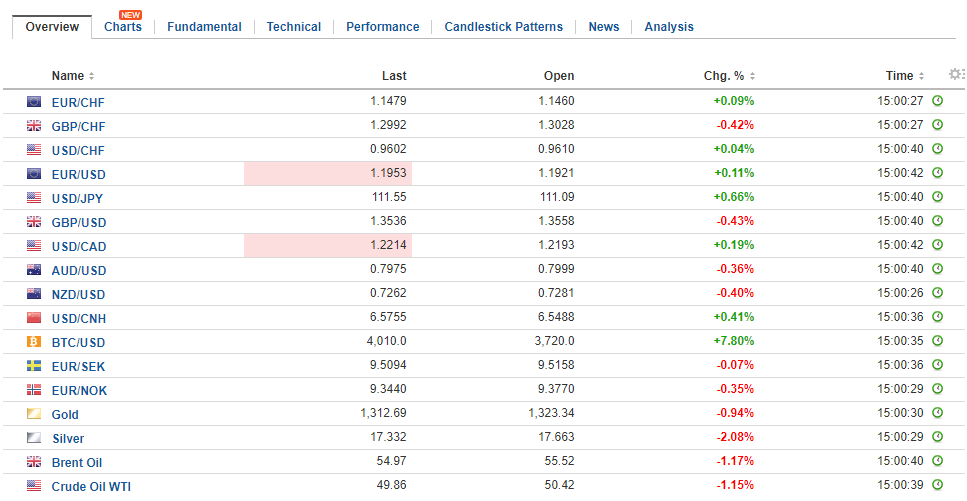

Swiss Franc The Euro has risen by 0.03% to 1.1468 CHF. EUR/CHF and USD/CHF, September 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The unexpected weakness in US retail sales and industrial production reported before the weekend did not prevent US yields and stocks from rising. Asia followed suit, and with Japanese markets closed, the MSCI Asia Pacific Index rallied a little more than 1%, the largest gain in two months. Of note, foreigners returned to the Korean stock market, buying about 0 mln today, which cuts the month’s liquidation in half. The Kospi rallied 1.3% today, the most in four months. The US dollar is firm, mostly in ranges seen before the

Topics:

Marc Chandler considers the following as important: China House Prices, EUR, EUR/CHF, Eurozone Consumer Price Index, Eurozone Core Consumer Price Index, Featured, FX Trends, GBP, JPY, newslettersent, TLT, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has risen by 0.03% to 1.1468 CHF. |

EUR/CHF and USD/CHF, September 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe unexpected weakness in US retail sales and industrial production reported before the weekend did not prevent US yields and stocks from rising. Asia followed suit, and with Japanese markets closed, the MSCI Asia Pacific Index rallied a little more than 1%, the largest gain in two months. Of note, foreigners returned to the Korean stock market, buying about $260 mln today, which cuts the month’s liquidation in half. The Kospi rallied 1.3% today, the most in four months. The US dollar is firm, mostly in ranges seen before the weekend in quiet turnover. The euro held support ahead of $1.1900. It recovered from $1.1840 on September 14 area to $1.1990 before the weekend. A break of the $1.1900 area signals a return to the lows. The dollar’s gains against the yen have been extended to almost JPY111.40, nearly a two-month high. Options that expire today struck at JPY111.00 ($608 mln) and JPY111.20 ($495 mln) may not be in play as the greenback may stretch toward the JPY111.75 area, which is next retracement objective of the decline since the mid-July high near JPY1114.50. |

FX Daily Rates, September 18 - Click to enlarge |

| Sterling is trading in a narrow range near its pre-weekend high (~$1.3615). Even though the BOE under Governor Carney has hinted several times that it would soon consider hiking rates and never did, the verbal guidance has been taken seriously by investors. Within reason, the Brexit issue has ceased to be the key consideration for investors.

