Hiking rates into a wildly overvalued market is potentially a mistake. So says Bank of America in a recent article. Optimists expecting the stock market to weather the rate-hike cycle as they’ve done in the past are missing one important detail, according to Bank of America Corp.’s strategists.While U.S. equities saw positive returns during previous periods of rate increases, the key risk this time round is that the Federal Reserve will be “tightening into an overvalued market,” the strategists led by Savita Subramanian wrote in a note.“The S&P 500 is more expensive ahead of the first rate hike than any other cycle besides 1999-00,” they said.” – Yahoo Finance While many media experts suggest that investors should not be concerned about rate hikes, BofA

Topics:

Lance Roberts considers the following as important: 9) Personal Investment, 9a.) Real Investment Advice, Featured, Investing, newsletter, Technically Speaking

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Hiking rates into a wildly overvalued market is potentially a mistake. So says Bank of America in a recent article.

Optimists expecting the stock market to weather the rate-hike cycle as they’ve done in the past are missing one important detail, according to Bank of America Corp.’s strategists.

While U.S. equities saw positive returns during previous periods of rate increases, the key risk this time round is that the Federal Reserve will be “tightening into an overvalued market,” the strategists led by Savita Subramanian wrote in a note.

“The S&P 500 is more expensive ahead of the first rate hike than any other cycle besides 1999-00,” they said.” – Yahoo Finance

While many media experts suggest that investors should not be concerned about rate hikes, BofA makes a very valid point regarding valuations.

Before we get there, we need to review current valuation levels and how we got here.

Valuations are a function of three components:

- Price of the index

- Earnings of the index

- Psychology

The price-to-earnings ratio, or the P/E ratio, is the most common visual representation of valuations. However, we tend to forget that ” psychology ” drives investors to overpay for those future earnings.

In other words, while valuations, in the long run, reflect future returns, in the short run, they reflect investor sentiment.

So, back to BofA, how could hiking rates now be problematic for stocks?

