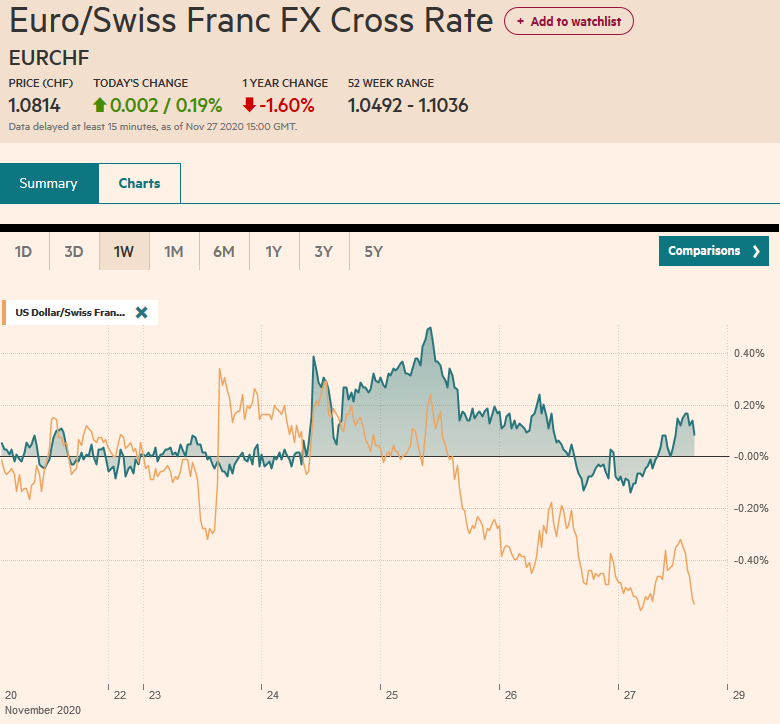

Swiss Franc The Euro has risen by 0.19% to 1.0814 EUR/CHF and USD/CHF, November 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Equities are finishing the week on a firm tone, while the US dollar remains heavy. In the Asia Pacific, only Australia and India did not end the week on a firm note. The MSCI Asia Pacific completed its fourth consecutive weekly gain, for around a 13% gain. Europe’s Dow Jones Stoxx 600 is edging higher today, and it too is completing its fourth weekly advance for a cumulative gain of around 14%. US stocks are trading firmer as well. So far this month, both the S&P 500 and NASDAQ are up about 11%, while the Russell 2000 is up nearly 20%. Bond yields are a little changed, and the US

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Australia, Brexit, China, Currency Movement, Featured, Indonesia, Japan, newsletter, Sweden, Turkey, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.19% to 1.0814 |

EUR/CHF and USD/CHF, November 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Equities are finishing the week on a firm tone, while the US dollar remains heavy. In the Asia Pacific, only Australia and India did not end the week on a firm note. The MSCI Asia Pacific completed its fourth consecutive weekly gain, for around a 13% gain. Europe’s Dow Jones Stoxx 600 is edging higher today, and it too is completing its fourth weekly advance for a cumulative gain of around 14%. US stocks are trading firmer as well. So far this month, both the S&P 500 and NASDAQ are up about 11%, while the Russell 2000 is up nearly 20%. Bond yields are a little changed, and the US 10-year yield is a couple basis points lows near 0.86%. Peripheral European bonds are making record lows, and Portugal’s 10-year yield is hovering just above zero. The dollar is softer against nearly all the majors today, and for the week, only the yen has been unable to rise against the offered greenback. Emerging market currencies are more mixed, with the Russian, Indian, and Chinese currencies softer. An increase in Turkey’s required reserve ratios for both lira and fx deposits and checking accounts appears to be offering the lira some support today. JP Morgan’s Emerging Market Currency Index is closing out its fourth consecutive weekly advance. Gold is bouncing along its trough, holding above $1800 but unable to move above $1820. WTI is trimming this week’s gains amid concerns that the recovery in prices (January WTI + 25% this month) will weaken OPEC+ resolve to postpone the planned increase in output at the start of next year. |

