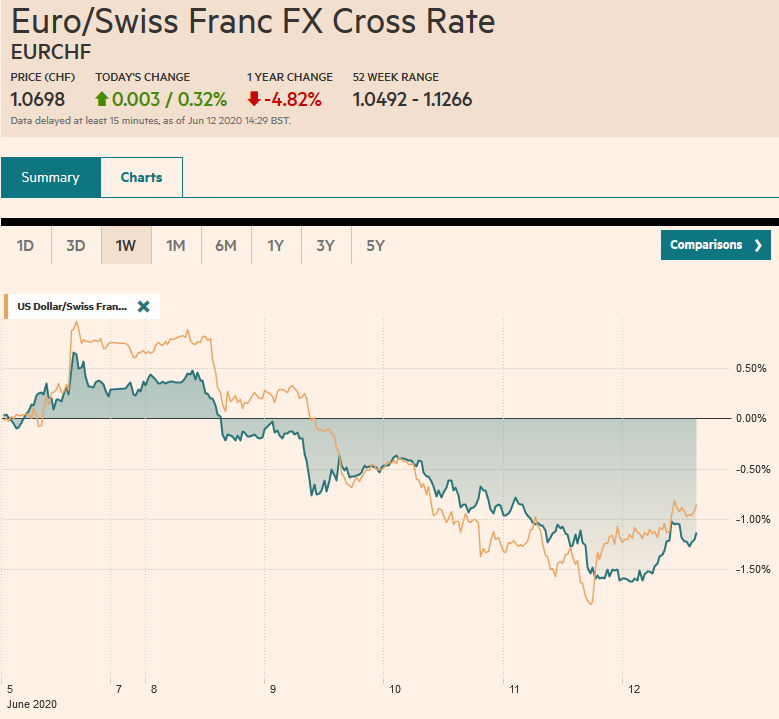

Swiss Franc The Euro has risen by 0.32% to 1.0698 EUR/CHF and USD/CHF, June 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The nearly three-month rally in risk assets ended with high drama with a stomach-churning almost 6% slide in the S&P 500 yesterday. Follow-through selling was seen in the Asia Pacific region, but most markets recovered from their lows, and although losses were still recorded, the downside momentum seemed broken. The same holds true for Europe. Bourses opened lower but by mid-morning had moved higher (~1.4%) and US shares are trading firmer (~2%). The MSCI Asia Pacific Index snapped a two-week advance that saw it rise 9.5% and is off around 3% this week. The Dow Jones Stoxx 600 rose

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of England, Bank of Japan, Currency Movement, EUR/CHF, Eurozone Industrial Production, Featured, FX Daily, newsletter, U.K. Gross Domestic Product, U.K. Manufacturing Production, U.K. trade balance, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.32% to 1.0698 |