Historical Valuations And Fed Hikes

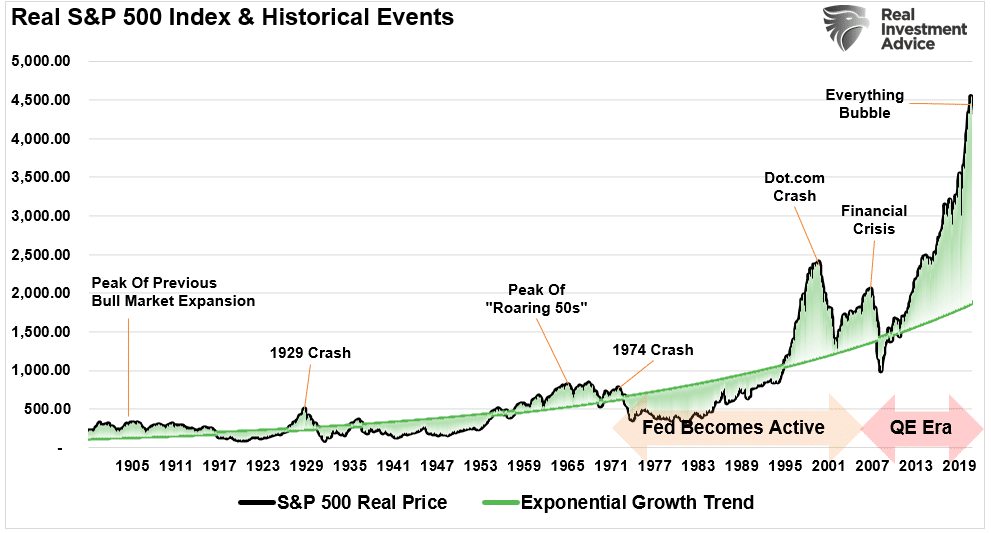

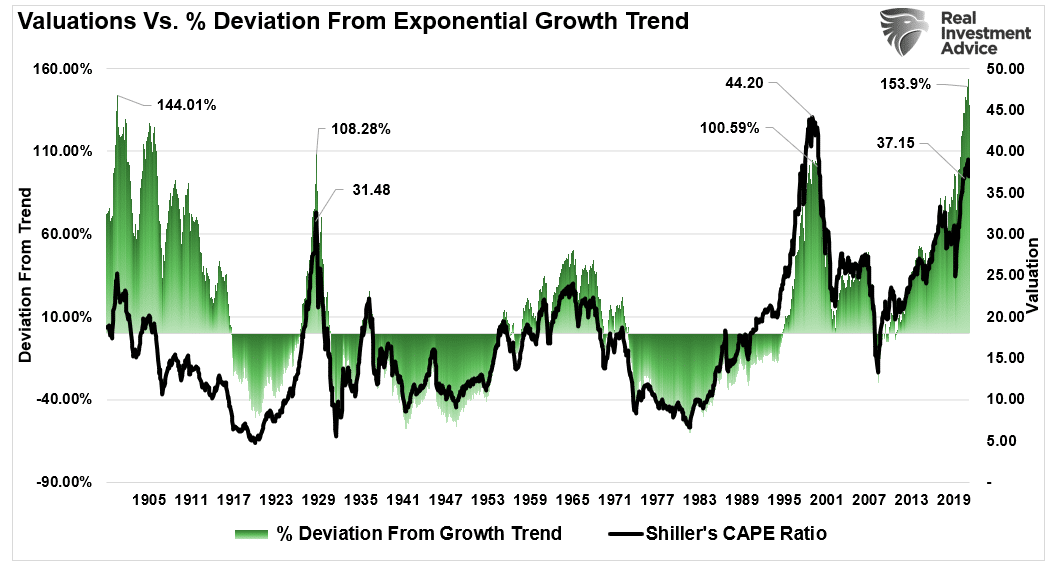

We recently discussed the massive deviation from long-term growth trends for the S&P 500. To wit:

Over the last 12-years, the pace of price increases accelerated due to massive fiscal and monetary interventions, extremely low borrowing costs, and unrelenting “corporate buybacks.” As shown, the deviation from the exponential growth trend is so extreme it dwarfs the “dot.com” era bubble.

That massive flood of liquidity from the Government checks to households, the Fed’s zero-interest-rate policy, and $120 billion in monthly bond purchases had to go somewhere. Instead, it showed up as inflation in both prices of goods and services and financial assets. Currently, market valuations are more extended than at any other point in history other than the “Dot.com” bubble.

Realigning the data above, we see that valuation extremes are a function of price extremes.

