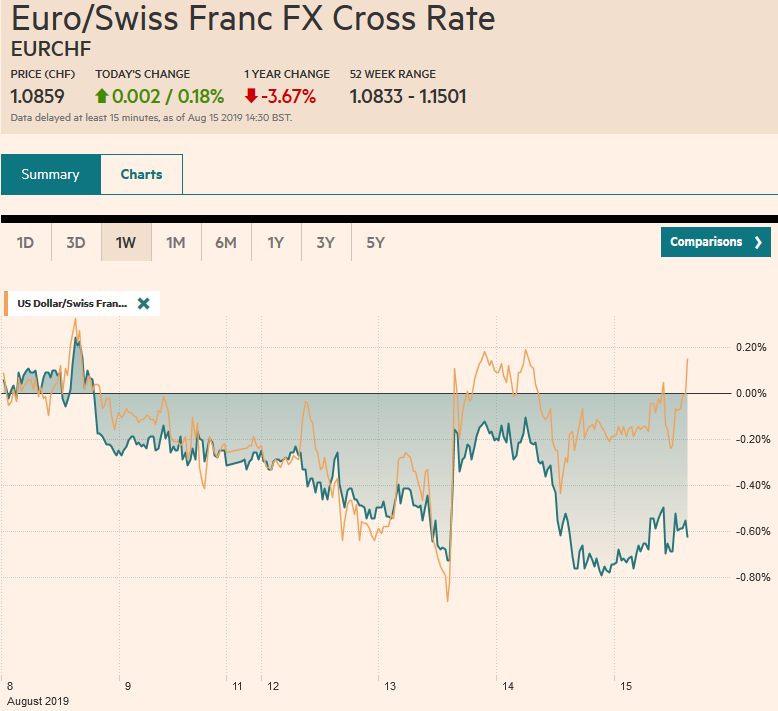

Swiss Franc The Euro has risen by 0.18% to 1.0859 EUR/CHF and USD/CHF, August 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: It took some time for investors to recognize that the scaling back of US tariff plans was not part of a de-escalation agreement. There was an explicit acknowledgment by US Commerce Secretary Ross that there was no quid pro quo. The US tariff split was more about the US than an overture to China. In fact, as China did in September when the US sanctioned it for buying weapons from Russia, this week it refused a request from the US for a port call in Hong Kong. This, coupled with a string of disappointing economic data China and Germany, saw a bullish flattening of yield curves and

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, China House Prices, Currency Movements, Featured, newsletter, U.K. Core Retail Sales, U.K. Retail Sales, USD, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.18% to 1.0859 |

EUR/CHF and USD/CHF, August 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: It took some time for investors to recognize that the scaling back of US tariff plans was not part of a de-escalation agreement. There was an explicit acknowledgment by US Commerce Secretary Ross that there was no quid pro quo. The US tariff split was more about the US than an overture to China. In fact, as China did in September when the US sanctioned it for buying weapons from Russia, this week it refused a request from the US for a port call in Hong Kong. This, coupled with a string of disappointing economic data China and Germany, saw a bullish flattening of yield curves and mored inversions. The US 2-10 inverted but is flat now and the 30-year yield, which dipped below 2% in Asia is back above, albeit slightly. France and Germany have the largest 2-10 year inversions (40 bp+ and 23 bp respectively. Canada’s inversion is around 15 bp. 30-year bond yields are negative in Switzerland, Germany, and the Netherlands. Finland may be next with a 30-year yield of about four basis points. Asia yields played catch-up earlier today, while European yields have steadied and are firmer. There is roughly $15 trillion in negative-yielding bonds globally, including more than $1 trillion of corporate paper. Equity markets are still struggling. In Asia, the Nikkei fell to six-month lows and is now lower on the year, but it was Australia that took the brunt with its main index falling 2.8%. A stronger than expected jobs report may mean that another interest rate cut may not be around the corner. Shares advanced in China, Hong Kong, India, and South Korea. European stocks are little changed, stuck in yesterday’s trough, while US shares are trading firmer, with the S&P 500 called higher after yesterday’s nearly 3% plunge. The dollar is seeing some of yesterday’s gains pared, except Swiss franc and yen. Among the emerging market currencies, the liquid and freely accessible currencies (e.g., South Africa, Turkey, Mexico) are firmer. |

