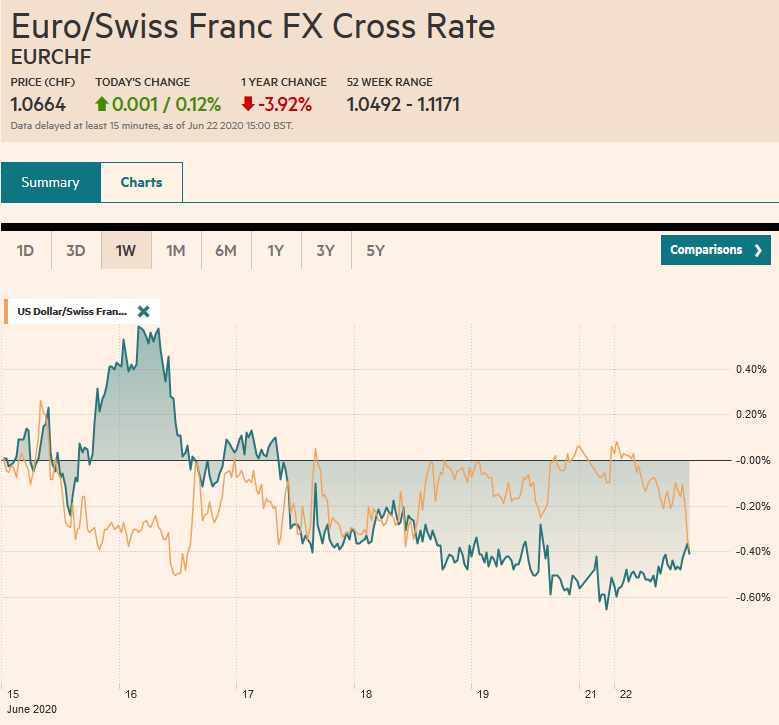

Swiss Franc The Euro has risen by 0.12% to 1.0664 EUR/CHF and USD/CHF, June 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Investors begin the new week, perhaps slowed a bit by the weekend developments and the growth of new infections. Equities are mixed. The MSCI Asia Pacific Index snapped a four-day advance, though India bucked the regional trend and gained 1%. Europe’s Dow Jones Stoxx 600 is recovering from an early dip to four-day lows. US shares are trading higher after the S&P 500 closed below 3100 ahead of the weekend after reaching 3155. That may provide a cap, while it takes a move above 3181.50 to signal the bull move has resumed. The bond market is quiet, and peripheral European bonds continue

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of England, China, COVID-19, EUR/CHF, Eurozone Consumer Confidence, Featured, Federal Reserve, FX Daily, Hong Kong, newsletter, South Korea, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.12% to 1.0664 |

EUR/CHF and USD/CHF, June 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Investors begin the new week, perhaps slowed a bit by the weekend developments and the growth of new infections. Equities are mixed. The MSCI Asia Pacific Index snapped a four-day advance, though India bucked the regional trend and gained 1%. Europe’s Dow Jones Stoxx 600 is recovering from an early dip to four-day lows. US shares are trading higher after the S&P 500 closed below 3100 ahead of the weekend after reaching 3155. That may provide a cap, while it takes a move above 3181.50 to signal the bull move has resumed. The bond market is quiet, and peripheral European bonds continue to outperform the core. The US benchmark is virtually unchanged near 69 bp. The dollar is softer, with the Scandis and Antipodeans leading the move. The dollar is though holding its own against the Japanese yen. Emerging market currencies are mixed. The Mexican peso and central European currencies are advancing, while Asian currencies, Turkey, and South Africa are heavy. Gold set a new high for the month (~$1758) and backed off before testing last month’s high (~$1765). August WTI continues to flirt with the $40-a-barrel level but has been unable to close above it. |