EUR/CHF and USD/CHF, June 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

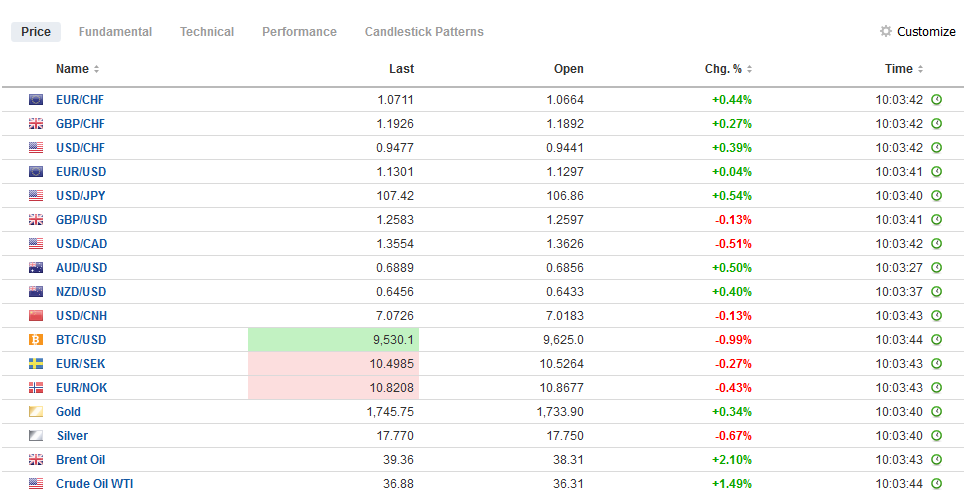

FX RatesOverview: The nearly three-month rally in risk assets ended with high drama with a stomach-churning almost 6% slide in the S&P 500 yesterday. Follow-through selling was seen in the Asia Pacific region, but most markets recovered from their lows, and although losses were still recorded, the downside momentum seemed broken. The same holds true for Europe. Bourses opened lower but by mid-morning had moved higher (~1.4%) and US shares are trading firmer (~2%). The MSCI Asia Pacific Index snapped a two-week advance that saw it rise 9.5% and is off around 3% this week. The Dow Jones Stoxx 600 rose around 13.75% over the past two weeks, and even with today’s gains that snap a four-day slide, it is off about 5.3% this week. The S&P 500 is nursing a 6% weekly loss coming into today’s session. It rose a little more than 11% over the past three weeks. Bond markets are subdued today. Yields are mostly narrowly mixed. The US 10-year benchmark yield is hovering around 70 bp, an almost 17 bp decline on the week. The benchmark German Bund yield is off 10 bp, and peripheral spreads widened this week. The dollar’s safe-haven gains yesterday are being pared today. The yen and Swiss franc are also slipping after yesterday’s gains. Many emerging market currencies in Asia did not recover today, but the Mexican peso and South African rand are leading the broader move higher. The JP Morgan Emerging Market Currency Index is up about 0.4% today to retrace about a third of yesterday’s drop. Gold is firm (~$1735) in the upper end of its range. July crude initially extended its slide since poking above $40 on Monday. It fell to about $34.50 earlier today before recovering to trade a little above $36 in the European morning. |

FX Performance, June 12 - Click to enlarge |

Asia Pacific

Japan revised its April industrial production loss to a 9.8% slide on the month, compared with the initial estimate of a 9.1% decline. There was little market reaction. The BOJ meets next week, and it is not expected to take fresh initiatives. That said, BOJ Governor Kuroda has hinted that the corporate sector may need more support. The BOJ has tripled the amount of corporate bonds and commercial paper it purchases. There is some talk that the BOJ could make loans with negative interest rates as the ECB does (and will do so in a big way next week).

The dollar held yesterday’s low just below JPY106.60 today and is recovering. There is an option for about $445 mln at JPY107.35 that expires today. A close above JPY107.85 area would be constructive. Follow-through selling pushed the Australian dollar to $0.6800, from where it bounced back above $0.6900 in early European turnover, but appears to be stalling. The $0.6930 area corresponds to the middle of this week’s range. It rose about 4.5% last week and near $0.6900 it is giving back about 1% this week. The PBOC set the dollar’s reference rate at CNY7.0865, seemingly to try to temper its surge. The bank models suggest a fix above CNY7.09. Net-net both the onshore and offshore yuan were little changed on the week (less than 0.1%). Meanwhile, the Hong Kong Monetary Authority appears to be continuing its defense of the band. Separately, the central bank of Indonesia announced it would intervene in the spot, NDF, and local bond market. The rupiah has risen more than 16% here in Q2 and appears to have turned this week. Intervention in the direction of the market is often more effective than fighting it.

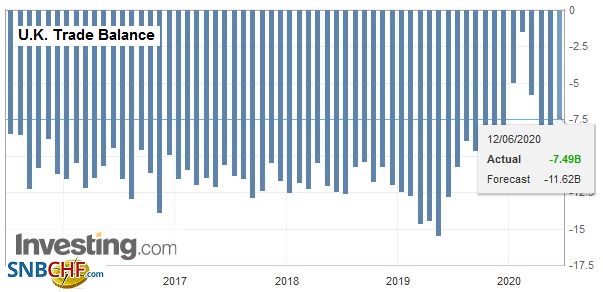

EuropeThe UK’s output dropped 20.4% in April after a 5.8% contraction in March. It was a bit worse than economists expected. Services contracted by 19%, manufacturing by more than 24%, and construction by 40%. Economic output was at 2002 levels. The only bright spot, some may find, is that the trade deficit narrowed. The Bank of England meets next week and is widely expected to increase its bond purchases. |

U.K. Gross Domestic Product (GDP) YoY, Q1 2020(see more posts on U.K. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| The UK has indicated it will maintain a light touch customs requirement next year but is set to confirm it has no intention to seek an extension of the transition period. |

