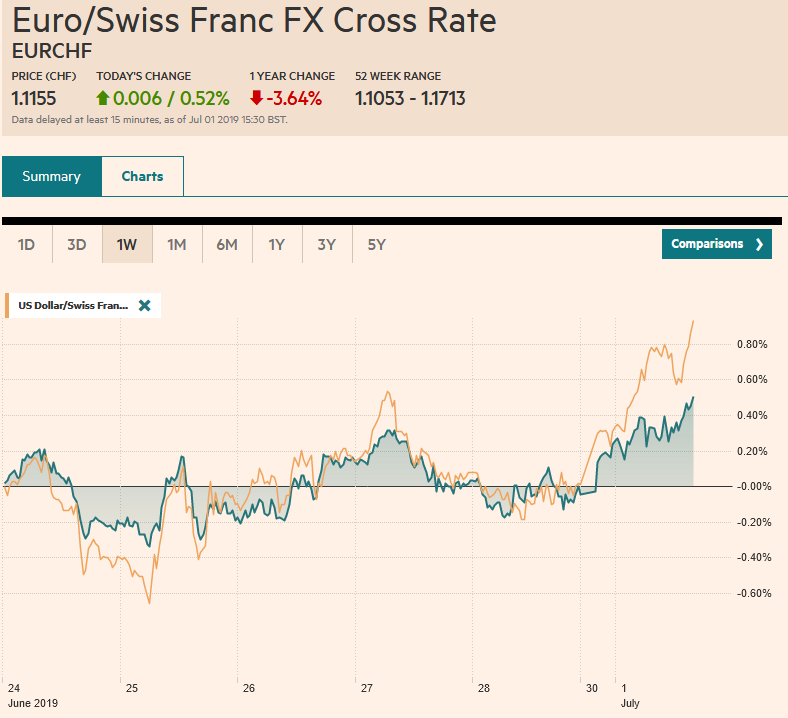

Swiss Franc The Euro has risen by 0.52% at 1.1155 EUR/CHF and USD/CHF, July 01(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: A new tariff truce between the US and China, coupled with the North Korean diplomacy and Russia-Saudi tentative agreement boosted investor confidence and sharp equity rallies. Japanese and Chinese equities rallied 2-3%. Most markets rallied in Asia-Pacific except for South Korea’s Kospi and Hong Kong markets were closed as the handover was commemorated. Europe’s Dow Jones Stoxx 600 was nearly 1% higher and at its best level in almost two months. The US S&P 500 is poised to gap higher to a new record high. Benchmark 10-year bond

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, China Caixin Manufacturing PMI, Eurozone Manufacturing PMI, Featured, FX Daily, Germany Manufacturing PMI, Germany Unemployment Rate, newsletter, trade, U.S. Manufacturing PMI, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.52% at 1.1155 |

EUR/CHF and USD/CHF, July 01(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A new tariff truce between the US and China, coupled with the North Korean diplomacy and Russia-Saudi tentative agreement boosted investor confidence and sharp equity rallies. Japanese and Chinese equities rallied 2-3%. Most markets rallied in Asia-Pacific except for South Korea’s Kospi and Hong Kong markets were closed as the handover was commemorated. Europe’s Dow Jones Stoxx 600 was nearly 1% higher and at its best level in almost two months. The US S&P 500 is poised to gap higher to a new record high. Benchmark 10-year bond yields are mostly firmer, as Asia Pacific bonds were dragged higher by pre-weekend upticks in US rates. European core bonds yields edged slightly higher despite disappointing manufacturing PMI readings, though the periphery, led by Italy has yields move lower. The dollar is firmer against all the majors and many emerging market currencies, though regional Asian currencies fared well. The Turkish lira was bolstered by Trump’s comments, claiming that Obama mistreated the Erdogan and may reconsider sanctions if Turkey goes forward to take delivery of Russian anti-aircraft system, which is due over the next week or two. Gold prices slid (~1.5%)on new trade hopes, while oil is rallying on OPEC+ restraint and hopes that the trade thaw may bolster demand. Separately, fewer shipments from Australia and strong steel output in China is lifting iron ore prices after the biggest quarterly rise in three years. |