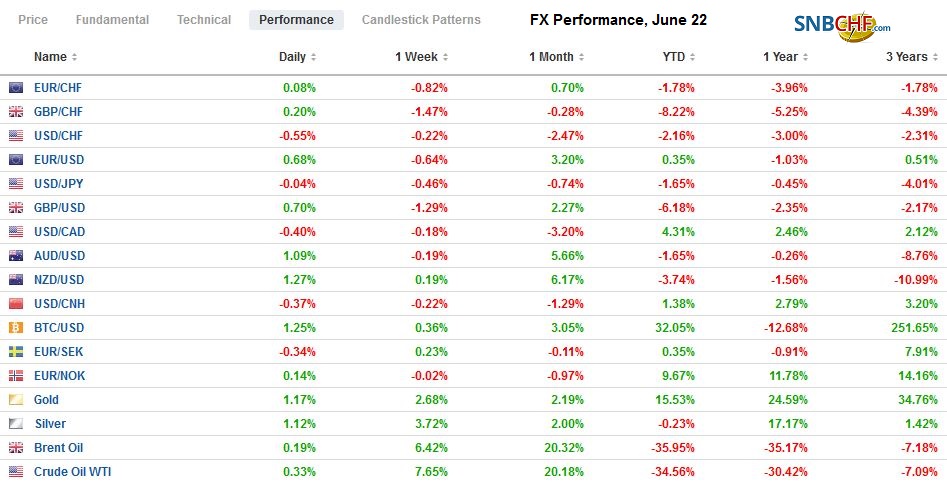

FX Performance, June 22 - Click to enlarge |

Asia Pacific

China suspended some imports from Tyson Foods after a cluster of the virus was discovered. A Pepsi snack-making factory was closed Sunday because of the virus. The number of new cases in Beijing reportedly declined. Germany is also experiencing a flare-up of cases and infections rose Sunday for the third consecutive day. US infections rose by the most in three weeks on Saturday, concentrated in the Sun-Belt states and California. Brazil has over a million cases, and fatalities surpassed 50k. Mexico has reported its second-highest daily deaths.

Hong Kong unions and students failed to get the support that they required to strike against the security law. At the same time, the coronavirus restrictions prohibit large gatherings and prevent securing the necessary permits. A new spark may be needed, but the kindling remains dry. The first actions under the security law could serve the purpose. Still, some suspect that the lack of widespread demonstrations will hint at a different strategy: emigration. Meanwhile, Hong Kong forwards, which is where the negative pressure is seen, normalized or nearly so, but appear poised to rise again. Separately, HKMA has had to fight a sustained campaign to prevent the US dollar from falling through its lower end of the currency band. The pressure comes from the mainland for HK IPOs and some flows drawn to the higher yields.

Intra-regional Asian trade remains challenged. South Korea reported exports in the first 20-days of June fell 12% year-over-year, which represents an improvement of over a nearly 20% fall in the first 20-days of May. However, the slowing chip exports (2.6% vs. 13.4%) was troubling and may have weighed on both the Kospi and the won. On Saturday, Taiwan disappointed with a May export orders rose 0.4% year-over-year, after a 2.3% gain in April.

The dollar has been confined to about a quarter of a yen below JPY107.00. It is going nowhere quickly. Last week’s range was roughly JPY106.65-JPY107.65. The Australian dollar finished last week on its lows, and initial follow-through selling saw it reach a five-day low near $0.6800 before rebounding. The pre-weekend high was set just north of $0.6910, and a push through here today, especially on a closing basis, would be constructive. That said, the intraday technicals warn that it may be stretched. The PBOC set the dollar’s reference rate a touch firmer than the models suggested and kept its Loan Prime Rate unchanged. Note that the PBOC is one of the few large central banks not engaged in quantitative easing (long-term asset purchases), and the premium it pays over 10-year Treasuries is around 220 bp, the most since 2011.

