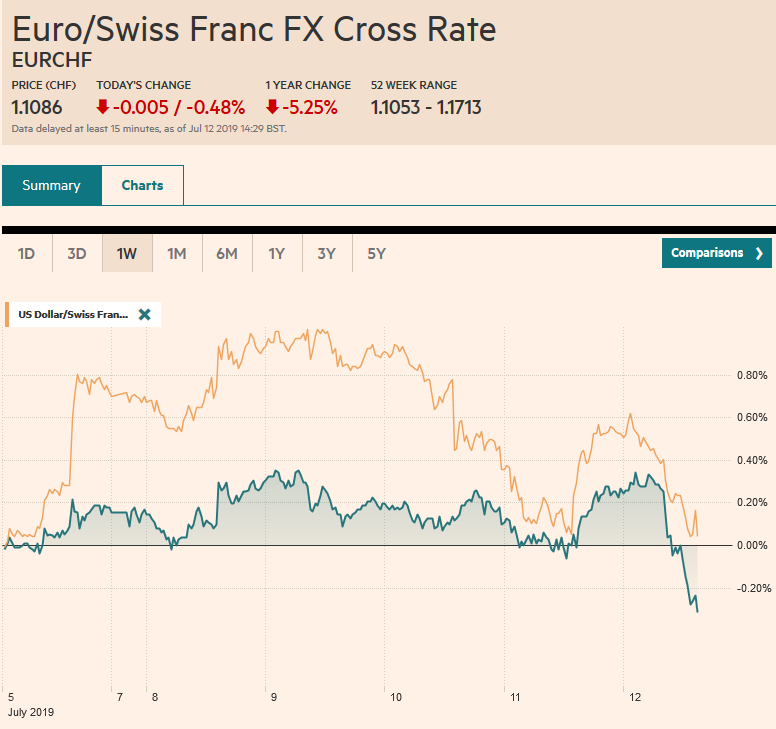

Swiss Franc The Euro has fallen by 0.48% at 1.1086 EUR/CHF and USD/CHF, July 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Higher than expected US CPI and the second tepid reception to a US bond auction this week pushed US yields higher and helped stall the equity momentum. Asia Pacific yields, especially in Australia and New Zealand jumped 8-10 bp in response, and Spanish and Portuguese bonds bore the burden in Europe. Barring a sharp decline today, the US 10-year yield is higher for the second consecutive week, something not seen in three months. Equities are mostly firmer, but small gains were not enough to prevent the MSCI Asia Pacific Index from

Topics:

Marc Chandler considers the following as important: 4) FX Trends, China, EUR/CHF, Featured, FX Daily, newsletter, Singapore, Turkey, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.48% at 1.1086 |

EUR/CHF and USD/CHF, July 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Higher than expected US CPI and the second tepid reception to a US bond auction this week pushed US yields higher and helped stall the equity momentum. Asia Pacific yields, especially in Australia and New Zealand jumped 8-10 bp in response, and Spanish and Portuguese bonds bore the burden in Europe. Barring a sharp decline today, the US 10-year yield is higher for the second consecutive week, something not seen in three months. Equities are mostly firmer, but small gains were not enough to prevent the MSCI Asia Pacific Index from snapping a five-week rally. Europe’s Dow Jones Stoxx 600 is trying to end a six-day slide, but the five-week rally appears to be over. US shares are firmed and are set to probe new record highs. The dollar continues to trade with a heavier bias against the major currencies on the day and the week. |