U.K. Manufacturing Production YoY, April 2020(see more posts on U.K. Manufacturing Production, ) Source: investing.com - Click to enlarge |

| The latest round of trade talks ended last week with little progress. The pace of negotiations will be increased, and a meeting between Prime Minister Johnson and EU’s von der Leyen may help reinvigorate the talks. |

U.K. Trade Balance, April 2020(see more posts on u-k-trade-balance, ) Source: investing.com - Click to enlarge |

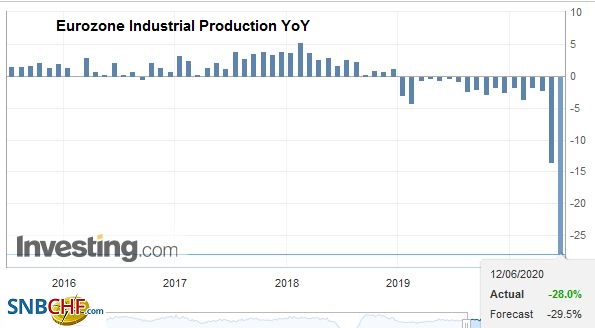

| The eurozone’s industrial output fell 17.1% in April after an 11.3% decline in March. The April drop was smaller than expected and may have something to do with seasonal adjustments. Note the national figures. Germany reported a 17.9% decline, and Italy’s industrial output fell 19.1%. French industrial production contracted 20% and Spain’s by nearly 22%. The two EMU highlights for next week are the ECB’s TLTRO with can provide loans for a little as minus 100 bp, and the EU Summit to discuss the 750 bln euro Recovery Fund. |

Eurozone Industrial Production YoY, April 2020(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

The euro eased to almost $1.1275 in Asia before recovering to $1.1340. However, the market appears to be waiting for US leadership now. Initial support is seen around $1.1300, and there is an option for almost 610 mln euros at $1.1310 that expires today. The euro has declined in one session this week and in each of the past two. It closed near $1.1290 last week. A gain this week would be the fourth in a row, the longest in more than two years. For its part, sterling fell to about $1.2545 earlier today before finding a bid that lifted it a cent by late morning turnover in the UK. Yesterday’s 1.1% slide snapped a 10-day advance that saw it rise by around four cents. Resistance is seen in the band between $1.2650 and $1.2680.

America

The US reports import/export prices, University of Michigan’s preliminary June reading, and the Baker Hughes rig count. These are not typically market-moving reports even in the best of times. Investors are more focused on what appears to be a resurgence in Covid cases, and Houston is reportedly considering reimposing stay-in-place orders. Canada and Mexico do not have market-moving economic reports either.

The Federal Reserve’s balance sheet rose by $3.7 bln last week, its smallest increase since the crisis began. About a third of the increase was accounted for by the $1.2 bln purchases of the corporate bond ETFs. Yesterday, during the equity carnage, the Fed announced adjustments to its repo operations starting next week. The overnight repo will be conducted at a minimum of five basis points over the interest on reserves, and the one-week repo will be at a minimum of 10 bp on top of interest on reserves. The Fed cited better functioning markets for its decision.

Central banks had sold about $155 bln of Treasuries out of the custody holdings maintained at the Fed during the peak of the panic in March and April. Last week, they bought $17.5 bln back to bring their nine-week buying spree to roughly $97 bln. There are at least two takeaways. First, the divestment was tactical, not strategic. Second, the replenishing of reserves requires selling their own currency to buy dollars, hence what appears to be stepped up intervention.

The US dollar reached almost CAD1.3315 in the middle of the week, its lowest level since early March. Yesterday’s sharp recovery was extended to about CAD1.3665 today before it pulled back, reaching CAD1.3530 in Europe. There is an option for roughly $540 mln at CAD1.35, which could be in play before expiring later today. That also corresponds to the midpoint of this week’s range. Below there, the next target is near CAD1.3450. The greenback had been carving out a shelf a little below MXN21.50 before surging to almost MXN22.80 yesterday and MXN22.95 earlier today. However, it has come back offered. The initial corrective target is near MXN22.38 and then MXN22.20. While the peso’s 1.4% decline so far this month is the largest among emerging markets currency, the Brazilian real’s 7.25% gain is the most. However, Brazil was closed for a national holiday yesterday and missed the drama. A little catch-up today ought not to surprise.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, January 13: Dismal Data Undercuts Sterling and Boosts Chances of a Rate Cut

FX Daily, January 13: Dismal Data Undercuts Sterling and Boosts Chances of a Rate Cut

Overview: There are two big stories today. The first is the large scale protests in Iran after the government admits to accidentally shooting down the commercial airliner amid the fog of war. The market impact seems minimal but fueling speculation that this, coupled with the economic hardship related to the US embargo, could topple the regime. Second, the UK reported that the economy unexpectedly contracted in November.