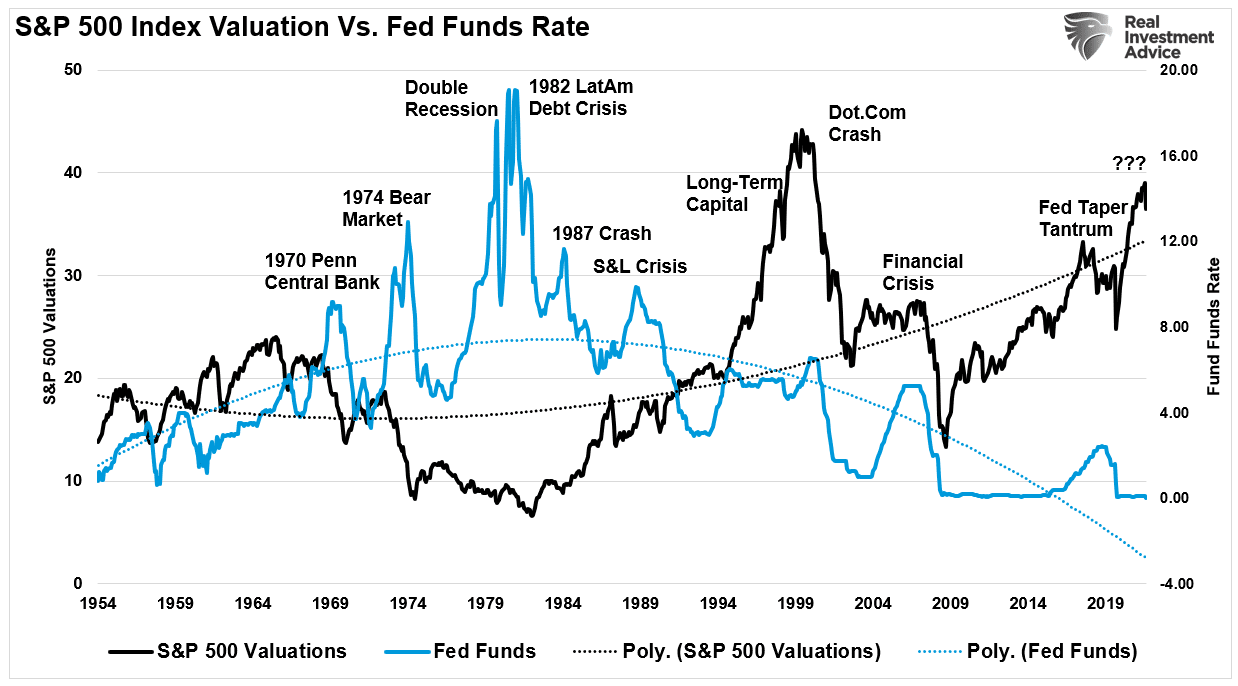

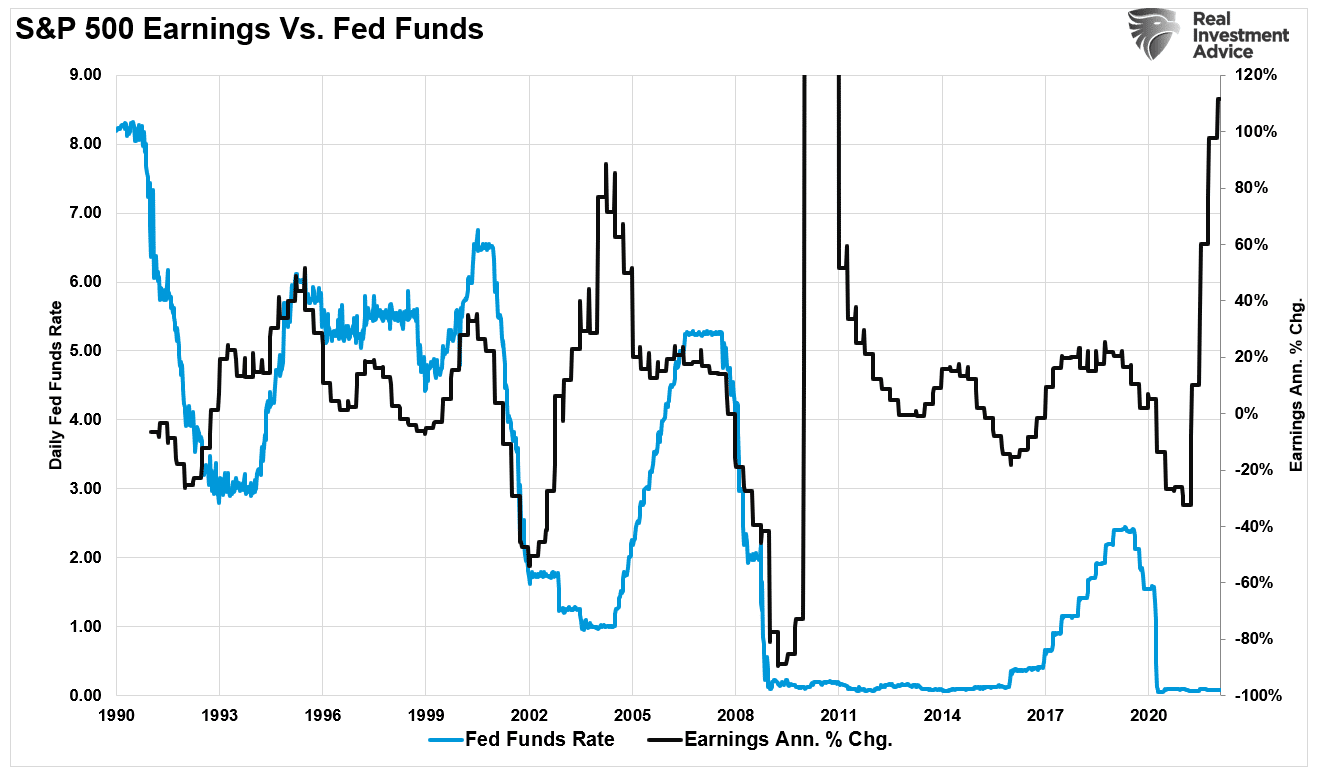

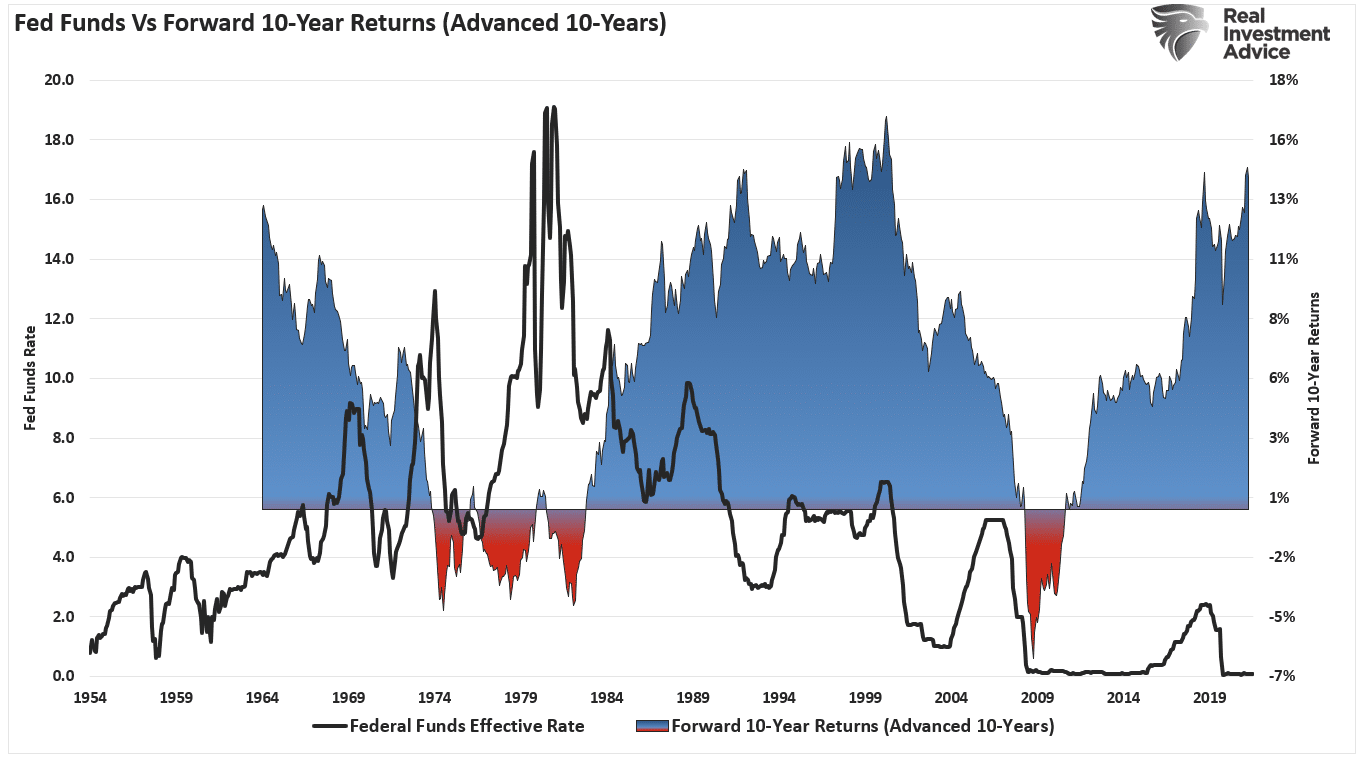

Jerome Powell clearly understands that a decade of monetary infusions and low rates created an asset bubble larger than any other in history. History shows that previous rate hiking cycles, particularly with elevated valuation levels in 1972, 1999, and 2007, led to poor outcomes.

Investors chase stocks on expectations of continued economic and earnings growth, so they risk disappointment. When the Fed tightens monetary policy to slow economic growth and quell inflation, such leads to a reversal in earnings.

Given already high valuations, the outcome will not be what investors were told to expect.