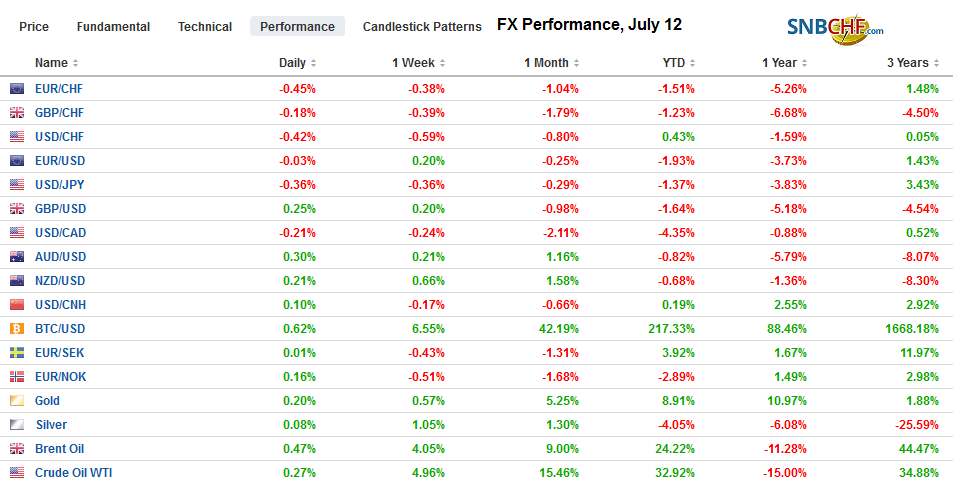

FX Performance, July 12 - Click to enlarge |

Asia PacificChina reported a 1.3% decline in exports in June, which were in line with expectations, and a 7.3% drop in imports, which were more than expected (~-4.8%). This generated a nearly $51 bl surplus, 20% wider than May. It is the largest monthly surplus in the first half. China’s surplus averaged a little more than $30 bln over the past six months compared with about $22.5 bln in H1 18. The bilateral flows with the US are instructive. Imports from the US have fallen by almost a third (31.4%) from a year ago while exports are off 7.8%. China’s bilateral surplus with the US rose to $30 bln, the widest this year. President Trump complained yesterday that China has not stepped up their purchases of US agriculture goods, but the US has not yet granted licenses to US companies to sell Huawei product and it had seemed the two actions were linked. Separately, China reported a surge in lending in June. Aggregate financing jumped to CNY2.26 trillion from CNY1.395 trillion in May. It rose considerably faster than bank lending (CNY1.66 trillion from CNY1.18 trillion). The difference is often associated with shadow banking, which in China is not simply nonbank financial institutions, but parts of some banks, as well. Expectations that the PBOC will ease policy are gaining momentum, especially given the signals this week by the Fed and ECB. |

China Trade Balance (USD), June 2019(see more posts on China Trade Balance, ) Source: investing.com - Click to enlarge |

Singapore, a regional entrepot, reported an unexpected and sharp contraction in Q2 GDP, which likely reflects the trade disruption. Output fell 3.4% quarter-over-quarter, nearly offsetting in full the 3.8% expansion in Q1. Economists had forecast a small gain. Exports were a major drag, but the domestic economy also softened as hinted at by the 2.2% decline in May retail sales reported separately.

South Korea and Japanese officials met today to begin trying to resolve their dispute. The US has offered to host high-level talks. Japan is arguing that South Korea has improperly shipped some semiconductor fabrication material to North Korea.

The dollar’s recovery from sub-JPY108 yesterday continued into Asia today where the greenback reached JPY108.60. It recorded the session low, so far, in early Europe near JPY108.20. We anticipate a consolidative North American session and the expiring option (~$565 mln) at JPY108 and the (~$660 mln) at JPY108.50 may large denote the range. Last week, the dollar closed a little below JPY108.50. The Australian dollar is rising for the third session and briefly pushed through $0.7000 for the first time this week. It finished last near $0.6980 last week. The Thai baht has come under pressure following stepped up efforts by the central bank to curb its gains. Over the past three months, the baht had risen by nearly four percent before shedding about 0.8% today.

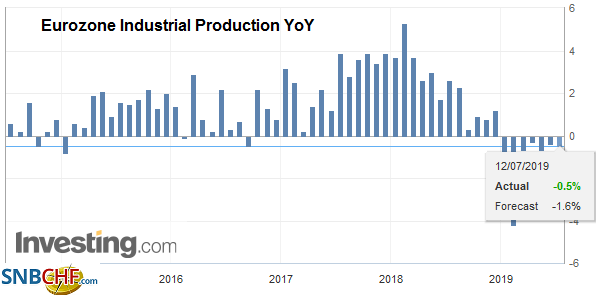

EuropeThe eurozone reported the sharpest rise in industrial production since January. May’s 0.9% increase offsets the 0.4% decline in April and the 0.3% drop in March. The median forecast in the Bloomberg survey was for a 0.2% gain. This is another example of the real data outperforming survey data. The eurozone appears to be recovering from the soft patch, but Daimler’s warning and its reduced outlook suggest that the headwinds have been completely worked through yet. |

Eurozone Industrial Production YoY, May 2019(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

Turkey reportedly begins taking shipment of the Russian-built missile defense system today. The US has threatened sanctions but recently appears to have softened its line. Nevertheless, reports suggest that the US has begun winding down Turkey’s role in producing the F-35 fighter jets. The Turkish lira is the weakest of the emerging market currencies this week and did not fully recover from the sell-off sparked by the dismissal of the central bank governor. The dollar finished last week near TRY5.6280 and is now near TRY5.7100. The central bank meets on July 25 and is widely expected to cut the 24% one-week repo by 100 bp or more.