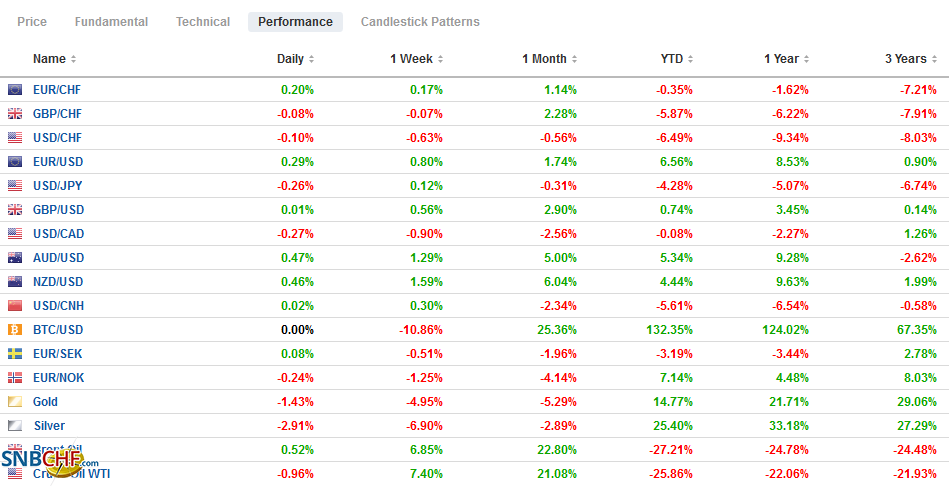

FX Performance, November 27 - Click to enlarge |

Asia Pacific

The MOF report showed Japanese investors sold JPY1.43 trillion (~$13.7 bln) of foreign stocks last week, the most in four months. For their part, foreign investors sold almost JPY1.2 trillion (~$11.5 bln) in Japanese equities. It is the most in a couple of months. Foreign investors could not keep pace in the fixed income space. Japanese investors bought JPY1.96 trillion (~$18.9 bln) of foreign bonds, while foreign investors about JPY461 bln Japanese bonds. It is the fourth consecutive week that Japanese investors were buyers of foreign bonds, and over the run, they bought roughly JPY4.42 trillion, the most in a four-week period since March.

After being under consideration for several weeks, China formally announced that Australian wine imports will be slapped with more than 100% anti-dumping levy starting tomorrow. This is the latest incident of Beijing punishing Canberra through trade, one of its few levers of power to express its disapproval over Australia’s political positions that have been critical of China and supportive of US efforts to check the rising power. Reports suggest that there are more than 50 ships carrying coal that are stranded off Chinese ports. Meanwhile, China reached a new agreement with Indonesia. Indonesia will supply China with $1.5 bln of coal over the next three years. Indonesia is the world’s largest exporter of thermal coal and is the main commercial rival of Australia’s coal.

For the first time in four sessions, the dollar traded below JPY104.00. The high for the week was set on Tuesday near JPY104.75 as it recovered from Monday’s low, near JPY103.70, which has been the week’s low as well. The greenback has not traded above JPY104.10 in the European morning today. The Australian dollar is firm and edging closer to $0.7400. The high for the year was set on September 1, near $0.7415. A small shelf has been carved near $0.7350, which serves as support. The PBOC set the dollar’s reference rate at CNY6.5755, in line with expectations. The yuan has moved broadly sideways this week. After falling for the past three weeks, the dollar is about 0.25% higher on the week. News of a surge in China’s industrial profits (28.2% year-over-year in October after 10.1% in September) seemed to have little impact. The PBOC injected a net of CNY40 bln into the banking system today to bring the week’s add to around CNY130 bln. The overnight repo fell by 44 bp to 0.82%, the lowest in a couple of months.

| Europe

Yesterday, Sweden surprised investors when the Riksbank announced a SEK200 bln (~$23 bln) increase in its bond-buying operation. It will step up its purchase pace in the New Year. The krona softened against the dollar and euro, both of whom had been trading near two-year lows before the unexpected announcement. The krona is consolidating softer against both the euro and dollar today. While the FOMC minutes boosted expectations of enhanced forward guidance on its balance sheets, and some expect a shift in purchase to the long-end, the recent ECB meeting record underscores the pessimistic tone and concern about the disinflationary pressures. The central bank’s chief economy also worried about the risk of tightening lending conditions to small and medium-sized firms. The regional economy is doing worse than expected, and the social restrictions are carrying into the next months. With the market expecting an expansion and extension of the ECB’s bond-buying and another lucrative TLRO, the ECB may struggle to surprise the market. A cut in the deposit rate from minus 50 bp would be one way, but even a small reduction may not be sufficient as the excess liquidity in the system has already pushed some short-term rates further below the deposit rate. The EU’s chief Brexit negotiator Barnier meets with EU fisheries ministers today ahead of his return to London next week to resume face-to-face talks after the Covid-driven virtual discussions seemed to make little headway. There has been a change in tone in recent days by EU officials expressing less optimism about a deal being struck. Meanwhile, the civil servant wage freeze and GBP4 bln cut in foreign aid announced by the Sunak, the UK Chancellor of the Exchequer, has been broadly criticized and sparking a new rift within the Tory Party. |

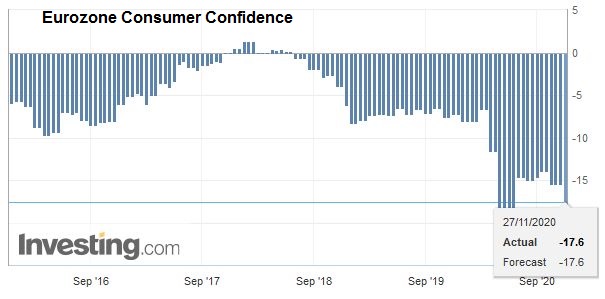

Eurozone Consumer Confidence, November 2020(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

Today may be the second time this year that the euro spends the entire session above $1.19. September 1, when the euro pushed above $1.20 for the first time in two years, was the other time. Still, so far today, the euro has been confined to the upper end of yesterday’s range ($1.1885-$1.1940). Although we retain a positive outlook for the euro next year, given the growth differentials here in Q4 illustrated by the PMIs and the recent upgrades of US Q4 GDP forecasts, we are cautious about extending euro exposure at these levels. Sterling has been knocking on $1.34 all week, and it has not given way, and an option for almost GBP390 mln today struck there that expires today. Initial support is seen in the $1.3300-$1.3325 area. Meanwhile, the euro has is edging higher against sterling for the fourth consecutive session. Around GBP0.8940, the euro has gained about 0.2% this week.

