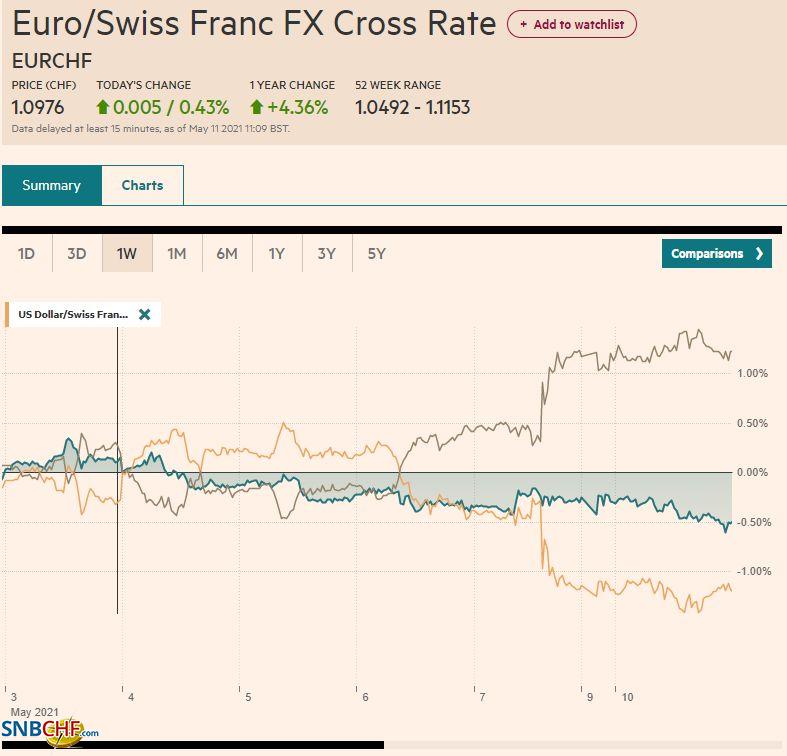

Swiss Franc The Euro has risen by 0.43% to 1.0976 EUR/CHF and USD/CHF, May 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Last week’s cyberattack on the largest US gasoline pipeline continues to lift oil and gasoline prices. The June gasoline futures gapped higher to extend last week’s 2.4% gain but has subsequently moved lower to enter the gap. June WTI is firm and holding above . The supply disruption is key, but iron ore prices soared 10% on strong Chinese demand. More broadly, the CRB Index settled last week at six-year highs. Led by South Korea, Asia Pacific equities markets moved higher, and Australia’s ASX rose to a new record high. Europe’s Dow Jones Stoxx 600 is up fractionally but sufficient

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, Currency Movement, EUR/CHF, Featured, Federal Reserve, Germany, jobs, newsletter, Olympics, U.K., USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.43% to 1.0976 |

EUR/CHF and USD/CHF, May 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Last week’s cyberattack on the largest US gasoline pipeline continues to lift oil and gasoline prices. The June gasoline futures gapped higher to extend last week’s 2.4% gain but has subsequently moved lower to enter the gap. June WTI is firm and holding above $65. The supply disruption is key, but iron ore prices soared 10% on strong Chinese demand. More broadly, the CRB Index settled last week at six-year highs. Led by South Korea, Asia Pacific equities markets moved higher, and Australia’s ASX rose to a new record high. Europe’s Dow Jones Stoxx 600 is up fractionally but sufficient to also set a new record high. US futures are narrowly mixed, with the NASDAQ trailing. The US 10-year yield recovered smartly after the sharp and quick drop on the back of the weak jobs data. It is steady today near 1.58%. European yields are narrowly mixed. The UK Gilt yield is up a couple of basis points, while Australia and New Zealand saw their 10-year yield rose three basis points. The dollar is mostly softer. Sterling and the dollar bloc are leading the majors, while the yen is softer. The South Korean won is leading emerging market currencies higher. The eastern and central European currencies are laggards, though the Hungarian forint is more resilient. The JP Morgan Emerging Market Currency Index is advancing for the fourth consecutive session. Last week’s 1.7% gain was the most since last November. Gold is firm but below the pre-weekend high (~$1843.50). The yellow metal may be pausing ahead other $1850 area, which is where the 200-day moving average is found. |