The Problem Of High Valuations And Forward Returns

For investors, the primary bullish arguments for overpaying for valuation over the last decade was three-fold:

- Earnings growth,

- Low interest rates; and,

- Quantitative Easing.

The premise was that with the Fed keeping rates at zero and earnings growth, the present value of future cash flows from equities would rise enough to justify their valuation. Furthermore, the Fed supporting asset prices with massive rounds of Quantitative Easing (QE) investment risk got removed. While true, assuming all else is equal, a falling discount rate does suggest a higher valuation.

“Instead of regarding stocks as a fixed-rate bond with known nominal coupons, one must think of stocks as a floating-rate bond whose coupons will float with nominal earnings growth. In this analogy, the stock market’s P/E is like the price of a floating-rate bond. In most cases, despite moves in interest rates, the price of a floating-rate bond changes little, and likewise the rational P/E for the stock market moves little.” – Cliff Asness

As Cliff notes, zero-interest rates and rising earnings growth supports high valuations. However, if earnings growth is declining as the Fed is hiking rates, such would logically denote lower future valuations. In this instance, to have a lower P/E ratio, as the (E) is declining, the (P) must also decrease.

Simply, if low-interest rates are bullish for equities, then higher rates can not be. They can’t be both.

Financial history confirms the logic.

