Swiss Franc The Euro has risen by 0.03% at 1.1439. EUR/CHF and USD/CHF, August 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Last week’s dollar losses were initially extended in Asia before it came back bid. The euro briefly poked through .1650 for the first time in three weeks. However, the gains were sold into, and the euro finished the Asian session near .16, where there is a 782 mln euro option expiring, and 2.4 bln euros struck at .1625. Even the first gain in the German IFO in nine months failed to recover its traction in the European morning. The dollar found support a little below JPY111.00 and is virtually unchanged on the day, as US players return

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, Featured, GBP, Germany IFO Business Climate Index, JPY, MXN, newsletter, SPY, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.03% at 1.1439. |

EUR/CHF and USD/CHF, August 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesLast week’s dollar losses were initially extended in Asia before it came back bid. The euro briefly poked through $1.1650 for the first time in three weeks. However, the gains were sold into, and the euro finished the Asian session near $1.16, where there is a 782 mln euro option expiring, and 2.4 bln euros struck at $1.1625. Even the first gain in the German IFO in nine months failed to recover its traction in the European morning. The dollar found support a little below JPY111.00 and is virtually unchanged on the day, as US players return to their posts. With minor exceptions, the dollar has spent the month confined to a JPY110-JPY112 range. There is an option for almost $1 bln struck at JPY112 that expires today but does not appear relevant. Sterling advanced six of the past seven sessions and is flat today. It has been confined to about 15 ticks on either side of $1.2850. The Australian dollar edged through the pre-weekend high but met a wall of offers in front of $0.7350 and it has been pushed back toward $0.7300, which met the 38.2% retracement of last Friday’s advance. Below there, the 61.8% retracement found near $0.7280. The Canadian dollar is unchanged against the US dollar, hugging close to CAD1.30. |

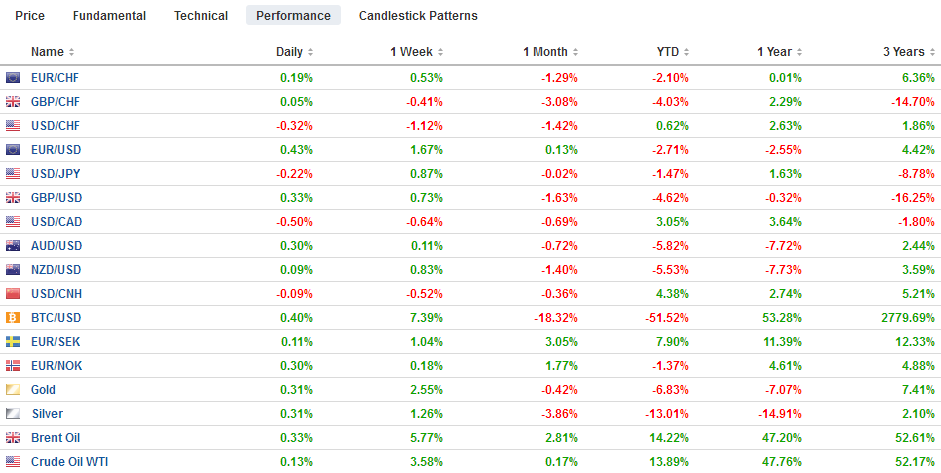

FX Performance, August 27 - Click to enlarge |

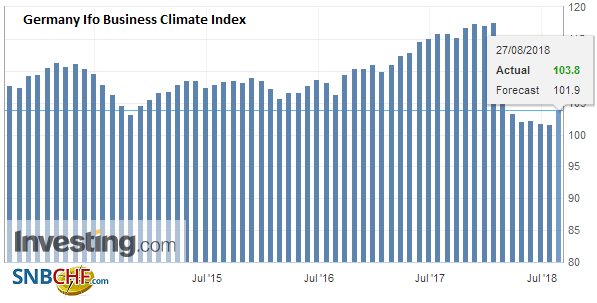

GermanyThe rise in the assessment of the Germany business climate to 103.8 in August from 101.7 in July is the first increase since last November and puts it at its best level since February. The current assessment rose to 106.4 from 105.4, and the expectations component rose to 101.2 from 98.2. This coupled with the improving PMI suggest Europe’s biggest economy is finding its stride and growth around 0.5% is projected for Q3. |

Germany Ifo Business Climate Index, August 2018(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

Italy and the EU are headed for a confrontation. The Italian government’s threatened to withhold payment to the EU unless it shares the migrant burden that the front-line states, like Italy, Greece, and now Spain must contend due to rules that make the first EU country of entry responsible. Now the threat has morphed into the possibility a broader obstructionist role, including blocking the EU budget.

Italian stocks are underperforming, but the debt market is holding its own. The 10-year yield flat, while core yields are up around two basis points and the periphery bonds are edging higher. In the stock market, Milan is underperforming. It is slightly lower while most markets are higher. The Dow Jones Stoxx 600 is up around 0.25% in late morning dealings, while the London market is closed for a bank holiday. Last week, the benchmark rose 0.65% to snap a three-week slide.

China re-introduced a “counter-cyclical” component to set the yuan’s reference rate at the end of last week, and the yuan rallied on the news. It was another signal that Chinese officials had not weaponized the yuan and efforts to arrest its decline was being escalated. The PBOC strengthened the yuan’s reference rate today by about 0.25%, which was a bit stronger than anticipated. However, after surging the most in two-year ahead of the weekend, the onshore yuan slipped 0.2%, and the offshore yuan eased half as much.

Asian equities rallied today. The MSCI Asia Pacific Index gained 1.2%, its biggest gain since early July and has now advanced for six of the past seven sessions. The Shanghai Composite gained almost 1.9% and has moved higher in five of the past six sessions. A move above 2800 would solidify ideas that a low is in place. The Nikkei and Topix gapped higher in Japan. Japan’s Nikkei rose 0.9% and extended its winning streak to a fifth consecutive session. The Topix gained 1.15% and nearly retraced 61.8% of this month’s drop. With the US Secretary of State’s trip to North Korea postponed, it is not surprising that Korean shares underperformed (Kospi +0.25%), but what may be surprising is that foreign investors bought nearly $250 mln of Korean shares today, the most in two weeks.

Most emerging market currencies are under pressures, except the Mexican peso, where optimism that a deal can be struck with the US as early as later today. Turkey’s week-long holiday is over, and the volatility has popped up. The dollar rose more than 3% at one point (~TRY6.195), but now near TRY6.15, it is up about 2.5%. Turkish yields flat. The South African rand is off 1% with the dollar near ZAR14.29. South African shares are up around 1.5% today as is consistent with the 1.2% rally in the MSCI Emerging Markets Index. If the gain is maintained, it would be the largest in over a month. It is approaching an important retracement near 1065, and a move above could open the door for a few more percentage points of gains.

The US and Canadian economic calendars are fairly bare today (Chicago Fed’s national economic activity index and the Dallas Fed manufacturing survey). Our technical assessment that anticipated additional near-term dollar weakness, including the month-end related flows, remains intact, but the price action reinforces the importance of the $1.1650 area in the euro and the 95.00 area in the Dollar Index. The S&P 500 and NASDAQ closed at record highs before the weekend, and both are called higher today.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Featured,Germany IFO Business Climate Index,MXN,newsletter,SPY