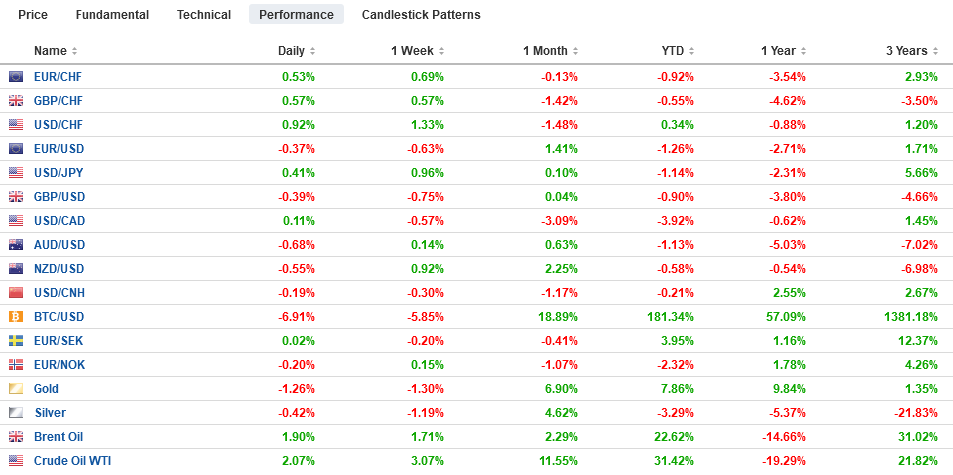

FX Performance, July 01 - Click to enlarge |

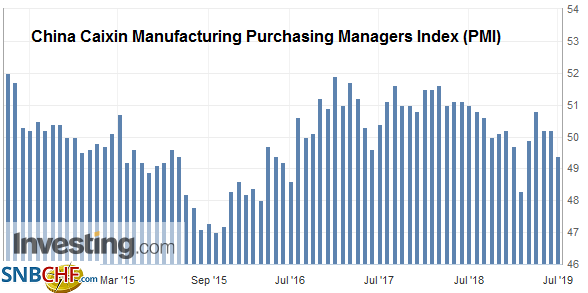

Asia PacificThe weekend optimism over the resumption of US-Chinese trade talks and Trump’s meeting with Kim in the DMZ has been checked by poor economic data. Japan’s Tankan survey and PMI manufacturing readings across the area, including Japan, China (Caixin), South Korea, and Australia (Australia Industry Group) fell. Separately South Korea reported its seventh consecutive decline in exports (June -13.5% after May’s -9.5%). Exports are one of the channels of contagion, and there appears no let up in sight. Japan’s export orders fell for the sixth month, while China’s official manufacturing PMI was unchanged 49.4 in June, new export orders slipped to 46.3 from 46.5, a fresh four-month low. China’s weakness is spilling over to impact employment. The official manufacturing PMI showed employment easing to 46.9 from 47.0, a ten-year low, while employment in non-manufacturing recorded a new three-year low (48.2 vs. 48.3). More stimulus from China is likely. Moreover, President Xi made more promises about market-opening measures and greater foreign access in a range of industries were announced, including oil, mining, and urban gas pipelines. A Japanese official noted that a supplemental budget could be forthcoming if to blunt the sales tax increase, which is still planned for October 1. Separately, tensions between South Korea and Japan are flaring up, and Japan will impose export restrictions on South Korea. |

China Caixin Manufacturing Purchasing Managers Index (PMI), Jun 2019(see more posts on China Caixin Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The dollar gapped higher against the Japanese yen. The bottom of the gap is the pre-weekend high near JPY107.95. The dollar found offers in both Tokyo and the European morning near JPY108.50, where a $933 mln option expires later today. We anticipate that the gap to be filled over the next day or two. The Tankan survey found a median expectation for the dollar to average JPY109.35 rather than JPY108.87 in the last survey. The dollar has averaged just around JPY107.70 in 2019 and just below JPY108 in Japan’s current fiscal year. The Australian dollar is posting a potential key reversal. It initially pushed higher in early turnover on the weekend news, but the disappointing (AiG) PMI and the broad weakness in the region PMIs took a toll despite higher iron ore prices. The Aussie is now trading below the pre-weekend low, and a close below there (~$0.7000) would confirm the single-day reversal pattern ahead of the RBA meeting on Tuesday which is widely expected to result in a rate cut. The initial retracement objective of the two-week rally is around $0.6960. The Chinese yuan strengthened for the third session. The dollar tested the recent low near CNY6.8350 after gapping lower. Nearby resistance is seen near CNY6.86, and support may extend to CNY6.80. The price action will strengthen the technical significance of the CNY7.0 cap.