EuropeWirecard, the wunderkind of German finance, collapsed. The CEO resigned, unable to account for a quarter of the balance sheet (~1.9 bln euros). Ahead of the weekend, its bonds offered similar yields as Hertz, according to Bloomberg. This is the third corporate challenge to the German corporate governance and regulatory regime after the emissions scandal and the billions in fines and legal settlements levied against Deutsche Bank. The new Bank of England Governor Bailey has indicated his first break from his predecessor Carney. Carney wanted to wait until rates had risen to 1.5% before allowing the balance sheet to shrink. Bailey argued that the balance sheet should be trimmed before rates increase. It still seems the eventuality is still some time off, as in more than a year. Meanwhile, the Chancellor of the Exchequer Sunak is considering an emerging cut in the value-added tax to help spur the economy. Separately, the UK signaled it will relax trade controls that will apply to the EU (but not Northern Ireland) for the first half of next year and will boost spending by GBP50 mln to prepare the necessary customs intermediaries. It may need to hire 50k more custom agents. Sensitive products that involve products of plant or animal origins, and especially poultry and fish, may still face delays. Prime Minister Johnson suggests an agreement by the end of next month is possible. |

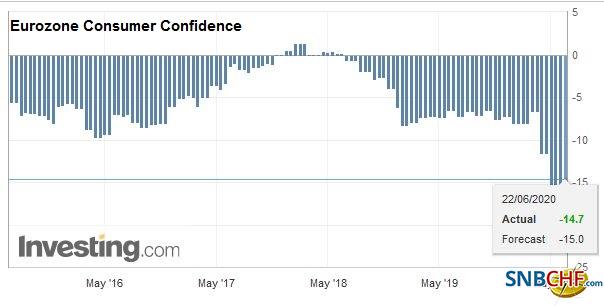

Eurozone Consumer Confidence, June 2020(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

Italy is also reportedly considering an emergency cut in the VAT for some strikes parts of the economy, including restaurants, tourism, clothing, and cars. It is preparing for a larger budget shortfall this year. Separately, the ECB’s record (minutes) from its recent meeting will be published later this week, and it may contain a section that discusses proportionality that the Bundesbank can pass on to Berlin to address the German Constitutional Court ruling. However, if it is too overt, it would seem to give credence to the idea that the German Constitutional Court can overrule the European Court of Justice.

The euro held its pre-weekend low by a hundredth of a penny ( a little below $1.1170), according to Bloomberg, and rose briefly through $1.1225in early European turnover. The intraday technicals are stretched, and optionality may help cap the upside. There are options for about 1.75 bln euros struck in the $1.1200-$1.1205 area that expire today and about 850 mln more euros at $1.1250. In addition, there are options for 1.8 bln euros at GBP0.9060 that expire today. The euro ran out of stream near GBP0.9070 earlier. The pre-weekend low was near GBP0.9000, and that maybe the near-term risk. Sterling itself is snapping a four-day downdraft against the dollar after first extending the losses to about $1.2335 before finding bids that lifted a cent off its lows before sellers reemerged.

America

The fact that the Fed’s balance sheet shrank last week for the first time since the end of February has little significance. The normalization of market functions has reduced the need for the swap lines by foreign central banks. Only a fraction of the maturing swaps is rolled forward. Still, the signal should not be lost. The Federal Reserve still has the monetary spigot wide open, and its balance sheet will increase. Treasuries, with purchases at $80 bln a month, will account more a smaller part of the new asset accumulation. Balance sheet growth is still the signal. Don’t be distracted by the noise. Meanwhile, the Treasury will be bringing to market $155 bln in coupons and around $170 bln in bills this week. Into the end of the month, quarter-end, some auctions may appear “sloppy.”

The US reports existing home sales for May. Recall last week, housing starts disappointed. Existing home sales are expected to have fallen for the third consecutive month. The anticipated pace of 4.09 mln (seasonally-adjusted annual rate) would be the lowest since 2011. Tomorrow sees the preliminary PMI, where the composite is expected to rise for the second consecutive month, and the median forecast in the Bloomberg survey is for the manufacturing PMI to reach the 50-level. Canada has a light economic calendar this week. The highlight for Mexico is the Banxico meeting on June 25 that is expected to result in a 50 bp rate cut (to 5.0%). Note that Argentina has extended the deadline for bondholders for the fifth time, now until late July, as it tries to reschedule its dollar debt.

