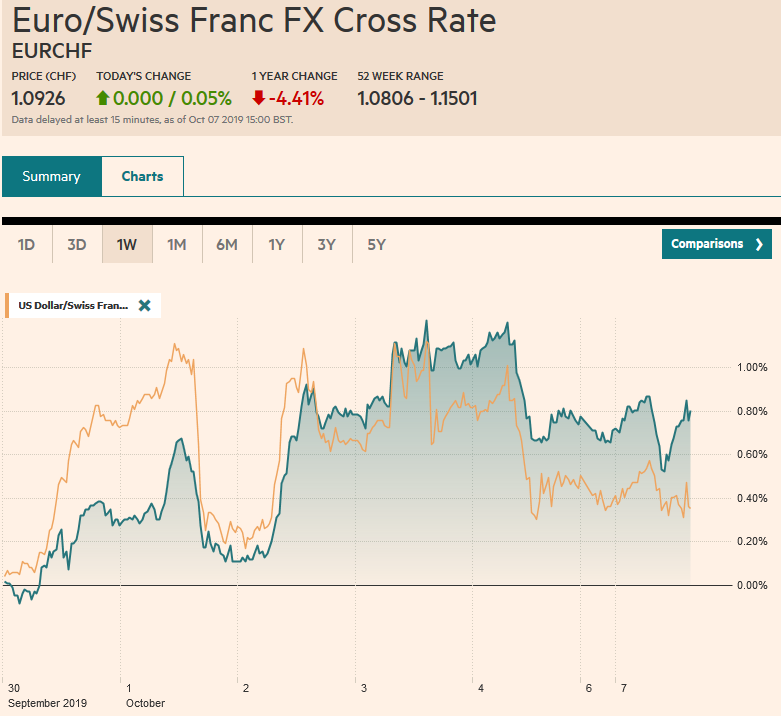

Swiss Franc The Euro has risen by 0.05% to 1.0926 EUR/CHF and USD/CHF, October 7(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The global capital markets are uneasy as the risks that have dominated investors’ concerns–trade and Brexit–remain front and center today. Expectations are low that this week’s talks between the US and China will lead to a breakthrough or will be sufficient to postpone further the next round of tariff increases set for next week. The UK government has indicated it will challenge Parliament’s effort to block a no-deal exit to the Supreme Court. Equities in Asia Pacific mostly higher, except for Japan and Indonesia. China and Hong Kong were closed. European shares initially advanced

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Brexit, China, Currency Movement, EUR/CHF, Featured, FX Daily, newsletter, Turkey, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.05% to 1.0926 |

EUR/CHF and USD/CHF, October 7(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The global capital markets are uneasy as the risks that have dominated investors’ concerns–trade and Brexit–remain front and center today. Expectations are low that this week’s talks between the US and China will lead to a breakthrough or will be sufficient to postpone further the next round of tariff increases set for next week. The UK government has indicated it will challenge Parliament’s effort to block a no-deal exit to the Supreme Court. Equities in Asia Pacific mostly higher, except for Japan and Indonesia. China and Hong Kong were closed. European shares initially advanced but by late morning were little changed, while US shares have a clear weaker bias, and the S&P 500 is trading nearly 0.5% lower. Bond yields are 1-2 bp softer, leaving the US 10-year a little above 1.50% and the 10-year German Bund around minus 60 bp. The risk-off mood is evident in the foreign exchange market, where the yen and Swiss franc are outperforming, and the dollar-bloc, Scandis, and sterling are underperforming. Emerging market currencies, led by the large accessible currencies, including the Turkish lira, South African rand, are under pressure. Gold and oil are little changed. |

