We are approaching the mid-point of the first quarter, and the coronavirus from China is the new key development for businesses and investors. The economic impact appears to be still growing as the disruption to supply chains, production, and demand continues. The re-opening of China from the extended Lunar New Year holiday brought some relief to the markets as officials ensured ample liquidity, leaned against short selling, and offered concessions to businesses and encouraged forbearance by lenders. The markets have a penchant for overreacting to non-economic developments. The US-Iran conflict escalated, and Brent oil spiked to almost on January 8 and was back below a week later. China’s economic paralysis has reduced its consumption by an estimated

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Banxico, China, Featured, Federal Reserve, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

We are approaching the mid-point of the first quarter, and the coronavirus from China is the new key development for businesses and investors. The economic impact appears to be still growing as the disruption to supply chains, production, and demand continues. The re-opening of China from the extended Lunar New Year holiday brought some relief to the markets as officials ensured ample liquidity, leaned against short selling, and offered concessions to businesses and encouraged forbearance by lenders.

The markets have a penchant for overreacting to non-economic developments. The US-Iran conflict escalated, and Brent oil spiked to almost $75 on January 8 and was back below $64 a week later. China’s economic paralysis has reduced its consumption by an estimated million barrels a day, and this saw Brent oil drop below $54 a barrel last week. The US 10-year yield began the year a handful of basis points below the 2% threshold, which it has not traded above since the beginning of last August. It dropped to almost 1.70% on the US-Iran tension and fell to nearly 1.50% at the end of January. After a series of robust reports, including the 225k jump in January non-farm payrolls and new record highs in the stock market, the yield still finished the week below 1.60%.

In December, 14 of the 17 Federal Reserve officials indicated that they thought no change of rates was likely this in 2020. The December 2020 fed funds futures contract ended 2019 with an implied yield of 1.40%, 15 bp below the average effective rate. It fell to 1.25% on the Middle East hostilities and eased to 1.12% by the end of January before the Chinese markets re-opened. Last week, it finished near 1.25%. Meanwhile, the Fed’s decision to hike the interest on reserves (by five basis points) at the late January FOMC meeting has seen the effective average fed funds rate (which is what the futures contract settles at) creep up to 1.59%,

Meanwhile, high-frequency data suggests the US economy has begun Q1 on a firm note. Most of the data surprised to the upside. This is not necessarily inconsistent with expectations of Fed easing. Last year’s three moves were cast insurance policies due primarily to headwinds from international issues, including trade. Even if the direct impact of the coronavirus is concentrated in China, the disruption to supply chains and the loss of affiliate sales (indeed the local sales by majority-owned affiliates of US multinationals is the dominant way that foreign demand is met, easily outstripping exports) arguably poses as great a risk to the US economy as last year’s threats.