FX Daily, December 20: Sterling Trades Higher after Test on $1.30

FX Daily, December 20: Sterling Trades Higher after Test on $1.30

Overview: The holiday mood has tightened its grip on the capital markets, and global investors have nearly completely ignored the impeachment of the US President as it has little economic or policy significance. US equities reached new record highs yesterday with the S&P 500 moving above 3200.

FX Daily, January 20: Stocks Stall while the Dollar Remains Bid

FX Daily, January 20: Stocks Stall while the Dollar Remains Bid

Overview: The new week is off to a quiet start as the US celebrates Martin Luther King’s birthday, and investors look for a fresh focus. Hong Kong and Indian markets were suffered modest declines while most of the other large Asia Pacific markets edged higher. European stocks are trading a little lower, and the Dow Jones Stoxx 600 is threatening to end a four-session advance. Most benchmark bond yields around half a basis point in one direction or the other.

FX Daily, February 11: New Calm in the Capital Markets Continues, Powell Moves to Center Stage

FX Daily, February 11: New Calm in the Capital Markets Continues, Powell Moves to Center Stage

Overview: Investors are taking solace from reports indicating that the increase in the new coronavirus at ground zero (Hubei) is slowing. After the S&P 500 reversed early losses yesterday to close at new record highs helped keep the bullish sentiment intact. Benchmarks in Hong Kong, South Korea, Australia, and China rose for the sixth session.

FX Daily, March 11: US Over-Promises and Under-Delivers, while BOE Steps Up with 50 bp Rate Cut

FX Daily, March 11: US Over-Promises and Under-Delivers, while BOE Steps Up with 50 bp Rate Cut

Overview: The S&P 500 and Dow Jones Industrials sold off after the higher open and briefly traded below yesterday’s lows. Investors seemed disappointed that the Trump Administration was not ready with specific policies after Monday’s tease that had initially helped lift Asia Pacific and European markets earlier on Tuesday. This sparked a sharp decline in Europe into the close.

FX Daily, May 13: Will Powell have any more Luck Pushing against Negative Rate Expectations in the US?

FX Daily, May 13: Will Powell have any more Luck Pushing against Negative Rate Expectations in the US?

Overview: Another late sell-off in US shares, this one perhaps related to the sobering assessment by the leading medical adviser for the Trump Administration about the risks of opening too early, failed to deter investors in the Asia Pacific region. Although Japanese shares slipped, most other markets rose. India led the way (~2%) after a fiscal stimulus program was announced.

FX Daily, June 3: Dollar is Sold and ROW is bought

FX Daily, June 3: Dollar is Sold and ROW is bought

Overview: Two recent trends continue. Equities are moving higher, and the dollar remains heavy. Equity markets in the Asia Pacific region rose at least one percent, and South Korea, Singapore, and Malaysia rallied 2-3%. Europe’s Dow Jones Stoxx 600 is up more than 1% for the third consecutive session. US shares are trading higher and are poised to extend their recent run.

FX Daily, June 5: Greenback Remains Soft Ahead of Employment Report, but Reversal Possible

FX Daily, June 5: Greenback Remains Soft Ahead of Employment Report, but Reversal Possible

The modest loss in the S&P 500 and NASDAQ yesterday did not signal the end of the bull run. All the markets in the Asia Pacific region rallied, with the Hang Seng among the strongest with a 1.6% advance that brought the week’s gain to around 7.8%. South Korea’s Kospi was not far behind with a weekly gain of 7.5%. In the past two weeks, the MSCI Asia Pacific Index is up nearly 10%.

Tags: #USD,Bank of England,Bank of Japan,Currency Movement,EUR/CHF,Eurozone Industrial Production,Featured,FX Daily,newsletter,U.K. Gross Domestic Product,U.K. Manufacturing Production,U.K. Trade Balance,USD/CHF