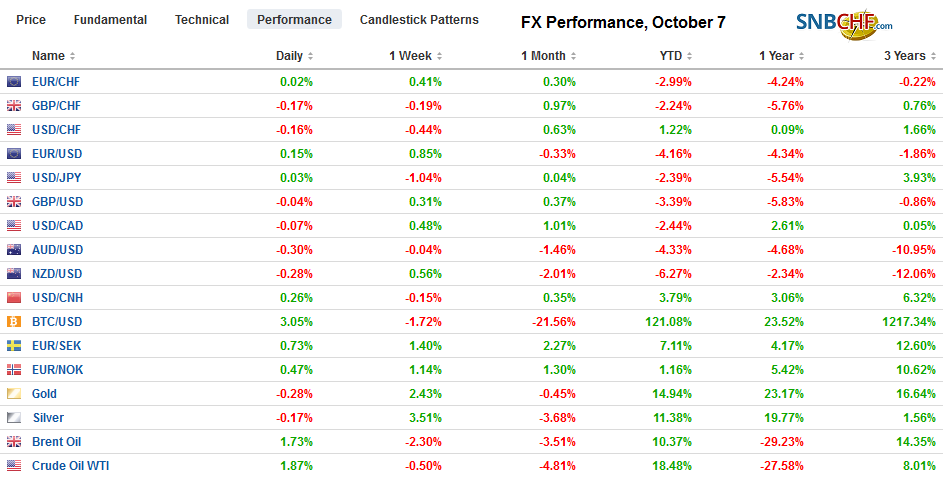

FX Performance, October 7 - Click to enlarge |

Asia Pacific

Beijing has moved to lower expectations for the talks that will be held in Washington toward the end of the week. Vice-Premier He, who leads the Chinese delegation, has reportedly indicated that it will not agree to reform China’s industrial policy or state subsidies, which appear to have grown or broadened under President Xi. In itself, it does not seem new but underscores the challenge to a broad agreement. One cannot count on any goodwill from either side. Only self-interest can be relied upon. Suffering from a protein shortage, China needs US meat and soy. With a nearly insatiable appetite for energy, it is willing to buy US crude and some products. It can make some concessions on intellectual property rights with little cost as it has denied wholesale violations and state-sponsored theft from the get-go. It is not clear what China wants in exchange, besides a rollback of US tariffs. China’s trade surplus has risen during the trade conflict with the US, while the US trade deficit has grown more than 10%.

China’s reserves slipped in September by $15 bln to $3.092 trillion. It does not reflect a material change. Instead, it likely is a result of valuation adjustments. Other reserve currencies, like the euro and yen, weakened against the dollar (-0.75% and -1.6%, respectively). Reserves are invested in bonds and bonds sold off in September. The US 10-year Treasury yield rose 17 bp, and the Germany Bund yield rose 13 bp.

North Korea says the talks with the US broke down on Saturday. The North Korean foreign ministry claimed that the negotiations were really about US domestic politics. The US offered a different take. It described the talks as a “good discussion.” Which interpretation is correct will be known in two weeks, when Sweden offered to host the second round of negotiations.

The dollar is recording a lower high against the yen for the fourth consecutive session. Today it barely poked above JPY107.00. There are about $1.2 bln in options set to expire today in the JPY107.00-JPY107.10 area. There is another set of options (JPY106.70-JPY106.85) for about $2 bln also will be cut today. That said, the dollar appears to be losing its downside momentum against the yen, and the JPY106.50 area is key now. The Australian dollar rallied 1% in the last three sessions is giving half of its back here today. It has retraced (38.2%) of those gains around $0.6735. The next retracement targets are near $0.6720 and $0.6710. The US dollar eased by about 0.5% against the offshore yuan (CNH) in the last two sessions last week and is about 0.3% firmer today near CNH7.1350.

Europe

The UK Government told a Scottish court last week that it will follow the law that Parliament approved and request a delay in Brexit if a deal is not reached in a couple of weeks (October 19). Prime Minister Johnson and government officials continue to claim to prefer to be “dead in a ditch than request an extension.” Ireland’s Prime Minister suggested over the weekend that the UK is likely to make a new offer by the end of the week. Most key officials saw last week’s proposal as insufficient in its present form. A survey by Bloomberg found that the median forecast sees sterling falling by around 10% on a no-deal exit.

German factory orders fell 0.6%, which was twice the decline expected by the median forecast in the Bloomberg survey. The July decline was revised to a 2.1% decline rather than 2.7%. It puts the year-over-year contraction at 6.7%, down from the revised 5% decline in July. The year-over-year decline was the 15th in a row. There were a couple of bright spots in the disappointing report. First foreign orders increased (0.9%) but not to offset the 2.6% drop in domestic orders. Second, orders for basic goods increased by 1.1% (July -1.5%) and the reductions in investment and consumer goods moderated from July. Germany reports August industrial output figures tomorrow, and a small decline is forecast.