The US dollar rose to a five-day high of CAD1.3630 earlier today but has come back offered. It was sold down to about CAD1.3560 in the European morning. The intraday technical indicators warn that the greenback may recover in the North American morning. The CAD1.3600 area is the middle of today’s range. The dollar traded in MXN22.1960 to almost MXN22.83 range on June 18 and remained in the range ahead of the weekend and thus far today. It needs to resurface above MXN23.00 to confirm a low is in place.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, June 16: Correction Scenario Tested

FX Daily, June 16: Correction Scenario Tested

Overview: Shortly after the US stock market opened sharply lower, the Federal Reserve announced that it’s Main Street facility was up and running. US stocks never looked back. After the S&P 500 recouped its full decline, the Fed announced it would begin buying corporate bonds. Up until now, it had been buying representative ETFs. Stocks rallied further on the news before pulling back into the close. The rally in risk assets carried into Asia.

FX Daily, January 17: China and the UK Surprise in Opposite Directions

FX Daily, January 17: China and the UK Surprise in Opposite Directions

Overview: Helped by new record highs in the US, global stocks are moving higher today. Nearly all the markets in the Asia Pacific region advanced and the seventh consecutive weekly rally is the longest in a couple of years. Europe’s Dow Jones Stoxx 600 is at new record highs and appears set to take a four-day streak into next week. US shares are trading firmly.

FX Daily, January 29: Escaped from a Crocodile’s Mouth, Entered a Tiger’s Mouth

FX Daily, January 29: Escaped from a Crocodile’s Mouth, Entered a Tiger’s Mouth

Overview: This colorful Malay saying captures the spirit of the animal spirits. Narrowly escaping an escalation of a trade war between the world’s two largest economies, the outbreak of a deadly virus has spurred moves, especially the sell-off in stocks and rally in bonds, for which many investors seemed ill-prepared. Even though the virus contagion has not peaked, the recovery in US equities yesterday points to a break the fear and anxiety.

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

Overview: The ring of containment of Covid-19 has grown from China. The new frontline is Japan, South Korea, Italy, and Iran. A lockdown of around 50k people near Milan and Austria blocking trains from Italy is scaring investors. Asian markets fell, but South Korea bore the brunt with a nearly 4% decline. The national holiday in Japan spared local equities.

FX Daily, February 26: Dramatic Investor Adjustment Continues

FX Daily, February 26: Dramatic Investor Adjustment Continues

Overview: The warning by the US Center for Disease Control and Prevention that Americans should prepare for an outbreak of Covid-19 sent the S&P 500 tumbling to an 11-week low and the 10-year Treasury yield to a record low near 1.30%. The volatility of the S&P (VIX) jumped to its highest level since 2018. The sell-off in global equities continues unabated.

FX Daily, February 28: Fallout Accelerates

FX Daily, February 28: Fallout Accelerates

Overview: The dramatic response by investors to Covid-19 continues unabated and worse. The slide is accelerating. The S&P 500 posted a 4.4% loss yesterday, its worst session since 2011, and the sell-off is continuing. Many markets in Asia Pacific, including Japan, China, Korea, Australia, India, Singapore, and Thailand, fell by more than 3%.

FX Daily, April 30: ECB Takes Center Stage

FX Daily, April 30: ECB Takes Center Stage

Overview: Equities continue to recover even as deep economic contractions are reported. Yesterday, the US said Q1 GDP contracted at an annualized pace of 4.8%, while the eurozone reported today that output fell 3.8% quarter-over-quarter in Q1. Hong Kong and South Korea were closed, but the rest of the Asia Pacific bourses rallied strongly with several, including Australia and India, rising more than 2%.

FX Daily, May 27: China and Hong Kong Pressures are Having Limited Knock-on Effects

FX Daily, May 27: China and Hong Kong Pressures are Having Limited Knock-on Effects

Overview: The S&P 500 gapped higher yesterday, above the recent ceiling and above the 200-day moving average for the first time since early March. The momentum faltered, and it finished below the opening level and near session lows. The spill-over into today’s activity has been minor. The heightened tensions weighed on China and Hong Kong markets, but Japan, South Korea, Taiwan, and Indian equity markets rose.

Tags: #USD,Bank of England,China,COVID-19,EUR/CHF,Eurozone Consumer Confidence,Featured,federal-reserve,FX Daily,Hong Kong,newsletter,South Korea,USD/CHF