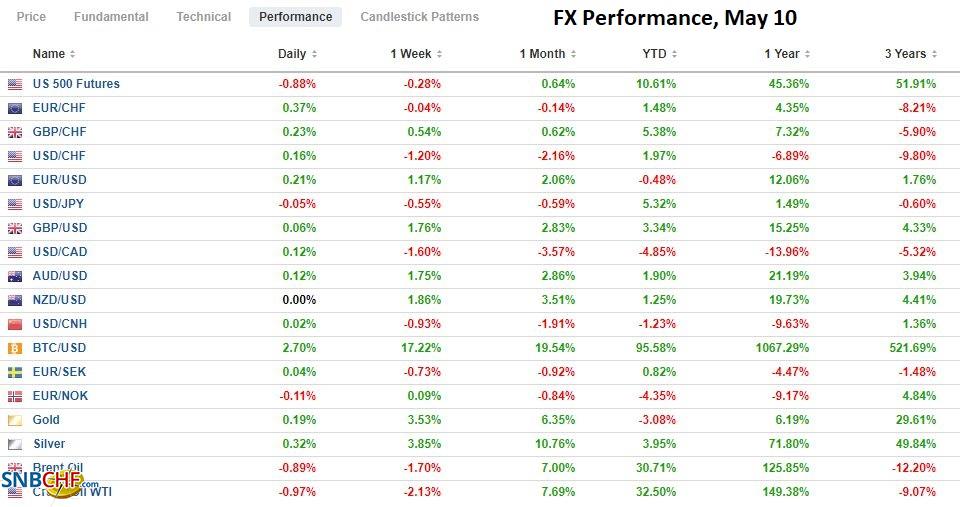

FX Performance, May 10 - Click to enlarge |

Asia Pacific

The yen rose to two-week highs at the end of last week but has come back offered today. The exchange rate remains hyper-sensitive to US rates. Meanwhile, the formal state of emergency for Tokyo and three other prefectures was extended at the end of last week through the end of the month. The emergency declaration was broadened to the industrial regions in Aichi and the prefecture of Fukuoka. It now covers around 40% of the economy and most major urban centers. The latest poll (JNN) found support for Prime Minister Suga fell to its lowest level of his eight-month tenure. His support was at 40%, down from 44.4% last month. Nearly 2/3 of the respondents (63%) said there disapproved of the government’s handling of the pandemic, a 13 percentage point rise. A separate poll (Yomiuri) found 60% want the Olympic games canceled. Suga will face a leadership contest within the LDP in September ahead of the national election, which must be held by the end of October.

The PBOC set the dollar’s reference rate weaker than expected, and the gap between the fix and the market expectations (e.g., median projection in Bloomberg’s survey of bank models) was particularly wide. Bloomberg calculates it was the widest since January (CNY6.4425 vs. forecast for CNY6.4370). As we detected in the pre-weekend fix as well, Chinese officials appear to be trying to slow the yuan’s rise. The yuan is at a three-year high today, with the greenback approaching CNY6.4100.

Tomorrow Australia’s government will announce its budget. In many respects, it will look like the Us approach with strong infrastructure measures, social spending, and extended tax income-tax breaks for low and middle-income households. The faster-than-expected growth and the surge in iron ore prices boost the government’s revenues, allowing it to record a smaller than expected budget deficit. Meanwhile, Australia’s vaccine rollout out so far has been slow, and before the weekend, the Trade Minister warned international visitors may remain restricted well into H2.