The euro is trading inside yesterday’s range, and quiet activity is likely to continue in the North Ameican session. There is a 1.1 bln euro option at $1.1250 that will but cut today and one for a little more than half of it at $1.1270, with another 1.1 bln euro option at $1.13. Since closing near $1.1250 in the middle of the week, the euro has hardly moved. It closed near $1.1225 last week. Today is the first time since Monday that sterling has held above $1.25. It has been confined to less than a third of a cent range today. A nearly GBP600 mln option at $1.2580 that will expire today is a little above this week’s highs. Sterling is set to extend its losing streak against the euro to what appears to be a record 10 weeks (using synthetic data going back to 1980)

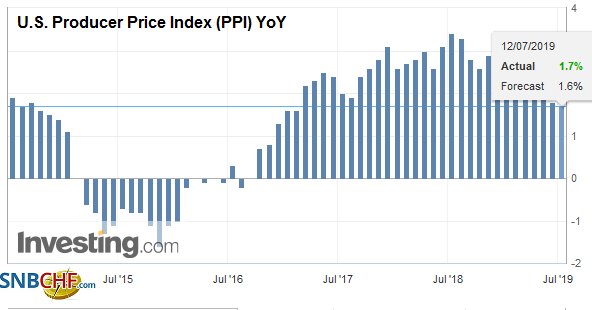

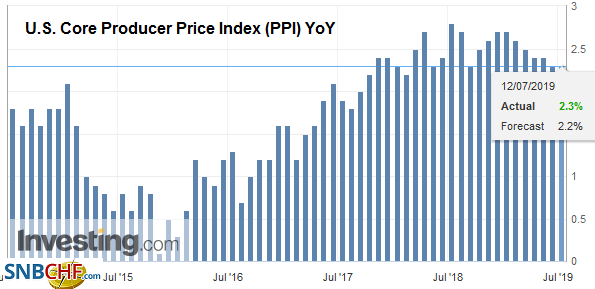

AmericaSeveral weeks ago, Powell argued that some of the downward pressure on prices was temporary. At his testimony on Wednesday has backtracked, suggesting that weak price pressures could be more persistent. Yesterday the US reported a 0.3% increase in the core CPI, the largest rise since January 2018, and lifted the year-over-year rate to 2.1%. The headline remained at 1.6%. Maybe Powell was right before he was wrong. Measured inflation is not dead. When everything has been said and done, the implied yield of the January 2020 fed funds futures contract eased 1.5 bp this week. The implied yield of 1.76% compares with the current effective average rate of 2.41% and 1.555% low seen on June 20. |

U.S. Producer Price Index (PPI) YoY, June 2019(see more posts on U.S. Producer Price Index, ) Source: investing.com - Click to enlarge |

| The North American calendar is light. The US reports June producer prices, which typically are not as volatile as consumer prices. However, like the CPI, the core rate, which excludes food and energy, is expected to be firmer than the headline. The headline rate is forecast to be flat, which would translate into a 1.6% pace, while the core may rise 0.2%, generating a 2.1% year-over-year rate. Chicago Fed President Evans is the last Fed officials to speak this week, and he is seen on-board with a 25 bp rate cut later this month. Canada’s diary is empty, while Mexico reports May industrial production figures. A small decline is expected after the 1.5% surge in April. |

U.S. Core Producer Price Index (PPI) YoY, June 2019(see more posts on U.S. Core Producer Price Index, ) Source: investing.com - Click to enlarge |

The US dollar is trading at its lowest level since last October against the Canadian dollar and is approaching psychological support at CAD1.30. However, the intraday technicals are turned up in Europe, and there may be a test on the CAD1.3050 area, which holds a $1 bln option that will be cut today. It is the fourth consecutive week the US dollar has fallen against the Canadian dollar, its longest losing streak since January. The dollar continued to unwind the gains scored against the Mexican peso that was sparked by the unexpected resignation of the finance minister. The dollar punched above MXN19.35 in the immediate response and today returned to almost MXN19.05, which corresponds to a (61.8%) retracement of the earlier surge.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,China,EUR/CHF,Featured,FX Daily,newsletter,Singapore,Turkey,USD/CHF