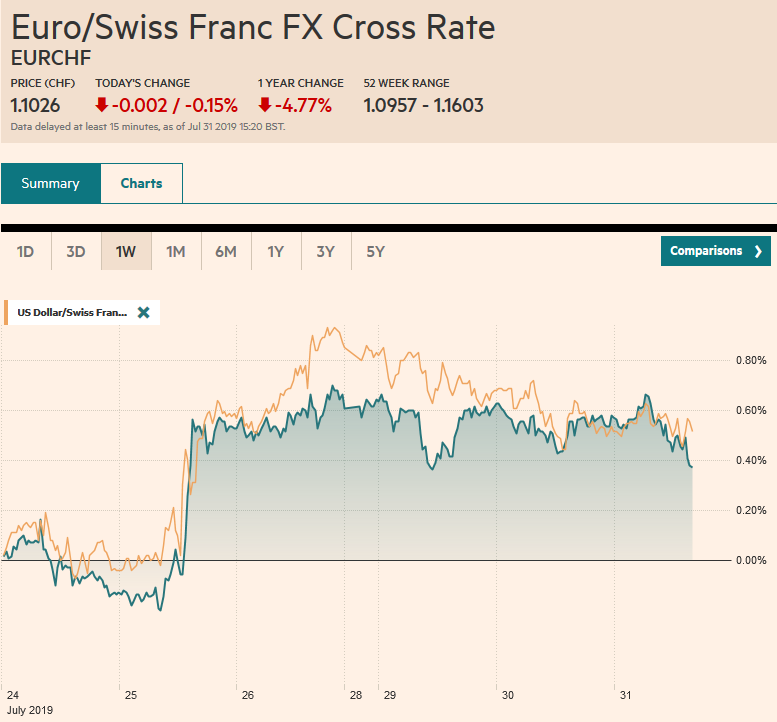

Swiss Franc The Euro has fallen by 0.15% to 1.1026 EUR/CHF and USD/CHF, July 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: After a shellacking in recent days, sterling has stabilized though there is not much of a bounce to speak of, suggesting the adjustment to the risk of a no-deal Brexit may not be complete. After the S&P 500 posted back-to-back declines, Asia Pacific equities struggled. Hong Kong shares led the regional decline. European stocks are little changed after the Dow Jones Stoxx lost nearly 1.6% yesterday, its largest loss in two months. The bank share index dropped 3% yesterday, the most in four months, but has steadied today. US shares are

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, brl, China, China Manufacturing PMI, Currency Movements, EMU, Eurozone Consumer Price Index, Eurozone Gross Domestic Product, Eurozone Unemployment Rate, Featured, Germany Retail Sales, Germany Unemployment Rate, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.15% to 1.1026 |

EUR/CHF and USD/CHF, July 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: After a shellacking in recent days, sterling has stabilized though there is not much of a bounce to speak of, suggesting the adjustment to the risk of a no-deal Brexit may not be complete. After the S&P 500 posted back-to-back declines, Asia Pacific equities struggled. Hong Kong shares led the regional decline. European stocks are little changed after the Dow Jones Stoxx lost nearly 1.6% yesterday, its largest loss in two months. The bank share index dropped 3% yesterday, the most in four months, but has steadied today. US shares are trading with a slightly firmer bias in the European morning. Benchmark 10-year yields are mostly a little softer. The US dollar is narrowly mixed, with the Australian dollar is recovering some of the ground lost yesterday. Most of the other majors are in narrow ranges. Among the emerging market currencies, the Turkish lira continues to edge higher. Brazil is widely expected to deliver a 25 bp cut in the Selic rate (to 6.25%) a few hours after the FOMC’s first anticipated rate cut in over a decade. |