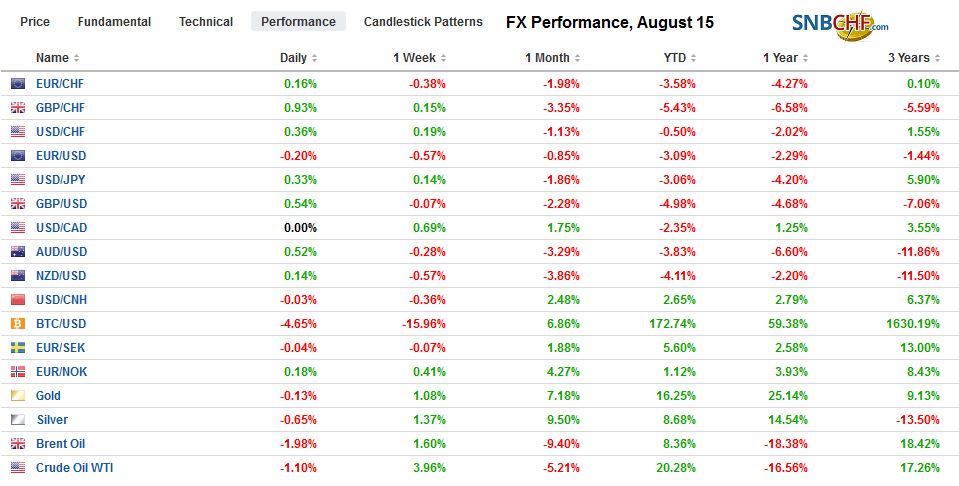

FX Performance, August 15 - Click to enlarge |

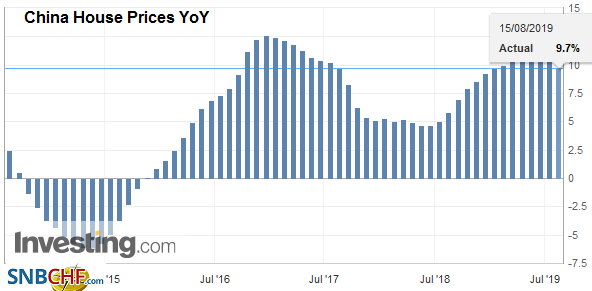

Asia PacificThe PBOC set the dollar reference rate at CNY7.0268. This was slightly stronger for the dollar than had been anticipated by the median forecast in the Bloomberg survey. But, the important signal today was that the fix was lower than the previous day’s fix (CNY7.0312), suggesting some easing of pressure. Separately, the PBOC injected CNY400 bln through its medium-term lending facility (MLF) to offset the amount expiring from a previous operation. China protested the 10% tariff the US intends on more than $100 bln of Chinese goods and said it violated the agreement between Xi and Trump. |

China House Prices YoY, July 2019(see more posts on China House Prices, ) Source: investing.com - Click to enlarge |

Australia created 41.1k jobs last month, well above the 14k that the median forecast in the Bloomberg survey anticipated. Of these jobs, 34.5 were full-time positions, which is the second-highest this year. The unemployment rate was steady at 5.2%, while the participation rate ticked up to 66.1% from 66.0%. The jobs report, coupled with the rise in consumer inflation expectations to 3.5% in August from 3.2% in July, saw participants scale back expectations of a rate cut next month. The market halved the chances of a move at the September 3 meeting to around 21%.

Under its “yield curve control” policy, the Bank of Japan targets the 10-year yield in a range of +/- 20 bp around zero. The yield is lower than -20 bp for the fifth consecutive session today. It leaves the BOJ in a tough place with limited options, especially if doesn’t want to take the risk of confusing the market by stopping purchases long-dated bonds, for example. The BOJ could work the other end of the curve by pushing the deposit rate deeper into negative territory. At minus 10 bp, it is the least negative of countries that have gone down this route. The market is pricing in almost a 1-in-4 chance of a small cut in the deposit rate, with a better than 50% chance of such a move at the end of October.

The dollar has mostly been confined to yesterday’s range against the yen and remains within the broad range seen on Tuesday (~JPY105-JPY107). The greenback is near the middle of that range in late European morning turnover. There is a $430 mln option at JPY107 and $450 mln at JPY105.75 that expire today. The Australian dollar is firmer but also is within yesterday’s range. It is stuck in a little more than a half-cent range (~$0.6745-$0.6800) that has dominated this week’s activity. The Aussie has come off from its Asian high in Europe but may find support near $0.6760.

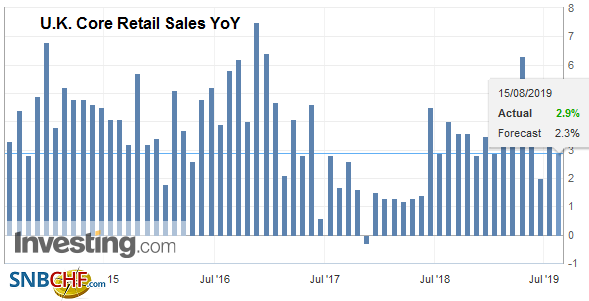

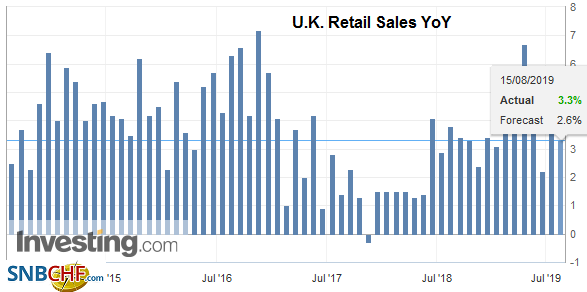

EuropeUK consumers continued to defy economists forecasts that they going to hibernate. Nearly every month this year, the retail sales report has come in above expectations. July was no exception. |