The dollar is within the pre-weekend range against the Japanese yen (~JPY108.35-JPY109.30). The stabilization of the US 10-year yield appears to have helped. The JPY109 area is the halfway point of last week’s range, and the greenback stalled a little above there. The next retracement target (61.8%) is near JPY109.20. The dollar looks poised to snap a three-day slide today. It finished last week near JPY108.60. The Australian dollar is extending its gains for the fourth consecutive session. Around $0.7870, it is at its best level since the end of February. There is an option for roughly A$640 mln at $0.7900 that expires today. The multi-year high was set on February 25, a little above $0.8005. Since April 9, the Chinese yuan has only fallen in two sessions. However, the pace of its ascent has quickened. Since returning from the May Day holidays last Thursday, the dollar has fallen by nearly 1%. It took almost two and half weeks to fall by the last 1%. The offshore yuan is a bit stronger than the onshore yuan. Official protests may escalate, and among the measures it has adopted before, it can make it easier to invest abroad.

Europe

The UK government did well in last week’s local elections, and it is set to ease social restrictions further in about a week’s time. Last week, the Bank of England announced it will slow its weekly bond purchases and looks to complete them by the end of the year. The opposition Labour is in a bit of disarray after losing some traditional strongholds, and party leader Starmer’s initial reaction to downgrade his deputy did not boost confidence and was ridiculed by other Labour leaders. The SNP did not secure an outright majority in Scotland, but with the Greens, a clear majority favor independence. Still, the public health crisis is the first order of business, and the SNP does not envision a referendum until toward the middle of the five-year term.

Support for Germany’s CDU/CSU slipped to 23% from 24% in the latest polls. Support for the Greens eased a percentage point as well to 26%. The SPD lag behind in third place. It formally endorsed Scholz, the current Finance Minister as its candidate over the weekend. However, he tacked left with a call for more progressive taxes to pay for expanded social programs in his acceptance speech. The SPD challenge is to distinguish itself after being the junior coalition partner to the CDU/CSU since 2013.

The euro rose by nearly 0.85% ahead of the weekend to reach about $1.2170, its highest level since the end of February. It was the largest gain of the year. It made a marginal new high today but is really consolidating after a strong advance. Recall that in the middle of last week, it briefly traded at two-and-a-half week lows near $1.1985. Resistance is seen near $1.22 now, and the late February high was near $1.2245. Initial support is pegged near $1.2130 and then $1.2100. Sterling rose to almost $1.41 today after testing $1.38 at the start of last week. It peaked a little above $1.4235 on February 24. The $1.4100 area offers nearby resistance, and the intraday technical readings are stretched. Support is seen by $1.4050. The euro stalled near GBP0.8700 last week, the upper end of its recent range, and appears poised to test support in the GBP0.8590-GBP0.8600 area.

America

The disappointing April employment data spurred a debate about the nature of the problem. Tomorrow’s Job Opening and Labor Turnover Survey (JOLTS) will be looked up to shed some fresh light on the issue, but the issue has been terribly partisan. Some, including the Chamber of Commerce, see the main culprit being the government’s income support and the federal unemployment insurance supplement. Others, including the Biden administration, argue that the main challenge is the partial re-opening of the economy and that many have not been able to return to work because they are taking care of family members (children and seniors).

There is a secondary argument the suggests if the modest bump in unemployment insurance coverage is sufficient to deter the return of employees, it says something about the low pay, below what is called a “living wage.” In the public health crisis, poverty itself was seen as a comorbidity. Initial industry-level analysis suggests that there does not seem to be an obvious relationship between the slow job gain and the relative wage. Hiring in some high and mid-wage sectors slowed while others quickened. Leisure and hospitality reported a 331k increase in employment, mostly associated with lower-wage positions. Personal and laundry services grew 14k positions. On the other hand, employment by couriers and messengers fell by 77k.

The knee-jerk reaction to the jobs report saw the 10-year yield dropped 10 basis points to 1.46%, but it snapped back completely in less time it took to make a cup of coffee. Net-net, the 10-year yield closed higher (albeit slightly) ahead of the weekend. The market concluded after the employment data that the Fed was less likely to raise rates next year and that inflation is likely to result. As a result, the 10-year break-even rate rose to a fresh eight-year high, a little above 2.50%.