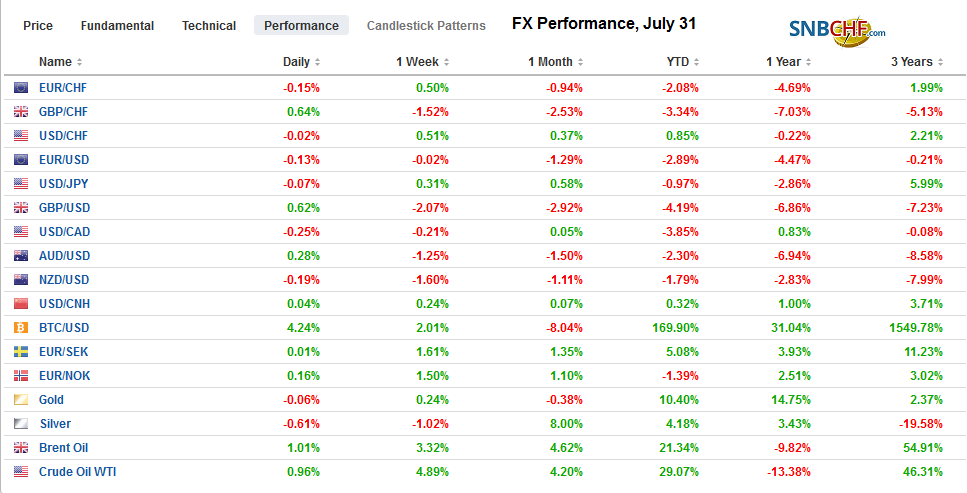

FX Performance, July 31 - Click to enlarge |

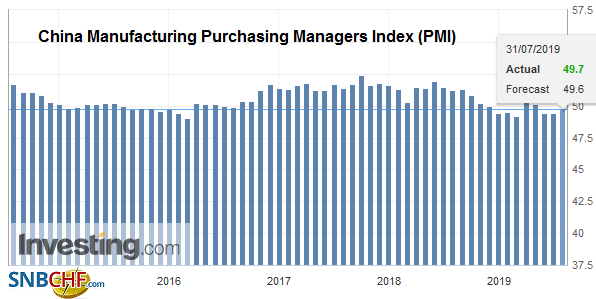

Asia PacificThe resumption of US-China trade talks in Shanghai ended without a statement. Little progress was expected, and it appears little delivered. US President Trump’s claimed that China “just doesn’t come through” and that it may be waiting for after the 2020 US election, seemed to underscore America’s frustration. Trump is complaining that China has not stepped up its purchases of US agriculture while Chinese officials seemed to have seen it as a quid pro quo for granting licenses to US companies to sell to Huawei. China reported the July PMI. The manufacturing component edged up to 49.7 from 49.4. It was the third consecutive reading below the 50 boom/bust level. The non-manufacturing component slipped to 537 from 54.2. The composite nudged up to 53.1 from 53.0. The Caixin version, which focuses more on small and medium-sized businesses, will be released tomorrow. |

China Manufacturing Purchasing Managers Index (PMI), July 2019(see more posts on China Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Australia’s Q2 CPI firmed. Consumer inflation rose 0.6% quarter-over-quarter for a 1.6% year-over-year increase. It was slightly firmer than economists forecast and follows a flat Q1 (and 1.3% year-over-year.). Separately, Australia reported a little softer than expected private credit growth in June (3.3% vs. 3.5%). The net impact of the reports is to reduce the odds of a follow-up rate cut after the back-to-back moves in June and July. There was never a good chance of an August move, but the odds of a September move have fallen back below 50%. The odds of a move in October have narrowed but remains above 50%.

The dollar-yen exchange rate has been confined to about 15 ticks through the European morning (JPY108.50-JPY108.65). The dollar has not traded below JPY108.40 so far this week, and the JPY109.00 technical cap of some significance remains in place. The Australian dollar initially made a new low a little below $0.6865 before rebounding toward $0.6900. It is trying to snap an eight-day slide. The intraday technical readings favor another push higher in North America. There seemed to be little market reaction to another short-run ballistic missile test by North Korea that may be protesting an upcoming US-South Korea military drill. The US is encouraging South Korea and Japan to reach a standstill agreement while negotiators can try to resolve the issue. However, Japan is expected to remove South Korea from its preferred trading partners list ahead of the weekend, which will broaden the economic impact of its actions. The Chinese yuan firmed slightly for the second day after easing for the previous three sessions.

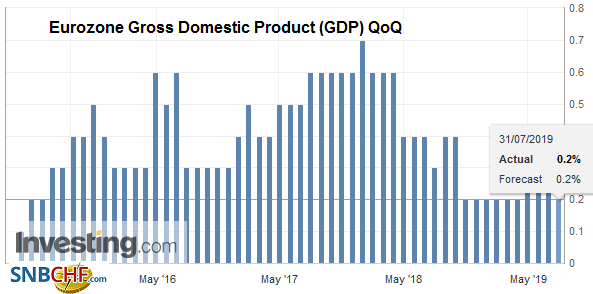

EuropeGrowth slowed to 0.2% in the eurozone in Q2 from 0.4% in Q1. This was in line with forecasts. |

