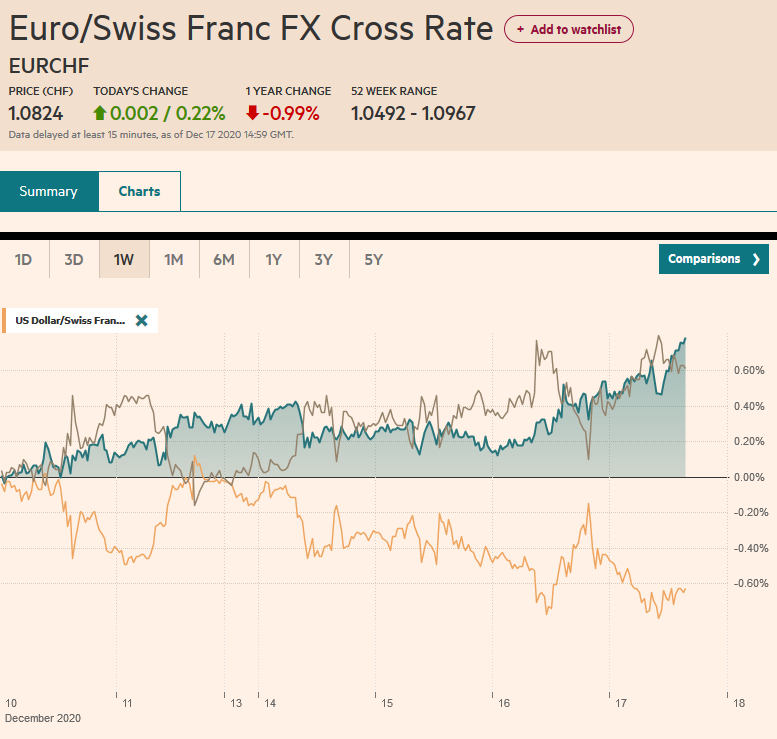

Swiss Franc The Euro has risen by 0.22% to 1.0824 . FX Rates Overview: The prospects of a UK-EU deal and US stimulus continue to underwrite risk appetites and weigh on the dollar. Equity markets are moving higher. Led by Australia and China, the MSCI Asia Pacific Index rose to new record highs, while Dow Jones Stoxx 600 in Europe is at its best level since February. US shares are also trading higher. Bond markets are quiet, with European yields paring yesterday’s gains while the US 10-year benchmark is hovering around 0.92%. The dollar has lurched lower against nearly all the world currencies today. The Norwegian krone is aided by a central bank suggesting it could be among the first major central banks to begin normalizing monetary policy (not until H1 22).

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Australia, Bank of England, China, Currency Movement, currency war, EU, Featured, newsletter, Norway, Switzerland, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.22% to 1.0824 |

. |

FX RatesOverview: The prospects of a UK-EU deal and US stimulus continue to underwrite risk appetites and weigh on the dollar. Equity markets are moving higher. Led by Australia and China, the MSCI Asia Pacific Index rose to new record highs, while Dow Jones Stoxx 600 in Europe is at its best level since February. US shares are also trading higher. Bond markets are quiet, with European yields paring yesterday’s gains while the US 10-year benchmark is hovering around 0.92%. The dollar has lurched lower against nearly all the world currencies today. The Norwegian krone is aided by a central bank suggesting it could be among the first major central banks to begin normalizing monetary policy (not until H1 22). The Australian dollar, boosted by a strong employment report, is leading the majors. The euro’s roughly 0.25% gain to a new 18-month high is a laggard. Meanwhile, emerging market currencies are mostly higher, and the JP Morgan Emerging Market Currency Index is higher for the third consecutive session. Gold is shining in the weak dollar environment. It has risen by about $50 an ounce over the past three sessions, and straddling $1880, it reached its best level in nearly four weeks. Oil is bid as well. Ideas that demand will improve, and a drawdown in US stocks, coupled with the dollar’s weakness, lifted the January WTI contract to almost $49 a barrel, while Brent is closing in on $52. |