U.K. Core Retail Sales YoY, July 2019(see more posts on U.K. Core Retail Sales, ) Source: investing.com - Click to enlarge |

| Economists forecast a 0.2% decline in both the headline and exclude petrol. Instead, both measures rose by 0.2% while the June series was revised slightly lower to 0.9% at the headline (from 1.0%) and excluding petrol to 0.8% (from 0.9%). |

U.K. Retail Sales YoY, July 2019(see more posts on U.K. Retail Sales, ) Source: investing.com - Click to enlarge |

A Tory backbencher has warned that UK Prime Minister Johnson may try to pull the UK out of the EU within the next week and a half, before the G7 summit on August 24. It is difficult to evaluate such claims, but it does not ring true. The markets do not seem to believe it. Sterling is edging higher against the euro for a fourth consecutive session. It is the longest such streak in three months and barring a reversal tomorrow, sterling’s record-long 14-week slide against the euro will end.

Norway’s central bank, Norges Bank, was one of the few central banks in a tightening mode. It did not change its stance much today, but the small nuance in the statement referring to global uncertainty places the hike that was anticipated for the next meeting (Sept 19) in doubt. The euro has rallied nearly 5.25% against the krone since the late July low near NOK9.60. It has found support this week near NOK9.90 and is now back above NOK10.0, having been as high as nearly NOK10.05.

The euro has been confined to a fifth of a cent range today (~$1.1135-$1.1155). There is a nearly 720 mln euro option at $1.1150 that expires today. The market appears to be waiting for North American leadership, but the bias is to sell into rallies. There is more speculation that Germany, which has contracted in two of the past four quarters, may shrink again in Q3. The flash August PMI will be reported next week. Sterling is firm at the upper end of its $1.20-$1.21 range that has trapped prices this week. A close above $1.21 may help lift the tone and force some weak shorts to cover, but it may take a move through $1.2210, the high for the first half of the month, to be anything significant from a technical perspective. The intraday technicals are stretched, following the positive reaction to the retail sales figures.

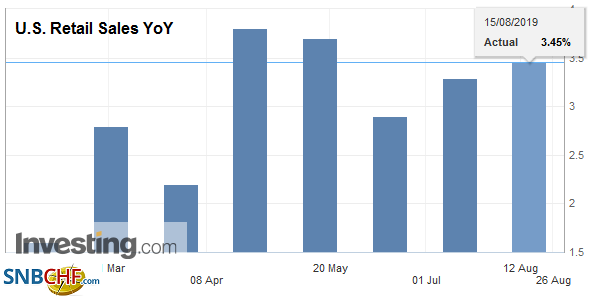

AmericaPresident Trump blamed the Federal Reserve for yesterday’s equity slide. Most observers tie it to the poor Chinese and German data, some of which appears to be adversely impacted by the trade conflict between the US and China. Still, accepting that the Fed’s job is not so much to determine the causes but to respond to shocks by adjusting policy. The market has raised the likelihood that the Fed cuts by 50 bp at the September 18 meeting to 40% from practically zero the day after the July 31 FOMC meeting. The January 2020 fed funds futures contract implies a yield of 1.435%. The current effective average fed funds rate is 2.12%. Almost 67 bp of easing has been discounted for this year. |

U.S. Industrial Production YoY, July 2019(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

| The US economic calendar is chock full. The August NY and Philadelphia Fed surveys and the weekly jobless claims are the most current readings, while the July retail sales and industrial production figures will be helped in calculating Q3 GDP. The inversion of the yield curve has understandably spurred more recession talk and fears, but the data is unlikely to show that a contraction is imminent. |

U.S. Retail Sales YoY, July 2019(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

Canada reports existing home sales for July. Economists look for recovery after a small decline (0.2%) in June. Although the Bank of Canada has a neutral stance, many in the market think that the inversion of the Canadian curve, the prospects of further easing in the US, and the global headwinds, sets the stage for a rate cut at the end of October meeting (57% chance) and an almost 2/3 chance of lower rates by the end of the year. Mexico’s central bank meets today. There is a little more than 25% chance of a cut today. Mexico has among the highest real rates in the world and despite a weak economy, and inflation back within the target range, the central bank has been reluctant to cut rates amid an uncertain policy environment. Waiting for the next meeting (Sept 26) will build on the central bank’s strong credibility in the market.

The US dollar closed above its 200-day moving average yesterday against the Canadian dollar (~CAD1.3310) and is gravitating around there today. Last week’s high was near CAD1.3345, but we suspect there are offers near there that may cap it. The CAD1.3355 level corresponds to a (61.8%) retracement of the June-July US dollar slide. The dollar has become more volatile against the Mexican peso. The dollar pushed through MXN19.77 on Monday but has not seen that level since. Dollar support is not seen until MXN19.50.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$CNY,China House Prices,Currency Movements,Featured,newsletter,U.K. Core Retail Sales,U.K. Retail Sales,Yield Curve