Eurozone Gross Domestic Product (GDP) QoQ, Q2 2019(see more posts on Eurozone Gross Domestic Product, ) Source: investing.com - Click to enlarge |

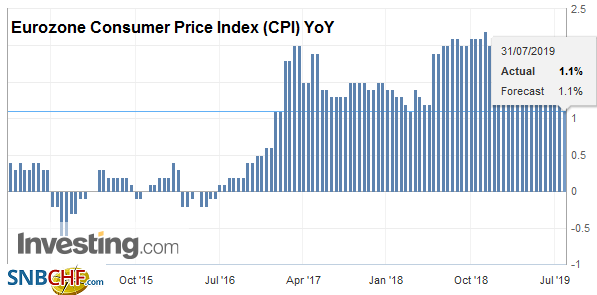

| The preliminary July CPI eased to 1.1% from 1.3%. This, too, had been anticipated. The surprise was that the core rate slipped more than expected (0.9% from 1.1%). However, the impact on the market was minimal. The ECB is widely expected to provide more stimulus in September, and today’s data will not change the dynamics or calculations. |

Eurozone Consumer Price Index (CPI) YoY, July 2019(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| UK Prime Minister Johnson is in Northern Ireland today. Tomorrow is the byelection in the Wales district of Brecon Radnorshire. The seat was held by a Tory, but now the Lib-Dems are favored to win it. This will reduce Johnson’s working majority to one MP. This may not mean much in August, but come September 3 when Parliament reconvenes, Johnson will likely face a confidence vote.

Ironically, Europe seems poised to rebuff one of the few multilateral initiatives of the Trump Administration. German finance minister Scholz, who rejected calls for Europe’s largest economy that can borrow for 10-years at negative yields or 30-year for a new record low of 16 bp to boost government spending, is skeptical about Germany joining the proposed military mission in the Straits of Hormuz to protect oil tankers. |

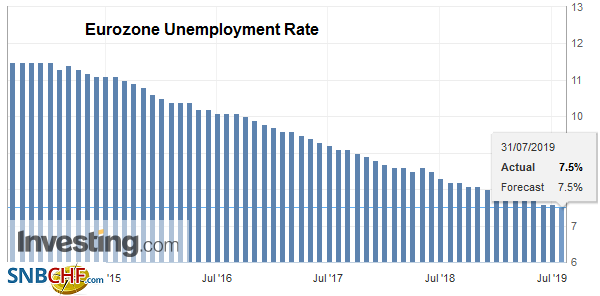

Eurozone Unemployment Rate, June 2019(see more posts on Eurozone Unemployment Rate, ) Source: investing.com - Click to enlarge |

| Following up his large rate cut last week, Turkey’s central bank governor cut this year’s inflation forecast to 13.9% from 14.6% while keeping next year’s forecast of 8.2% unchanged. This is seen allowing additional rate cuts. The lira is near four-month highs today and is rising for the sixth consecutive session. We suspect the move is getting overdone. Next week, less favorable news is likely. The CPI, which stood at 15.72% in June, likely rose in July. The median forecast in the Bloomberg survey is for an increase to 16.93%. Last July prices rose only 0.55%. Economists forecast a 1.6% rise in the CPI this month. |

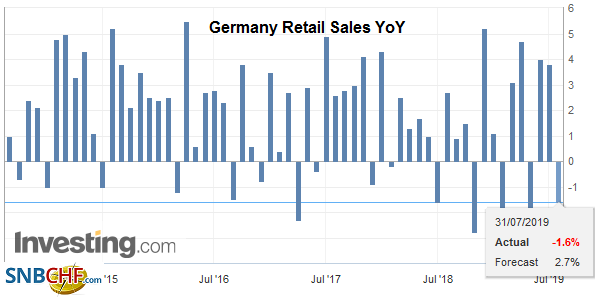

Germany Retail Sales YoY, June 2019(see more posts on Germany Retail Sales, ) Source: investing.com - Click to enlarge |

| The euro firmed to a new four-day high in late Asian turnover and poked briefly through $1.1160. However, the market shows little enthusiasm and the euro remains within the range seen last week when the ECB met (~$1.1100-$1.1190). There is a chunky 1.4 bln euro option struck at $1.1145 that expires today. The intraday technicals warn of the risk of additional short-covering in the North American morning. Sterling’s downside momentum has stalled but buying interest is minimal, and it is stuck in a 20-pip range on either side of $1.2160. The euro is trading a little heavier against sterling, and the four-day streak could end. |