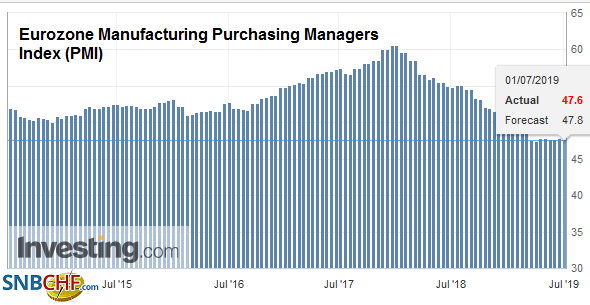

EuropeThe gain in the June eurozone PMI was revised away. Instead of creeping up to 47.8 from 47.7 in May, it fell to 47.6. |

Eurozone Manufacturing Purchasing Managers Index (PMI), Jun 2019(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

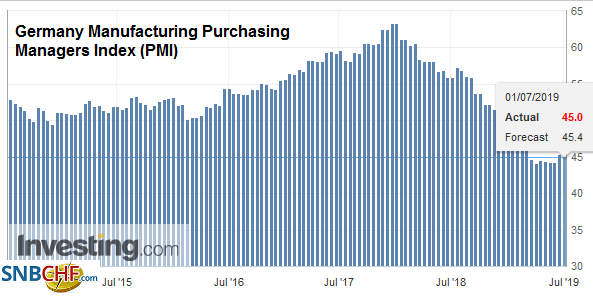

| That said, a mild recovery is still evident in the core. Germany’s manufacturing PMI is at a four-month high of 45.0 (44.3 in May) but not quite as good as the flash reading (45.4) suggested. France’s flash reading (52.0) was also revised down to 51.9 but is still an improvement over May (50.6). While these final readings are disappointing, Spain and Italy’s reports were more so. Spain’s manufacturing PMI slumped to 47.9 from 50.1, while Italy’s dropped to 48.4 from 49.7. Both were worse than expected. Perhaps taking some of the sting from Italy’s dismal report was new that unemployment in May slipped below 10% for the first time in seven years. |

Germany Manufacturing Purchasing Managers Index (PMI), Jun 2019(see more posts on Germany Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The report to pressure on the ECB to provide more stimulus coming months before Drahgi’s term ends in October. There is some thought it could come as early as the meeting later this month when under the rotating voting system, the Bundesbank’s Weidmann does not vote. That said, the informal process still is said to dominate the required procedures, and the market is pricing in about a one-in-three chance fo a cut this month. There are two other issues to note. First, on the sidelines of the G20 meeting, the EU and Mercosur (Argentina, Brazil, Paraguay, and Uruguay) finally (20 years?) struck a free-trade accord. Second, the EU is working towards an agreement on the top posts. The Netherland’s Timmermans seems to now be the leading candidate to succeed Juncker, though Poland and Hungary are opposed. A decision on Draghi’s replacement is yet to be decided, but the odds, which we never assessed to be particularly high, of Weidmann seems to have diminished, while the chances of a woman (Lagarde?) appears to be increasing.