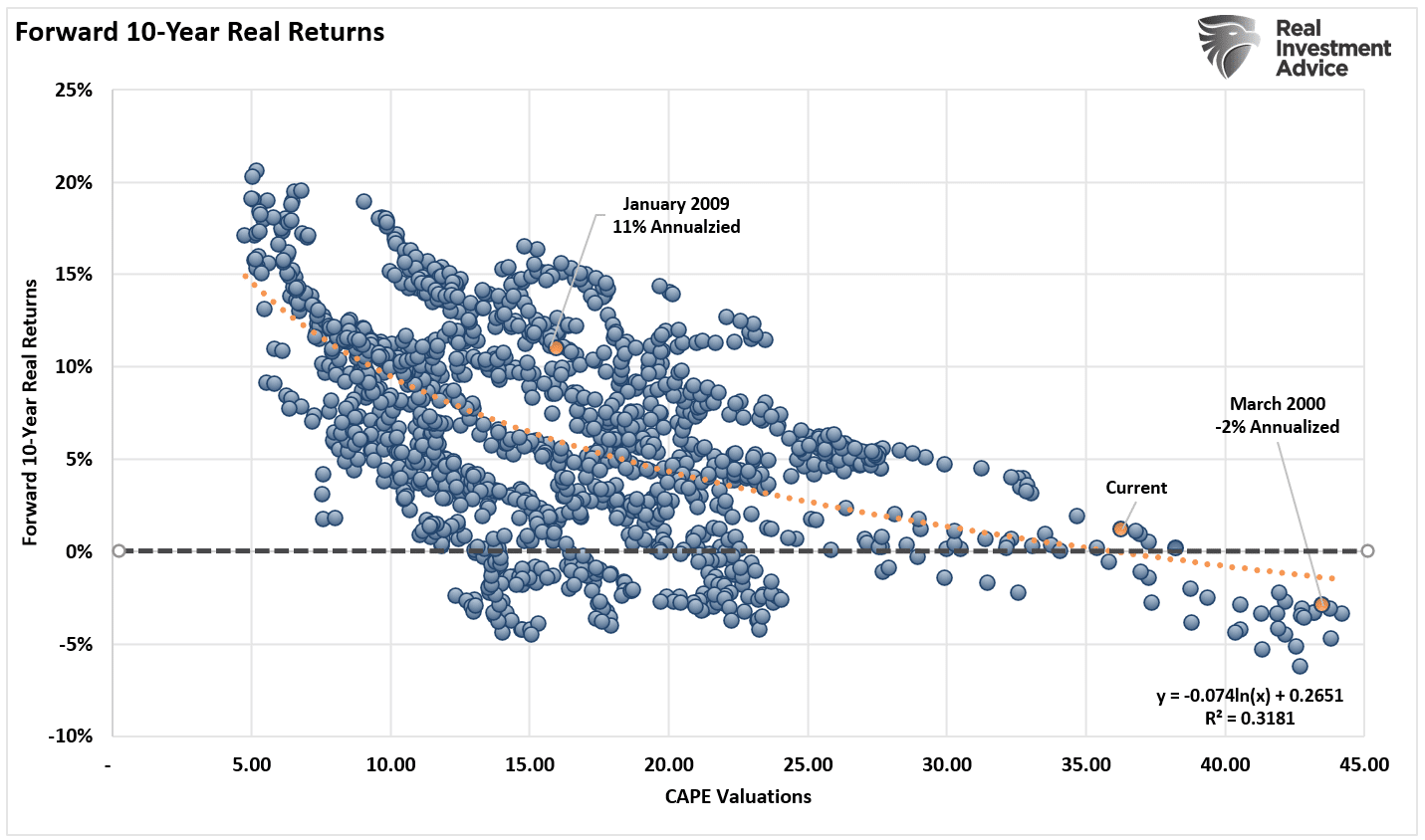

As we already know, high valuations lead to low future returns, as noted by 120-years of data. (Data courtesy of Dr. Robert Shiller)

However, logic and data also show that future returns decline when the Federal Reserve hikes rates, particularly in combination with elevated valuations.

This Time Is Unlikely Different

While market analysts continue to develop a variety of rationalizations to justify high valuations, none of them hold up under objective scrutiny. As noted previously:

“The problem is while Central Bank interventions boost asset prices in the short-term, over the long-term there is an inherently negative impact on economic growth. As such, it leads to the repetitive cycle of monetary policy.

- Monetary policy drags forward future consumption leaving a void in the future.

- Since monetary policy does not create self-sustaining economic growth, ever-larger amounts of liquidity are needed to maintain the same level of activity.

- The filling of the “gap” between fundamentals and reality leads to economic contraction.

- Job losses rise, wealth effect diminishes, and real wealth reduces.

- The middle class shrinks further.

- Central banks act to provide more liquidity to offset recessionary drag and restart economic growth by dragging forward future consumption.

- Wash, Rinse, Repeat.

If you don’t believe me, here is the evidence.