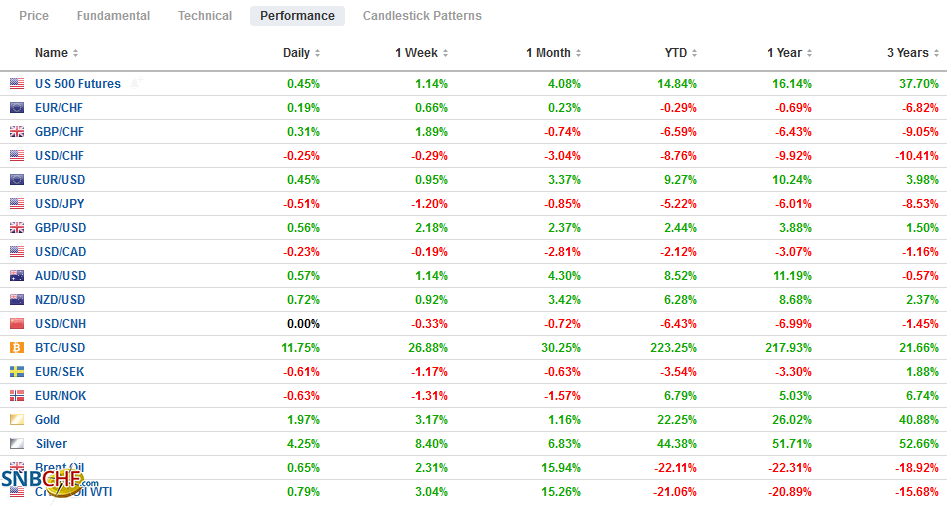

FX Performance, December 17 - Click to enlarge |

Asia Pacific

For the second month in a row, Australia reported employment data considerably better than economists forecast. It created more than double the 40k jobs the Bloomberg median forecast anticipated, and the October surge pushed even higher to 180.4k (from 178.8k). Nearly all the new jobs were full-time positions (84.2k). While the participation rate increase to 66.1% from 65.8%, the unemployment rate eased to 6.8% from 7.0%. Last November, the participation rate was 65.9%.

China avoided being cited as a currency manipulator by the US Treasury Department, but it remains on its watch list. It renewed its call for greater transparency. It noted as many observers have that its large current account surplus, relatively steady yuan, and a small increase in reserves does not add up. It notes that large banks are short yuan. No one has argued that the yuan is free-floating. It is not fully convertible. Several other areas are problematic, including the rising errors and commissions catch-all category.

MSCI announced that, like the other benchmark providers, it too was going to drop companies cited by the US as tied to the Chinese military. MSCI will drop seven companies in early January. S&P Dow Jones is dropping eight companies, and FTSE Russell is dropping 8. A further adjustment could be necessary, as the subsidiaries and affiliates of the 35 companies cited by the US were not excluded on this first cut. MSCI estimated that 0.04% of its global benchmark and 0.25% of its emerging market index are impacted. After surveying 100 fund managers, MSCI concluded that reversing the decision will not a top priority for the Biden administration.

With the US Treasury keeping Japan on its fx watch list as well, Japanese officials may be quieter as the dollar is poised to break below JPY103 than they were a month ago when the dollar was slipping through JPY104. The greenback has not been above JPY103.60 in Asia and is testing JPY103 in the European morning. This is a new nine-month low for the dollar, which hit JPY101.20 in the March chaos. The Australian dollar jumped above $0.7600 and is at a new 18-month high near $0.7640. The next chart point is around $0.7675. It is the fourth consecutive gain for the Aussie. Barring a dramatic reversal tomorrow, it will be the seventh straight weekly advance that began near $0.7000 at the end of October. The PBOC’s reference rate for the dollar was CNY6.5362, spot on the Bloomberg bank survey’s median forecast. The yuan is flat on the day. Against the offshore yuan, the dollar traded to CNH6.50 before returning to yesterday’s settlement level (~CNH6.5125).

EuropeOn the heels of the Treasury’s announcement, the Swiss National Bank argued that it is not manipulating its currency, but it will continue to intervene as necessary. All intervention is not manipulation, and if a country acts like a judge and a jury in determining the difference, it undermines the effort for international cooperation. At the conclusion of its policy meeting today, the SNB left rates unchanged and reiterated that the franc was “highly valued.” SNB President Jordan argued that its intervention is not aimed at securing a trade advantage but fighting deflationary pressures. Unlike the US, eurozone, and Japan, there are not sufficient domestic bonds for its to buy as a result of its fiscal policies. Note that the SNB’s reserves have risen by more than $100 bln in H1 20. |

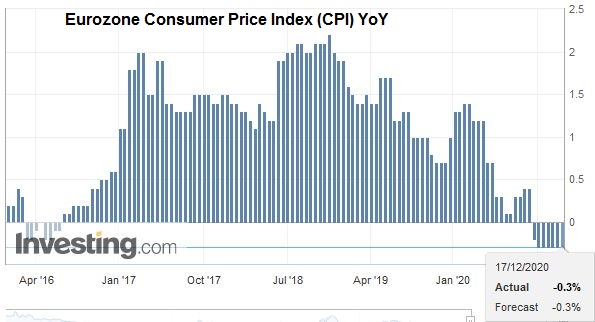

Eurozone Consumer Price Index (CPI) YoY, November 2020(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| Norway’s central bank sees a somewhat faster increase in rates starting in H2 2022 than it did in September. It makes Norway a leading candidate to be among the first of the high-income countries to begin normalizing policy. The Norges Bank has run a fairly orthodox policy. No QE. No negative rates. The government did tap the $1.2 trillion sovereign wealth fund for resources. The currency is the weakest of the majors this year, and that may be helping keep price pressures firm and allowing it to contemplate a hike in 18 months.