United States

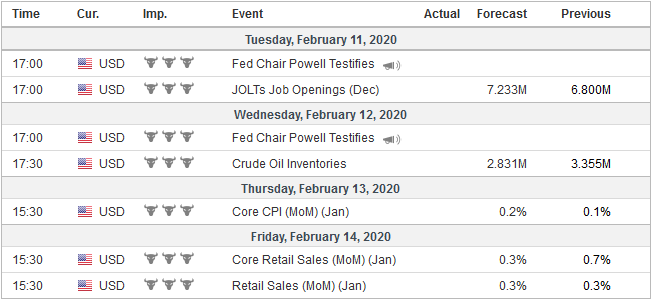

To date, the Fed officials that have spoken about the economic impact of the coronavirus, most seem to see limited direct impact. It does not appear to have been a sufficient shock (yet) to change their economic assessments, even if some multinational companies are affected. Fed Chair Powell can give the central bank’s policy as help keep the economic expansion moving forward despite the global challenges. The increase in the labor force participation rate (63.4%), the highest since 2013, suggests the Fed is right that there is more slack in the labor force. The data due out next week are unlikely to move the needle either. Headline and core CPI are running a little north of 2%, but the Fed targets headline PCE deflator and talks about the core deflator. Both of which have converged at 1.6% at the end of 2019. The Fed’s downgraded its assessment of consumption, for which the retail sales report covers a little more than 40%. Retail sales rose by 0.3% each month in Q4 19 and are expected to have increased by the same amount in January. As in other countries, the US industrial sector is facing headwinds. Consider that industrial output fell in four of the last six months of 2019. Indeed, last year it fell by almost 0.1% a month after rising at an average pace of 0.3% in 2018. The new year is off to a soggy start. The median forecast in the Bloomberg survey anticipates a 0.3% decline that would match the December report. Manufacturing output also fell by an average of 0.1% last year but has fared a bit better recently, increasing by 1.0% and 0.2% last November and December. It is projected to be flat, but the risks seem to be on the downside. Manufacturing lost 12k jobs in January, marking the third decline in four months. While the dramatic equity recovery is capturing the headlines and imaginations, the greenback as begun the year with a bang. Through the first full week in February, it has gained more than 2% against all the major currencies save the Swiss franc and yen. Both of them have fallen by more than 1%. In cold realpolitik Machievelian terms, the US’s chief geopolitical rival has experienced a negative shock that will weaken its economy, undermine is soft power, and setback its projection of power on the world stage. Business thinking about relocating production due to the “forever tariff war” with the US may be pushed further along this path by the coronavirus, and deep-seated suspicions, as this was the not first, it probably will not be the last coronavirus to emerge from China. |

Economic Events: United States, Week February 10 - Click to enlarge |

EurozoneEurope and Japan need stronger global growth conditions than the US. Europe is more reliant on exports than the US (or Japan, for that matter). At the low end are countries like Italy and France that export a bit more than 30% of GDP. Germany exports almost 50% of everything it produces. The Netherlands exported 85% and Belgium nearly 83% of GDP, according to the World Bank, in 2018. And then there is Luxembourg, which exported over 200% of GDP, and Ireland, who exported 122% of GDP. Of course, this probably overstates the case due to tax arbitrage games. Still, German factory orders were a big miss last week. The median forecast in the Bloomberg survey called for a 0.6% increase in December, and instead, they dropped by 2.1%. It was the weakest report in 10 months. It was notable, however, that domestic orders rose by 1.4% on top of the 1.3% increase in November. It was the third increase in the last four months of 2019. The weakness came from foreign orders. Here is the good news/bad news story. The good news is non-EMU orders increased by 2.1%. It followed two months in which their orders had fallen by a combined 5.5%. The bad news is that other countries in the eurozone were the culprit. They plummeted 13.9%, after a 2.4% decline in November. Adding insult to injury, the decline in orders was concentrated in capital equipment, which speaks to business investment and increasing growth potential. The simply dreadful December industrial production figures from Germany, France, and Spain warn of downside risks when the aggregate data are published next week. In fact, the data as to rekindle fears of a new contraction in Q1. On a month-over-month basis, economists expected German and French industrial output to fall by 0.2% and 0.3%. Instead, declines of 3.5% and 2.8% were reported, respectively. Economists expected Spain’s industrial production to have shrunk by 0.9% and instead contracted by 1.4%. Spain and France also reported downward revisions to their November reports. The outbreak of the coronavirus means that Q4 data is too historical to matter to most central banks, and even January data may not satisfactorily reveal the extent of disruption. This is especially true of China itself, whose data has not yet won investors’ confidence in the first place. The data is often distorted in January and February due to the Lunar New Year holiday in any event. |

Economic Events: Eurozone, Week February 10 - Click to enlarge |

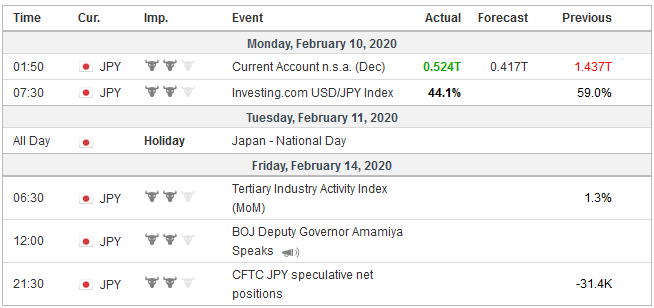

JapanMaybe Japan is an exception to this generalization. First, the official estimate of Q4 GDP is not due out until February 17 in Tokyo, but between the tax increase and typhoons, there is no doubt the economy contracted steeply in Q4. The median forecast in the Bloomberg survey stands at -1.0% quarter-over-quarter. Second, Japan exports account for less than a fifth of GDP, but for a country whose population is shrinking and household spending even before the tax hike was lukewarm at best, the knock-on effect could be severe. It is not only Japan’s goods exports to China, but foreign tourism is counted as the export of services in the national accounts. This means that it does not have to be a particularly strong shock to push Japan into a contraction in Q1 20, which be the second contracting quarter, meeting the rule-of-thumb definition of a recession. Arguably, the most critical data point from Japan in the week ahead is the preliminary estimate of January machine tool orders. They rose 10% in December, which included a 5% increase in foreign orders. Yet orders from China had fallen in November and December (by 2.8% and 7.6%, respectively). Orders from the US rose by 16.1%, but orders from South America surged by 44%, led by Brazil. |

