock-on Effects

Overview: The S&P 500 gapped higher yesterday, above the recent ceiling and above the 200-day moving average for the first time since early March. The momentum faltered, and it finished below the opening level and near session lows. The spill-over into today’s activity has been minor. The heightened tensions weighed on China and Hong Kong markets, but Japan, South Korea, Taiwan, and Indian equity markets rose.

FX Daily, May 29: Month-End Profit-Taking Weighs on Equities as the Euro Pops Above $1.11

FX Daily, May 29: Month-End Profit-Taking Weighs on Equities as the Euro Pops Above $1.11

Overview: The announcement that President Trump will hold a press conference on China later today rattled investors yesterday after they had earlier shrugged off the escalation of tension between the US and China to take the S&P 500 up to its highest level in nearly three months. The S&P 500 reversed and settled on its lows, and this carried over into today’s activity, which also may be reflecting month-end adjustments.

FX Daily, July 07: Fade the Dollar Gains

FX Daily, July 07: Fade the Dollar Gains

The S&P 500 rallied 1.6% yesterday to extend the streak to a fifth consecutive session, and the longest of the year and completed the negation of a bearish technical pattern. However, the main feature today is a wave of profit-taking on risk assets. Most equity markets moved lower in the Asia Pacific region. Chinese markets were a notable exception.

FX Daily, July 14: Turn Around Tuesday Began Yesterday

FX Daily, July 14: Turn Around Tuesday Began Yesterday

Overview: Turn around Tuesday began yesterday with a key reversal in the high-flying NASDAQ. It soared to new record highs before selling off and settling below the previous low. The S&P 500 saw new four-month highs and then sold-off and ended on its lows with a loss of nearly 1% on the session. Asia Pacific shares fell, led by declines in Hong Kong and India.

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

A consolidative tone has emerged after US equity benchmarks reached new highs yesterday. The MSCI Asia Pacific Index had reached seven-month highs on Tuesday, but Japan, China, and Australian stocks saw modest profit-taking today. European shares are recouping yesterday’s minor loss, and US shares are flat.

Tags: #USD,$CNY,Currency Movement,ECB,EUR/CHF,Featured,Japan,Mexico,newsletter,tltro,USD/CHF