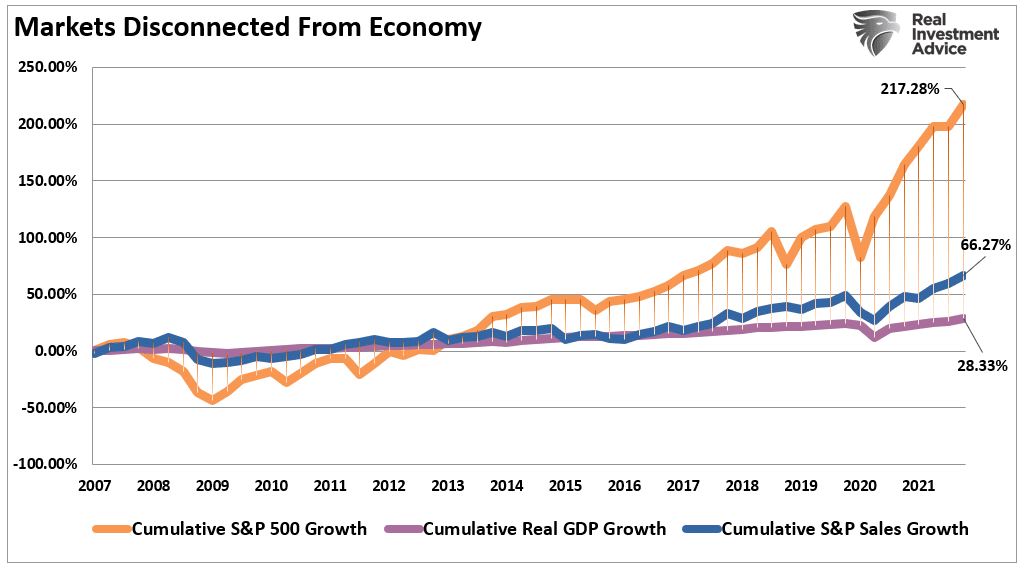

“Through the end of Q2-2021, using quarterly data, the stock market has returned almost 217% from the 2007 peak. Such is more than 7.5x the GDP growth and 3.2x the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)“

While it is “bullish” to come up with reasons to justify overpaying for assets in the short term, “fighting the Fed” is generally a “no-win” situation.

That means if a massive flood of liquidity, QE, and zero rates was your thesis for overpaying for earnings previously, the reversal of that policy is not.

You don’t get to have it both ways.

The post Hiking Rates Into Peak Valuations Is A Mistake appeared first on RIA.

You Might Also Like

SWIFT Ban: A Game Changer for Russia?

SWIFT Ban: A Game Changer for Russia?

2022-03-04

As part of the sanctions against Russia, seven Russian banks have been cut off from SWIFT.

We start by discussing what SWIFT is, and then the implications of completely cutting Russia out of SWIFT.

What is SWIFT and Why Russia is Being Excluded

SWIFT – The Society for Worldwide Interbank Financial Telecommunication is a messaging system that links more than 11,000 banks in 200 countries.

The system doesn’t move actual money between the banks but transmits messages between banks with instructions to settle transactions.

Additionally, this system is crucial to the international trade system – without it, countries wouldn’t be able to settle trade transactions between countries.

The bar charts in the graphic from the Wall Street Journal below illustrate the growth

Saving Money in Inflationary Times

Saving Money in Inflationary Times

2022-03-04

(3/4/22) Girl Scout Cookie Season returns with a vengeance; selling techniques & economic impact. Market performance continues to baffle,. Why is everyone’s side-job selling Real Estate? the importance of teaching kids the value of money and delayed gratification; money saving lessons for today from the Great Depression: eliminating recurring charges, lowering credit card rates, paying with cash, keeping up with automobile maintenance, Raising insurance deductibles, using online banks, and ditching banks with fees.

2:03 – Girl Scout Cookies & Market Performance in Troubled Times

13:10 – Money Scripts & The Value of Delayed Gratification

29:12 – Saving Money in Inflationary Times, Pt.1

43:16 – Saving Money in Inflationary Times, Pt.2

Hosted by RIA Advisors Director of Financial

2022-03-01

“Sell Energy Stocks” Was Originally Published At Marketwatch.com

Sell energy stocks? Such certainly seems counter-intuitive advice given high oil prices, geopolitical stress, and surging inflation. However, some issues suggest this could indeed be the time to “sell high.”

Before we go further, it is essential to state that I am not recommending selling energy stocks in total. As is always the case, portfolio management is about minimizing risk and preserving capital. Reducing energy exposure by selling portions of existing positions is more prudent.