Economic Events: Japan, Week February 10 - Click to enlarge |

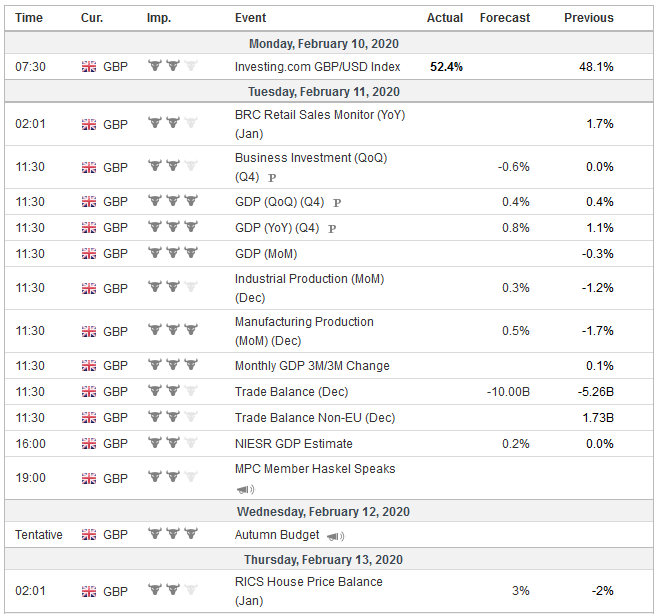

United KingdomThe UK’s data from the end of last year, including the first look at Q4 GDP (expected to have contracted slightly after a 0.4% expansion in Q3), is dated, not so much because of the pathogen, but because of the election that ended immediate uncertainty. This has led to a jump in business sentiment indicators. In contrast to the soft US and European industrial sectors, the UK’s industrial production likely expanded in December. Still, it must be understood within the context of the 1.2% decline in November. The stronger UK data, however, has not translated into strength for sterling. It was the weakest of the major currencies last week, losing about 2% against the dollar and 0.8% against the euro. The opposing positions between the UK and EU and the immediate resort to ultimatums brought to the fore a point we have underscored: There is a material risk that the standstill period ends without the UK and EU reaching an agreement, leaving the “Australian alternative” which is little more than the WTO agreement. |

Economic Events: United Kingdom, Week February 10 - Click to enlarge |

The Reserve Bank of New Zealand and Sweden’s Riksbank meet next week. Neither will change policy. The RBNZ meets on February 11, and it cut the cash rate by 75 bp last year. Growth and inflation expectations have picked up. The New Zealand dollar has fallen by roughly 4.8% so far here in Q1, and it can afford to monitor developments. The Riksbank meets the following day. It brought its reference rate back up to zero at the end of last year, becoming the first central bank to exit a negative rate regime, or at least partly. The deposit rate remains at minus 10 bp. The economy finished Q4 softly but appears to have bounced back in January with the PMI readings rebounding above the 50 boom/bust level.

Mexico’s central bank, Banxico, meets on February 13. It began an easing cycle last summer and has cut its overnight target four times to 7.25%. Inflation (CPI) rose 3.24% year-over-year in January, Mexico, reported before the weekend. The high nominal interest rate attracts carry trades where the euro, yen, Swiss franc, or dollar is sold to buy the peso or Mexican T-bills (cetes). The high real rate (nominal adjusted for inflation), a weak economy, and strong peso (due to these financial transactions) give the central bank plenty of room to continue to cut rates. This, in turn, attracts investors into Mexico’s bond market. The high real rates are also choking the economy. A case can be made for a larger move, but the central bank may be reluctant because of the cool reception of businesses to the Mexican government policies.

Tags: #USD,Banxico,China,Featured,federal-reserve,newsletter