The US-China tensions remain the dominant driver of investor risk appetites. President Trump has repeatedly accused China of manipulating its currency on twitter, and finally Treasury Secretary Mnuchiin acquiesced after China failed to prevent the dollar from rising above CNY7.0. China set the reference rate for the dollar lower than models based on the basket the PBOC uses implied for the past three sessions, and this helped stabilize the situation. Contrary to expectations, China is showing great restraint and still managing the pressure on the yuan. In the US, the end of the tariff truce was understood to undermine Fed Powell’s message that the rate cut at the end of July was a mid-course correction. Investors

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China, EMU, Featured, Federal Reserve, Italy, newsletter, US

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The US-China tensions remain the dominant driver of investor risk appetites. President Trump has repeatedly accused China of manipulating its currency on twitter, and finally Treasury Secretary Mnuchiin acquiesced after China failed to prevent the dollar from rising above CNY7.0. China set the reference rate for the dollar lower than models based on the basket the PBOC uses implied for the past three sessions, and this helped stabilize the situation.

Contrary to expectations, China is showing great restraint and still managing the pressure on the yuan. In the US, the end of the tariff truce was understood to undermine Fed Powell’s message that the rate cut at the end of July was a mid-course correction. Investors took US rates sharply lower. Consider that on the day the Fed announced its first rate cut since 2008, the January 2020 fed funds futures contract closed with an implied yield of 1.805%. Now it is at 1.51%.

The market understood the end of the tariff truce was going to undermine Chinese growth. Stocks fell, and yields eased. Most emerging market currencies were sold as investors had to discount further escalation, which dampened risk appetites. What ultimately led to Mnuchin’s declaration was that the PBOC chose not to stand in the way of the yuan absorbing some of the pressure.

Many observers recognized that due to the trade imbalance, the US would dominate an escalation of tariffs. The takeaway, judging from much of the American press was the US would win a trade war. The takeaway from the realpolitik perspective is that China would jump to another escalation ladder. What is restraining China is the one and perhaps only relevant thing in such matters: self-interest.

ChinaChinese officials recognize that a devaluation of the yuan would be counter-productive. Why would the Chinese government want to encourage Chinese business to rely on US markets? If Chinese companies wanted to maintain market share in the US, they would reduce prices, but they haven’t. A little depreciation eases the pressure and sends signals to Chinese corporates who have something on the magnitude of $870 bln of hard currency debt, mostly US dollars (BIS). Chinese officials had already warned that the CNY7.0 level should not be regarded as a red line. It used the end of the tariff truce to do what it wanted to do, and that is to remove the significance of the CNY7.0 level. Similarly, President Trump seemed to box himself in with offers to grant licenses to US companies to sell some products and services to Huawei. There was some backlash, including from Democrats whom Trump likes to spin as softer on China. This seeming confusion of commercial and security issues did not sit right. On the other hand, disengagement would likely hasten the development of parallel products and services, leading to a fork in the internet, we have discussed previously. There has been virtually no progress on the licenses or even the process since it was announced, which like the lack of Chinese purchases of US agriculture, builds the cathedral of mistrust. The formal announcement that this would be frozen, simply confirms the facts on the ground, and like the labeling China a currency manipulator is more symbolic than substantive. However, Trump is out of the corner he had painted himself into with Huawei. China does not seem to be in a particular hurry to easy policy. The decline in the PPI on a year-over-year basis, the first in three years, maybe an added incentive as it points to a profit-squeeze and deflationary pressure. The string of July data due out in the coming days includes investment, industrial production, and retail sales. The sluggish pace (for China) is set to continue. The most important thing for market participants next week will not be the monthly data points, but the daily fix. The PBOC sets the reference rate for the dollar-yuan rate at 9:15 pm ET. The dollar is permitted to trade 2% on either direction away from the reference rate. It rarely does. In fact, last week, when the dollar rose through CNY7.0, the dollar rose 1.8%, one would have thought the sky was falling. Other currencies are allowed to move in a wider band, and one of the moves that we suspect China may consider is to widen the dollar band. In the current context, it would be seen as a signal of willing to allow the yuan to fall faster. Economists have developed models that allow them to forecast the fix. The one factor that cannot be modeled is the “counter-cyclical adjustment factor,” which seems subjective. Therein lies the signal. When the fix is set weaker for the dollar than the models suggest, the PBOC is leaning against the current. When the fix sets the dollar stronger, the PBOC is signaling it is willing to accept more yuan weakness. The fact that the dollar is trading firmer (than the fix) demonstrates the upside pressure has not been extinguished. |