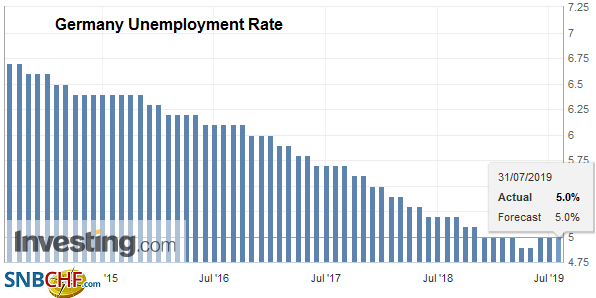

Germany Unemployment Rate, July 2019(see more posts on Germany Unemployment Rate, ) Source: investing.com - Click to enlarge |

America

It is Fed day, and the market has settled with about 79% chance of a quarter-point cut discounted and the remainder sees a 50 bp move likely, according to the CME’s model. More than one journalist has posited a shift in the coefficient of variables in the Fed’s decision-making equation and see global variables (or specifically, the interest rates spread between the US and Europe), and claim a new era is at hand. Meh, One does not need to propose a new paradigm. International uncertainties were included in the cross-currents that Chairman Powell and other Fed officials have cited. In his recent congressional testimony, Powell acknowledged that the relationship between unemployment and inflation had broken down and that this meant that monetary policy setting was tighter than may be appropriate. The case for easing is based primarily on domestic economic variables.

A majority of the FOMC argues that because inflation is below target, a low-cost insurance policy to extend the recovery in the face of a number of uncertainties is appropriate. Some suspect that Greenspan and Yellen’s recent endorsement of a rate cut was choreographed by the Fed, and it may have been, but for some strange reason, former NY Fed President Dudley did not get the call. He wrote an op-ed piece for Bloomberg yesterday in which he sounded more skeptical of the need and suggested that the Fed could be “one and done.”

It may sound cheeky to say this about the first Fed cut in a decade, but it may not be the biggest driver of the price action. It is largely assumed, as we noted. What may catch some unaware is that the Fed is also likely to stop its experiment in unwinding its balance sheet. It aimed to stop at the end of next month, but it would seem contradictory to continue to do so as the Fed reduces interest rates. We suspect that there will be at least one dissent favoring stand pat policy. Two dissents would get some notice, and three (unlikely) would be a blow. However, most important is how the market interprets the forward guidance. Given what seems to be the Fed’s view, and what we suspect will be the broad evolution of the economy, another rate cut toward the end of the year may remain the most likely scenario. We expect Powell to leave the door open but revert back to data-dependency to see if the risks are materializing or dissipating.

Before the FOMC announcement and Powell’s press conference, the economic calendar is chock full. The highlight for the US is the ADP job estimate (~150k) that may influence expectations for Friday’s national report. Outside of FOMC days, the non-farm payroll report often sees the greater market reaction of the US data. The Employment Cost Index (0.7% Q2, the same as Q1) is more important for economists that market participants. The Chicago PMI, which often tracks the national ISM, is seen rebounding back above 50. Canada reports May GDP, and Mexico reports Q2 GDP. Growth in Canada may have ratcheted down to 0.1% in May from a 0.3% expansion in April. This will reduce the year-over-year pace to 1.3% from 1.5%. Mexico is expected to report the second consecutive quarterly decline. It may be sufficient to push the year-over-year rate into contraction for the first time since 2009. Given Turkey’s recent aggressive rate cut, Mexico has the dubious honor of having the highest real rates after war-torn Ukraine.

The US dollar’s pullback after testing CAD1.32 may stall near CAD1.3130, a (38.2%) retracement of the leg up from the year’s low on July 19 (~CAD1.3015). If this yields, the next target is CAD1.3080-CAD1.3100. The dollar is continuing to coil against the Mexican peso. The technical indicators have been neutered by this prolonged sideways activity, which serves the carry-plays well. The dollar is testing resistance against the Brazilian real near BRL3.80. Note that the five-day moving average crossed above the 20-day moving average on Monday for the first time since late-May. The real had strengthened nearly 10% since then. The correction appears to have begun. The first target is the BRL3.85-BRL3.87 area. The Dollar Index is firm near yesterday’s high (~98.20), and the technical indicators look stretched.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,brl,China,China Manufacturing PMI,Currency Movements,EMU,Eurozone Consumer Price Index,Eurozone Gross Domestic Product,Eurozone Unemployment Rate,Featured,Germany Retail Sales,Germany Unemployment Rate,newsletter