As shown, there is a high correlation between the price of oil, the energy sector as represented by SPDR Energy ETF (XLE,) and even oil stocks like Exxon Mobil (XOM.) Therefore, if oil prices decline, energy stocks will also.

Market Selloff Into January

Market Selloff Into January

2022-01-19

The market selloff into January rattled investors as concerns of “So Goes January, So Goes The Year” began to dampen expectations. Combined with a more aggressive stance from the Federal Reserve, rising inflation, and a reduction in liquidity, investor concerns seem to be well-founded.

Is a Fed Taper GOOD for Markets?

Is a Fed Taper GOOD for Markets?

2021-11-22

At what interest rate will markets say, "enough?" The Instability of Stability is Markets’ biggest risk; What is the Fed’s taper-rate? Markets predict two rate hikes in 2022; Just because seasonality is here, don’t be unwary; concern over return of capital, not return on capital.

——

0:02 – What is the Interest Rate Threshold for Market Correction?

11:06 – What is the Fed’s Real Taper-rate?

22:31 – Christmas Trees, Turkeys, Going to the Dr.; Return of Capital

Hosted by RIA Advisors Chief Investment Strategist Lance Roberts, CIO

——–

Articles Mentioned in this show:

https://realinvestmentadvice.com/rising-interest-rates-matter-to-the-stock-market/

https://realinvestmentadvice.com/fed-taper-will-awaken-the-sleeping-bond-bull-market/

——–

Our Latest "Three Minutes on Markets &

Crypto’s Crash and Stocks Head Higher

Crypto’s Crash and Stocks Head Higher

2021-11-17

“Crypto’s Crash,” says some financial news headlines. The reality is Bitcoin, Ethereum and others are down about 10-15% in the last few days. The word “crash” may seem appropriate to describe the sharp decline, except 10%+ moves in a matter of days is the norm, not the exception for crypto.

Technically Speaking Tuesday (11/16/21): Market Technical Analysis & Commentary from RIA Advisors…

Technically Speaking Tuesday (11/16/21): Market Technical Analysis & Commentary from RIA Advisors…

2021-11-17

➢ Listen daily on Apple Podcasts:

https://podcasts.apple.com/us/podcast/the-real-investment-show-podcast/id1271435757

➢ Watch Live daily on our Youtube Channel:

www.youtube.com/c/TheRealInvestmentShow

➢ Upcoming personal finance free online events:

https://riaadvisors.com/events/

➢ Sign up for the Newsletter:

https://realinvestmentadvice.com/newsletter/

➢ RIA Pro Free Trial: Analysis, Research, Portfolio Models, and More.

https://riapro.net/home

Visit our Site: www.realinvestmentadvice.com

Contact Us: 1-855-RIA-PLAN

https://twitter.com/RealInvAdvice

https://twitter.com/LanceRoberts

https://www.facebook.com/RealInvestmentAdvice/

https://www.linkedin.com/in/realinvestmentadvice/

#Fed #Bitcoin #Gold #Stocks #Trading #rates #Money #Markets

10 Smart Money Moves to Make Right Now.

10 Smart Money Moves to Make Right Now.

2021-10-28

2021 isn’t over yet. So here are 10 smart money moves to make right now.

Saving money should be a year-round endeavor, but life gets in the way just like anything else. So with 2021 coming to a swift, thankful end, take advantage of the fourth quarter to accelerate your financial acumen, bolster your balance sheet and successfully springboard into the new year.

Tip One: Max Out HSA Contributions for 2021.

A Health Savings Account is a pre-tax savings miracle account. What other vehicle allows investors to sock money away triple tax-free? There’s no doubt HSAs have caught on with investors. According to Devenir’s latest survey, a national leader of investment solutions for Health Savings Accounts, the number of HSAs has now exceeded 30 million.

The popularity of HSAs

Tags: Featured,Investing,newsletter,Technically Speaking