Economic Events China, Week August 12 - Click to enlarge |

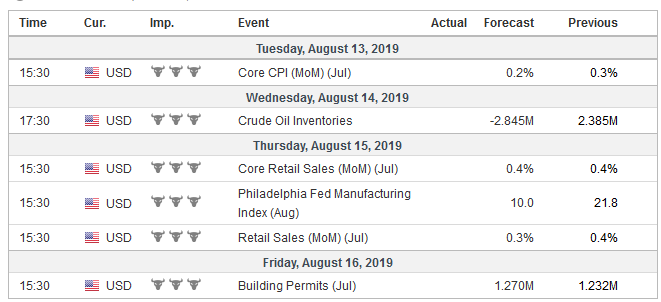

United StatesIn addition to, and not wholly separate from the conflict between the two largest economies, investors are concerned about the trajectory of growth and prices, and policymakers’ reaction function. The Federal Reserve acts as if it were dealt a fait accompli by the disruptive trade policy. This may dampen investor interest in the upcoming data that includes CPI, industrial production, and retail sales. The August Empire and Philadelphia surveys may attract some attention but are unlikely to shake perceptions that the economy is tracking a little below 2%, which is where the Fed has identified as trend-growth or the non-inflationary pace. Investors remain unswayed by cautionary comments from St. Louis Fed President Bullard who has been the leading dovish member of the FOMC. He supported the mid-course correction framing of the issue and again suggested that one more cut in Q4 may be appropriate. The January 2020 fed funds futures contract, which offers arguably the most transparent view of market expectations for the end of this year, implies about a 1.50% average rate in December. The current average effect fed funds rate is about 2.12%. The market has two more cuts completely discounted and is roughly split on a third, which would be a 25 bp move at each of the remaining meetings this year. |

Economic Events: United States, Week August 12 - Click to enlarge |

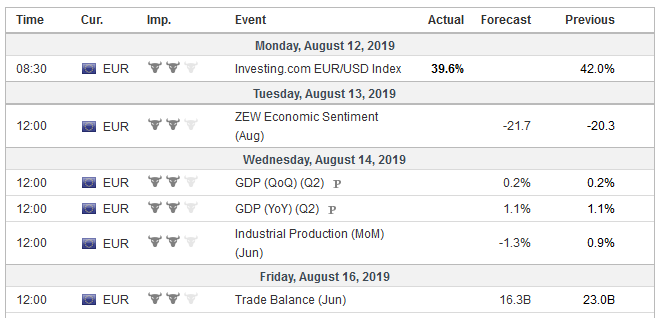

EurozoneEuropean news continues to get worse. Germany and France reported outsized drops in June industrial production, which underscore that Q3 has begun with weak momentum. Germany, the world’s fourth-largest economy, maybe slipping into its second consecutive quarterly decline. Germany reports Q2 GDP on August 14. The median forecast in the Bloomberg survey for 0.1% contraction may prove to be optimistic. |