The outcome of the Bank of England meeting is awaited. No change is in rates, or Gilt purchases are expected. Barring a surprise, it will be a non-event for sterling, where the market is focused on the weak dollar backdrop and the prospects for a last-minute UK-EU deal. We had been skeptical that a deal could be struck. From the outside, it looked like an old married couple talking at each other and not to each other, and there was much posturing. The UK was jealously seeking to reassert what it sees as its sovereignty. The EU was jilted and determined not to give any incentive whatsoever to others who might contemplate leaving. Still, since the middle of last week’s Johson/von der Leyen dinner, we have sensed a change and a greater commitment to getting a deal done. And at the same time, we continue to recognize that even with an agreement, there will be frustrating disruptions in the UK-EU trade early next year. |

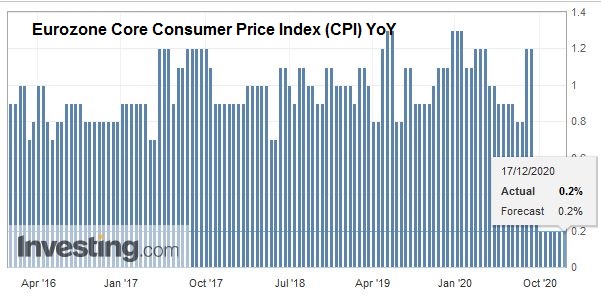

Eurozone Core Consumer Price Index (CPI) YoY, November 2020(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The euro pushed to nearly $1.2245 in late Asia turnover and has stabilized in the European morning. An option for 2.2 bln euros expires tomorrow at $1.2250. Support now is seen in the $1.2180-$1.2200 area. Sterling is trading higher against the dollar for the fourth consecutive session and is approaching $1.36. It finished last week near $1.3225. Partly, this reflects the weak dollar environment, but sterling is also recovering against the euro. The euro is slipping below GBP0.9000 after hitting GBP0.9230 at the end of last week. Important support is seen near GBP0.8980, which houses the lows from earlier this month and the 200-day moving average. A convincing break could target GBP0.8900.

America

The Federal Reserve said little new and did nothing. What it did say was important, though. It linked its future bond purchases to “substantial” progress toward its targets. The median forecast of the members for growth was ratcheted up and unemployment down. In September, four officials saw a hike in 2023 as likely being appropriate, and now five do. The extension of the dollar swaps and repo facility for foreign central banks is simply prudent and predictable, even if the former is a shadow of its former self. The latter does not appear to have been used. The markets wobbled initially; maybe disappointment in some quarters that the pace and composition of its bond purchases were unchanged, but it quickly found its footing. Stocks firmed into the close, and the long-end yields pulled back.

Treasury issued its long-overdue report on the international economy and the foreign exchange market. It cited Switzerland and Vietnam as currency manipulators and added India, Thailand, and Taiwan to the watch-list. The watch-list also includes China, Japan, South Korea, Germany, Italy, Singapore, and Malaysia. It is the first time since China was cited last year (and reversed quickly after signing the Phase 1 trade deal), which itself was the first time since 1994 that one or more countries were cited as manipulators. It was a mechanistic exercise. There are three criteria, bilateral imbalance with the US, large global imbalance, and repeated intervention on one side of the market. It makes no difference if a currency is overvalued, as is the Swiss franc or is too small and too poor, like Vietnam. The currency manipulators are to enter into talks with the US. Treasury Secretary Mnuchin will not be there. When Mnuchin took office, there was a coherent dollar policy. Since 1995, the US refrained from talking the dollar down. Rubin’s strong dollar policy stuck more or less. For the most part, other large countries refrained from doing the same. It was an arms control agreement of sorts. China’s behavior complicated matters, but the dollar policy is in disrepair.