Even before the BOE meeting, large speculators in the futures market were large buyers of sterling. They increased the gross long sterling futures position by more than 14k contracts or 25%. The gross shorts barely changed. That said, we caution against reading too much into this positioning which may have been skewed by the coming contract rolls as September contracts are closed or delivered upon and the December contract becomes the most active. There is an option struck at $1.3575 for GBP306 mln today that could come into play. Tomorrow there is 1.3 bln euros struck at GBP0.8750 that expires. If sterling’s run-up on the BOE verbal jousting is a bit exaggerated, as we suspect, sterling could correct toward $1.3440 with damaging the underlying technical picture. |

FX Performance, September 18 - Click to enlarge |

EurozoneEuropean shares are moving higher as well in early Monday turnover. The Dow Jones Stoxx 600, which gained 1.4% last week is being bid through the ceiling near 382 to reach its best level in six weeks. European bonds are firm, with Spain and Italy yields are 4-5 bp lower, while core yields are off fractionally. US 10-year yields rebounded 15 bp last week to 2.20% and are holding near there now. The odds of a Fed hike in December increased last week and are just below 50%, depending on the model (assumptions). The US two-year yield rose 12 bp last week, the most in six months. |

Eurozone Consumer Price Index (CPI) YoY, Sep 2017(see more posts on Eurozone Consumer Price Index, ) Source: Investing.com - Click to enlarge |

| The 10-year breakeven (conventional minus the yield of the inflation protected security) starts the news week near 1.85%, the highest in four months, helped by last week’s CPI report. There is a supply issue too. Later this week, the US will auction $11 bln 10-year TIPS. |

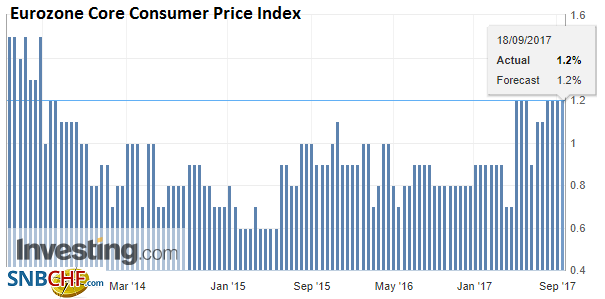

Eurozone Core Consumer Price Index (CPI) YoY, Aug 2017(see more posts on Eurozone Core Consumer Price Index, ) Source: Investing.com - Click to enlarge |

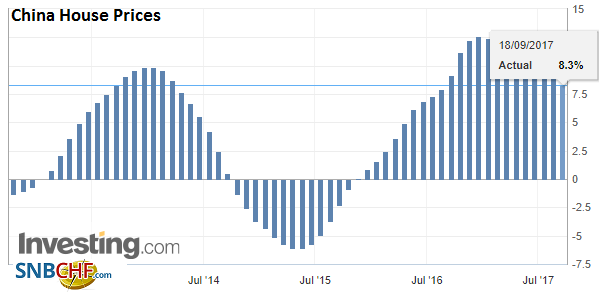

China |

China House Prices YoY, Aug 2017(see more posts on China House Prices, ) Source: Investing.com - Click to enlarge |

There were a few political developments to note. First, local press reports suggest that Japanese Prime Minister Abe, enjoying a boost in support with the firm handling of the North Korea crisis, may call for a snap election. It would prevent the opposition from being prepared. There are many variables that will be weighed, but it looks like a reasonable scenario. While monetary policy is unlikely to change on an Abe victory, though Kuroda’s term does expire next year, the snap election may see some extra spending.

New Zealand’s election on September 23 still appears too close to call. Both the governing Nationals and Labour are drawing around 42% of the vote. Labour’s call for cuts in immigration, new taxes to pay for more transfer payments and a strong social welfare seems to be getting a better hearing than a couple months ago. The Nationals promise tax cuts and infrastructure projects.

In Germany, it is as forgone a conclusion as these things get that Merkel will be re-elected Chancellor. The call from the FDP to all no new EMU members and re-invite Russia to join the G7 seems to be an admission that while it will be represented in the new parliament, it will not be part of the governing coalition. Merkel may have wished a return of its traditional ally. Some in the UK government may have thought a government with the FDP would have softened Germany’s Brexit stance. However, the numbers say that it the next government may look very much like the current one, with Schaeuble (turns 71 today) likely to continue as Finance Minister.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$EUR,$JPY,$TLT,China House Prices,EUR/CHF,Eurozone Consumer Price Index,Eurozone Core Consumer Price Index,Featured,newslettersent,USD/CHF