Economic Events: Eurozone, Week August 12 - Click to enlarge |

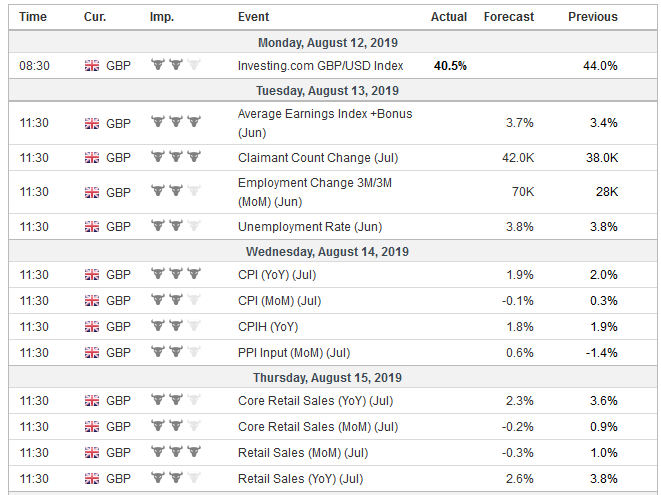

United KingdomThe Brexit debate is not happening between the UK and EC. They are talking past each other. The UK says that agreement that the previous government and some members of the current government negotiated for 18-months is rubbish. The new government wants to renegotiate jettisoning the backstop that the UK initially requested to enforce the Good Friday Agreement. The market has become more convinced that the UK will, in fact, leave the EU at the end of October. On PredictIt.Org, the odds have steadily climbed in recent weeks from about a one-in-three chance at the end of June to a slight favorite (57%). Instead, the UK continues to debate itself. When Parliament returns in early September, a vote of confidence will be held. Rarely has a British government lost a vote of confidence in modern times, but yes, this time could be different. The Tories have a one-seat working majority and an angry moderate-wing on the backbenches. The question arises if Johnson loses the vote, then what? An election must be held by early November, and Johnson could still lead the UK out without a deal at the end of October. A way out is if a new government could be cobbled together just to lead to elections and put in a new Prime Minister. Labour’s leader would be a reasonable choice in other circumstances, but Corbyn is too divisive, and a majority would not back him. Can a majority of MPs from across party lines put aside their differences and form a national unity government? And if, beyond the laws of probability, they do this, to what end? Revoke Article 50 and have half the country yelling foul? Seek a postponement of the exit date until some time after the next government takes office? And what really changes besides the extension of uncertainty that is paralyzing the economy, as the 0.2% contraction in Q2 GDP reported ahead of the weekend demonstrates. Market sentiment is gradually moving towards a rate cut by the BOE by the end of the year. Interpolating from derivatives suggest a 57% chance of a cut. Meanwhile, the realignment the sterling/euro exchange rate continues. The euro has climbed for 14 consecutive weeks against sterling and is at levels not seen for 3-4 years (almost GBP0.9300) and before that, the Great Financial Crisis. More broadly, sterling’s broad trade-weighted index has fallen by about 7.5% over the past three months. Given the exposure of the UK economy (imports plus exports), the currency realignment may be worth around 100 bp of easing. It will likely boost measured inflation. Whether it helps trade may depend more on demand than price. |

Economic Events: United Kingdom, Week August 12 - Click to enlarge |

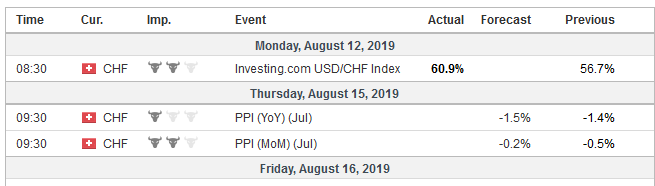

Switzerland |

Economic Events: Switzerland, Week August 12 - Click to enlarge |

If slumping economies and Brexit uncertainties were not sufficiently challenging, Italy’s simmering political tensions boiled over. League leader Salvini withdrew support from the government and demanded snap elections, which would likely mean October 13 or October 23. Salvini is feeling his oats. The League is said to be polling near 40%, and it did well in EU Parliament elections. The opposition seems weak. For several months, Salvini has teased his supporter and adversaries about forcing elections. The markets responded as one might imagine. It took Italian yields higher and equities, especially bank shares lower. The cost of insuring Italy’s debt (credit default swaps) rose sharply.

Although Salvini is toppling the government, he loses some control of the situation going forward. As we suggested was the case in the UK, the issue is whether another majority can be forged out of the existing parliament. Before elections, it would be helpful to do two things: approve the 2020 budget and some political reforms, like reducing the number of deputies.

For the past three weeks, one would pay Italy to lend it for two years. Now one earns three basis points. Italy’s 10-year yield jumped more than 40 basis points since it bottomed in the middle of last week after successfully testing the July low a little below 1.40%. The yield has not been lower since 2016. It had been halved from the mid-May highs, and now yields can push back toward 2.00%-2.25% despite a resumption of QE and TLTROs. Political risk is an economic risk in Italy where the confidence of investors is needed or the debt-burden, and slow growth makes for a lethal cocktail.

Tags: Brexit,China,EMU,Featured,Federal Reserve,Italy,newsletter,US