With this backdrop, the US Treasury will sell $126 bln at its quarterly refunding this week, and projections suggest as $40-$45 bln of US investment-grade corporate bonds. At the same time, the US is expected to report a surge in April CPI as the base effect peaks. Recall that in April 2020, headline CPI fell by 0.7%. It is expected to be replaced with a 0.2% gain last month. In May last year, CPI slipped by 0.1%. Core CPI fell by 0.4% in April 2020. It is expected to have risen by 0.3% last month. It took fell by 0.1% last May. The bottom line is that the year-over-year headline rate will soar well above 3% to reach its highest level in a decade, while the core rate will likely approach pre-pandemic levels (2.4% in February 2020).

The busy week begins off slowly with light economic calendars today in North America. The Canadian dollar has appreciated for the last five consecutive weeks against the US dollar. It has extended its gains today. The greenback slipped below CAD1.2100 today for the first time since September 2017 but has stabilized in the European morning. There is a $320 mln option struck there that expires today. There is little chart support until closer to CAD1.20. The CAD1.2150-level, which holds an expiring option for $425 mln, may offer initial resistance. The US dollar slumped by 1% against the Mexican peso before the weekend, its largest drop in over a month. It had begun the week around MXN20.24 and ended it below MXN19.92. So far today, the dollar is consolidating in a narrow range above the pre-weekend low (~MXN19.86). Last month’s low was set close to MXN19.7850, while the year’s low was set in late January by MXN19.55. The highlight for the week is Thursday’s central bank meeting. With inflation above 6%, Banxico cannot afford to resume the easing cycle that looks to have ended in February before price pressures accelerated.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-05-17

Update May 17 2021: SNB intervening. Sight Deposits have risen by +2.7 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +2.7 bn. compared to last week.

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

2021-05-12

The markets remain on edge. Asia Pacific and US equities have yet to find stable footing, and inflation fears are elevated. The foreign exchange market has turned quiet as the dollar consolidates its recent losses.

FX Daily, January 20: The Dollar Slips to New Lows against Sterling and the Mexican Peso

FX Daily, January 20: The Dollar Slips to New Lows against Sterling and the Mexican Peso

2021-01-20

Global equities are moving higher today. Led by continued strong buying of Hong Kong shares, the MSCI Asia Pacific Index rose to new highs. The Hang Seng is up 6% this year and is approaching the 2019 record high. Australia’s shares set a new record today. Japan and Taiwan bucked the trend.

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

2021-01-19

Overview: The animal spirits are on the march today. Equities are mostly higher, peripheral European bonds are firm, and the dollar is mostly softer. After posting the first back-to-back decline this year, the MSCI Asia Pacific Index bounced back today, led by a 2.7% gain in Hong Kong (20-month high) and a 2.6% rise in South Korea’s Kospi.

2021-01-15

The US dollar is firm against most of the major and emerging market currencies today. Among the majors, the Japanese yen and Swiss franc are resilient. For the week, sterling and the yen appear poised to eke out small gains, while the Scandi’s are the weakest performers with around a 1% decline.

FX Daily, January 11: Greenback Extends Recovery

FX Daily, January 11: Greenback Extends Recovery

2021-01-11

Julius Ceasar is said to have "crossed the Rubicon" on January 10, 49 BCE, taking the 13th Legion into Rome, defying orders from the Senate, and precipitating the Roman Civil Wat that marked the end of the republic and the birth of the empire.

FX Daily, January 08: Can the Dollar Find Traction Even if the Employment Data Disappoint?

FX Daily, January 08: Can the Dollar Find Traction Even if the Employment Data Disappoint?

2021-01-08

The global equity rally picked up this week as it closed in 2019. The MSCI Asia Pacific Index gained today and is up in nine of the past 10 sessions. It has fallen only in one week since the end of October. South Korea’s Kospi led today’s advance with a nearly 4% rally on the back of talks that were later played down between Hyundai and Apple.

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

2020-11-25

The global equity rally appears to be stalling after the US markets rallied strongly yesterday. Chinese, Taiwan, Korean, and Indian indices fell, and the MSCI Asia Pacific Index appears to have posted only its second loss this month. European shares are narrowly mixed, leaving the Dow Jones Stoxx 600 little changed.

Tags: #USD,China,Currency Movement,EUR/CHF,Featured,federal-reserve,Germany,jobs,newsletter,Olympics,U.K.,USD/CHF