America

The recent string of US data is encouraging economists to revise up forecasts for Q4 GDP. Based on this week’s data, the Atlanta Fed’s GDP tracker jumped from 5.6% to 11%. St. Louis and NY Fed’s models will be released shortly and are likely to be upgraded. Private-sector economists are doing the same. If most forecasts previously were 3-4%, now it may be 4-6%. This offers a contrast to Europe and Japan, where growth is stagnating, or worse and deflationary pressures are evident EMU’s November CPI is out next week. The headline year-over-year rate will likely remain below zero. In October, Japan’s CPI was also negative, and earlier today, the November reading for Tokyo was dreadful at -0.7% for the headline and core rate (which excludes fresh food prices) from -0.3% and -0.5%, respectively. The October US CPI stood at 1.2% and 1.6% for the headline and core, respectively.

Neither the US nor Canada releases economic data today. Mexico reports its October trade surplus. The compression of its domestic demand and the integration in the US manufacturing has been a boon for Mexico’s trade surplus. Through the first nine months, Mexico has reported an average monthly surplus of $2.1 bln. In the same period last year, the average trade surplus was about $244 mln. The best days, though, are behind as the Mexican economy is recovering, led by manufacturing. The monthly surplus likely peaked in August at around $6.1 bln and narrowed in September to about $4.38 bln. The October surplus is expected to be near $3.35 bln.

Like the past three sessions, the US dollar is straddling the CAD1.30 level, where a $600 mln option will expire today. It is holding just above the week’s low near CAD1.2985. The year’s low was set on November 9 near CAD1.2930. The greenback has not traded above CAD1.3030 since Tuesday, which continues to offer the nearby cap. Similarly, the US dollar has been straddling the MXN20 level this week. While lower highs have been recorded each session this week, and while the low for the week was recorded yesterday just below MXN19.94, there is not much momentum. That said, the next important technical target is near MXN19.65.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

A flurry of deals, including the still-evolving Oracle-TikTok tie-up, helped lift equity markets in the Asia Pacific region. South Korea’s Kospi, and Indonesia, which had been battered last week, led the advance. The MSCI Asia Pacific Index rose for the third consecutive sessions. European bourses are little changed while US stocks are firmer.

FX Daily, October 15: Markets Shake and Dollar Goes Bid

FX Daily, October 15: Markets Shake and Dollar Goes Bid

A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off.

FX Daily, November 12: Nervous Calm in the Capital Markets

FX Daily, November 12: Nervous Calm in the Capital Markets

There is a nervous calm in the capital markets today. The equity rally in the Asia Pacific region stalled to end an eight-day rally, though the Nikkei’s rally remains intact.

FX Daily, November 16: Risk-On Despite Surging Pandemic

FX Daily, November 16: Risk-On Despite Surging Pandemic

Despite the surging pandemic and new restriction measure, risk-appetites appear strong to start the week. Led by 2% gains in the Nikkei and Taiwan’s Taiex, all of the Asia Pacific region’s equity markets advanced. European markets have followed suit and the Dow Jones Stoxx 600 is knocking on last week’s eight-month high.

FX Daily, November 19: Surging Virus Saps Risk Appetites

FX Daily, November 19: Surging Virus Saps Risk Appetites

Overview: News that the New York City was closing the schools to contain the virus sent stocks reeling in late North American dealings yesterday and spurred some profit-taking in the Asia Pacific and Europe. Equities in the Asia Pacific region were mostly lower, though China, South Korea, and Australia’s advanced and Tokyo markets were mixed.

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

Overview: News that the stimulus talks between the House Democrats and Senate Republicans was the excuse traders were looking for to extend the US equity gains yesterday, but shortly after the close, confirmation that Treasury was not going to agree to extend several Fed facilities sent stocks reeling.

FX Daily, November 24: Diverging PMIs Fail to Give the Dollar Lasting Support

FX Daily, November 24: Diverging PMIs Fail to Give the Dollar Lasting Support

Overview: The contrast between the eurozone and US preliminary PMI readings caught the short-term market leaning the wrong way, and the dollar snapped back after extending its recent losses. However, today the US dollar is back on its heels and returning to yesterday’s lows against most major currencies.

Tags: #USD,Australia,Brexit,China,Currency Movement,Featured,Indonesia,Japan,newsletter,Sweden,Turkey