Portugal’s Socialist Prime Minister Costa, who governs from the center, helped secure a larger plurality in Parliament, though still shy of an outright majority. The Socialists garnered a little more than a third of the vote while the center-right PD took a bit a quarter of the vote. Costa will have a slightly stronger hand in negotiating with the smaller parties in the governing coalition (the Left Party and Communist/Greens. The Socialist may have won about 106-108 of the 230 seats. Even if a majority is secured, Costa could choose to keep an alliance that protects his left flank as the centrist fiscal policy may be more difficult to abide if the economy continues to slow.

Turkey is expected to strike at Kurdish fighters in Northern Syria. Although the Kurds had been allies of the US, the Trump Administration has reportedly approved of Turkey’s actions. The US promised to remove US troops from the combat area and indicated it will not “support or be involved in the operation.” The US also announced that Turkey would be responsible for the captured Isis fighters that have been captured. This is seen as a major reversal of US policy. In 2015, the US gave air support to the Kurds in Syria and had allied with them to fight Isis. The Turkish lira is the weakest of the emerging market currencies today, losing about 0.8%. The US dollar is trading at the upper end of a three-week range (~TRY5.75).

The euro is trading within the pre-weekend trading range, which itself was inside the October 3 range of roughly $1.0940 and $1.10. It approached $1.0960 in the European morning, where an option for about 965 mln euros is struck that will be cut today. The intraday technical indicators suggest the downside momentum has faded. The same is generally true for sterling–the second consecutive inside day. The October 3 range was about $1.2265 to $1.2410. Sterling is trading around $1.23 in late-morning turnover in London. There is an option for nearly GBP260 mln at $1.23 that expires today.

America

The Federal Reserve continues to demonstrate its resolve to ease the squeeze in the repo market while it contemplates a longer-term solution. At the end of last week, it pre-announced an extension of the overnight repo operations from through November 4. The previous announcement had extended them to October 10. These will be for a maximum of $75 bln. Several term (two-week) operations were also preannounced for a maximum of $45 bln. What makes these temporary operations, even if they are repeated, is that the repo operations are unwound (which is why the size of the operations cannot simply be added). There could be a permanent injection through QE or the purchases needed for the organic growth of the Fed’s balance sheet. But the problem is not so much the lack of excess reserves in the system. It is the piece of plumbing, if you will that allows the excess reverses to turn be used for repos.M If for several reasons, banks do not want to use their excess reserves in this way, the Fed can do so directly, as it has demonstrated through the repo operations.

The US reports the September monthly budget figures and consumer credit for August today. Investors are well aware of the growing US budget deficit, and although Modern Monetary Theory remains contentious, the fact of the matter is that the large US shortfall is not boosting rates or inflation. The US typically runs a monthly surplus in September, but the surplus last month is expected to be closer to $82 bln after last September’s $119 bln surplus. This will likely push the 12-month rolling average deficit beyond $80 bln. In September 2018, the average deficit was about $64 bln. Consumer credit jumped by $23.3 bln in July, spurred by a $10 bln surge in revolving credit (credit cards), the most in two years. The median forecast had expected only a $16 bln increase in July. Undeterred, the median forecast is for a $15 bln increase in August. Through July, the average increase this year has been about $16.1 bln compared with a $13.2 bln average in the first seven months of 2018.

The US dollar is holding above CAD1.33, which it broke above in the middle of last week. The Bank of Canada is one of the few major central banks that has resisted global move to lower rates. However, in the face of the prospect of more Fed cuts, many doubt that the Bank of Canada can hold out long. Initial resistance is seen in the CAD1.3330-CAD1.3340 area.The high set in early September was near CAD1.3380. The US dollar found support near MXN19.50 and is trading higher today. The MXN19.60 area offers the nearby cap, but if the risk-off mood deepens, the dollar can work its way toward MXM19.65-MXN19.70. The Dollar Index is trading within its recent ranges. Support is pegged near 98.70, and resistance is seen between 99.15 and 99.30.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,Brexit,China,Currency Movement,EUR/CHF,Featured,FX Daily,newsletter,Turkey,USD/CHF