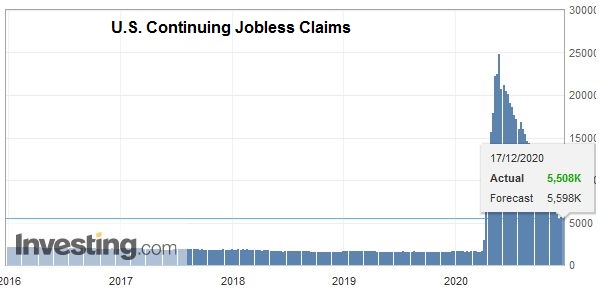

| The US reports weekly jobless claims (a small decline is expected after last week’s surprise increase), housing starts and permits (among the sectors leading the recovery), and the Philadelphia and Kansas City Fed surveys (likely softer). These data points do not have the heft to reverses the dollar’s weakness or substantially alter views of the economy. The weakness seen in yesterday’s retail sales bodes ill for next week’s more comprehensive personal consumption report. The flash PMI suggests the economic momentum waning into year-end, especially in services, which seems related to the pandemic. Today, Canada has a light agenda after yesterday’s CPI, where the firmness of the headline masked flat underlying measures. Tomorrow it reports October retail sales, which are most unlikely to match September’s strength (1.1% headline gain and 1.0% excluding autos. Mexico’s central bank meets and is widely expected to keep the overnight target rate at 4.25%. There was one dissent last month, and it could be repeated again. Still, the majority seem to want to wait for confirmation that price pressures are moving lower in a sustained fashion rather than a one-off related to sales discounts. |

U.S. Continuing Jobless Claims, December 17, 2020(see more posts on U.S. Continuing Jobless Claims, ) Source: investing.com - Click to enlarge |

The US dollar is trading heavily against the Canadian dollar near CAD1.2700. The 2.5-year low was set a couple of days ago, a little below CAD1.2680. The price action has been chopped and has seen intraday upticks extent to almost CAD1.2800. Note that today’s high of CAD1.2750 matches the strike of a $1.1 bln option that expires today. The greenback tested the MXN20.25 level earlier this week. That may have been the bounce that some had looked for. A four-day dollar bounce ended Tuesday, and today it is offered for the third consecutive session. It is trading near MXN19.75, and the low seen last week was near MXN19.70. A break of that targets the MXN19.50 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

2020-11-05

Overview: The markets did not wait for the final vote count and took stocks and bonds higher while pushing the greenback lower. While it appears Biden will be the next US President, investors seemed to like the fact that his agenda will be checked by a Senate that may remain in Republican hands. Stocks are on a tear.

FX Daily, September 28: Stocks Recover while the Greenback Consolidates

FX Daily, September 28: Stocks Recover while the Greenback Consolidates

2020-09-28

Overview: Following the strong finish in the US before the weekend, global equities are paring last week’s slide. The MSCI Asia Pacific Index rose to for a second session. Markets in Japan, Taiwan, South Korea, and India rose by more than 1%. China and Australia were notable exceptions.

FX Daily, October 15: Markets Shake and Dollar Goes Bid

FX Daily, October 15: Markets Shake and Dollar Goes Bid

2020-10-15

A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off.

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

2020-11-09

The new week has begun with robust risk appetites, driving stocks and stocks higher and sending the dollar broadly lower. Nearly all the equity markets in the Asia Pacific region gained more than 1%, except Malaysia and Indonesia.

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

2020-11-13

Overview: The largest bourses in the Asia Pacific region followed the US equity market lower, with the Nikkei posting its first loss in nine sessions. China, Hong Kong, and Australia moved lower as well. On the week, the MSCI Asia Pacific Index gained about 1% after rising 6.3% in the prior week.

FX Daily, November 19: Surging Virus Saps Risk Appetites

FX Daily, November 19: Surging Virus Saps Risk Appetites

2020-11-19

Overview: News that the New York City was closing the schools to contain the virus sent stocks reeling in late North American dealings yesterday and spurred some profit-taking in the Asia Pacific and Europe. Equities in the Asia Pacific region were mostly lower, though China, South Korea, and Australia’s advanced and Tokyo markets were mixed.

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

2020-12-02

The selling pressure that drove the dollar lower yesterday has abated, and the greenback is paring yesterday’s loss, though the dollar-bloc currencies are showing some resilience. EC negotiator Barnier briefed ministers that the same three issues that have bedeviled the trade talks with the UK remain unresolved (fisheries, level playing field, and a conflict resolution mechanism).

FX Daily, December 15: The Bulls are Emboldened

FX Daily, December 15: The Bulls are Emboldened

2020-12-15

The S&P fell for the fourth consecutive session yesterday, the longest losing streak of the quarter, and this seemed to encourage profit-taking in the Asia Pacific region today. The MSCI Asia Pacific Index slipped for the second consecutive session, and even confirmation of the Chinese recovery failed to lift the Shanghai Composite.

Tags: #USD,Australia,Bank of England,China,Currency Movement,currency war,EU,Featured,newsletter,Norway,Switzerland