While the Tory leadership challenge and Brexit are the main talking points in the UK, it reported a string of poor data today. The manufacturing PMI weakened further rather than stabilize as many economists expected. It fell to 48.0 from 49.4, a six-year low. Separately, the UK reported slower lending to consumers and mortgages and weaker money supply growth. |

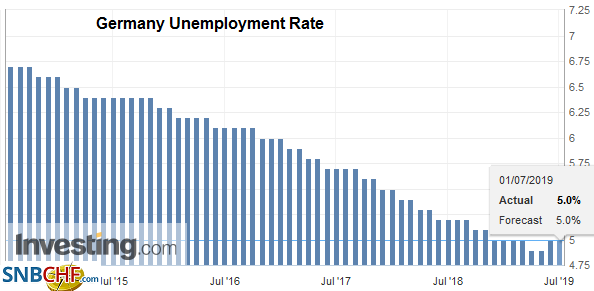

Germany Unemployment Rate, Jun 2019(see more posts on Germany Unemployment Rate, ) Source: investing.com - Click to enlarge |

| The euro has been sold through last week’s low (~$1.1355) and is trading around the (38.2%) retracement of the rally since June 18 (from ~$1.1180). The next retracement objective, psychological support, and the 20-day moving average are near $1.1300. There is a roughly 640 mln euro option struck at $1.1300 that will be cut today and nearly a billion euro option that will also expire at $1.1320 today. Resistance is now pegged around $1.1350. Sterling is testing the 50% retracement of the same rally from June 18 near $1.2640. There is an option for about GBP205 mln by $1.2615 that expires in front of $1.2600 support. |

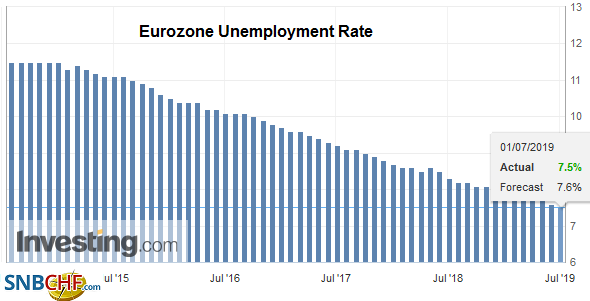

Eurozone Unemployment Rate, June 2019(see more posts on Eurozone Unemployment Rate, ) Source: investing.com - Click to enlarge |

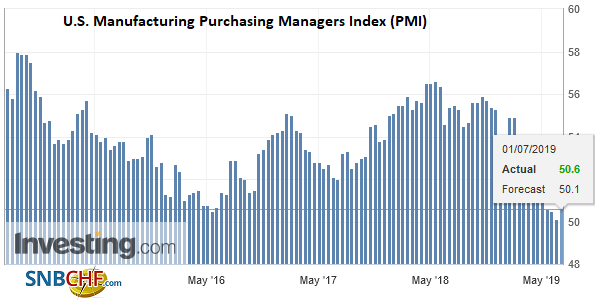

AmericaThe US reports the manufacturing ISM and PMI and construction spending today, but the highlight this week is the jobs report at the end of the week. The Fed’s Vice Chairman Clarida will speak about monetary policy in the North American afternoon. Canada has a light calendar today, while Mexico reports IMEF manufacturing and non-manufacturing indices and both were below the 50 boom/bust level in May. We suspected that the pendulum of market sentiment had reached a peak of dovishness toward the Fed last week. The new tariff truce between the US and China has made others come around to this view. However, we are skeptical that the resumption of trade talks does much for gaming out the Fed’s options. The current level of tariffs remains in place. The downside (of more tariffs) have been reduced, for the time being, but the Trump Administration’s trade policy is not the best anchor of monetary policy. Europe’s unveiling of payments system that will allow some trading with Iran (food and medicine to begin) will not sit well with the US government with whom trade talks have started, for example. Moreover, the tariff battle with China could resume shortly as the May tweets illustrated. The US dollar recovered from CAD1.3060 to close near session highs ahead of the weekend. It has made a little more headway today. We look for CAD1.3125-CAD1.3150 to be tested. The Mexican peso is firm but is not showing any inclination to test last week’s high (USD low near MXN19.09). The broad consolidation looks set to continue. The Dollar Index has near-term potential toward 96.80, near where a retracement objective and the 20-day moving average are found. |

U.S. Manufacturing Purchasing Managers Index (PMI), Jun 2019(see more posts on Jun 2019, U.S. Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,China Caixin Manufacturing PMI,Eurozone Manufacturing PMI,Featured,FX Daily,Germany Manufacturing PMI,Germany Unemployment Rate,newsletter,Trade,U.S. Manufacturing PMI