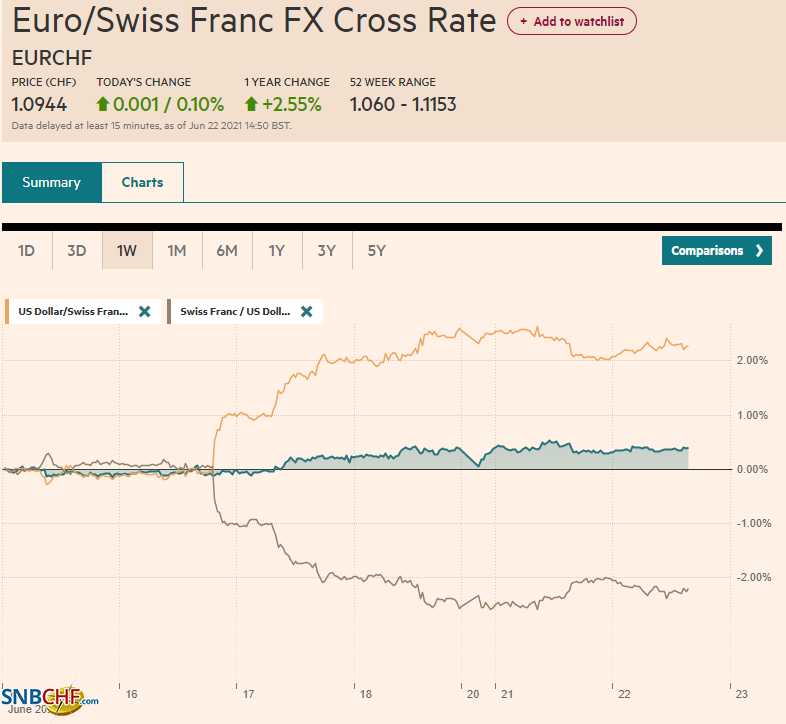

Swiss Franc The Euro has risen by 0.10% to 1.0944 EUR/CHF and USD/CHF, June 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Firming long-term US yields have lent the dollar support after trading heavily yesterday. The greenback is around 0.15%-0.50% higher against the major currencies. The Japanese yen and Canadian dollar are among the more resilient, and the Australian dollar and sterling among the heaviest. Emerging market currencies are mostly lower, except the South Korean won and Turkish lira. Even the Hungarian forint, where the central bank is widely expected to be the first EU country to lift rates today, is weaker. The US 10-year yield continues to recover from the drop to almost 1.35% early

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Czech, EUR/CHF, Featured, Federal Reserve, Hungary, Japan, newsletter, RBA, semiconductors, U.K., USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.10% to 1.0944 |

EUR/CHF and USD/CHF, June 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

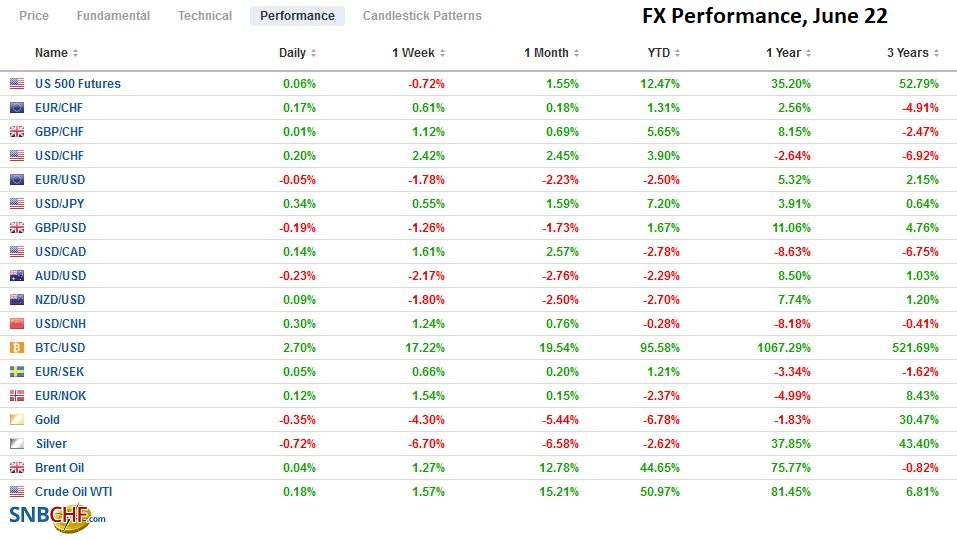

FX RatesOverview: Firming long-term US yields have lent the dollar support after trading heavily yesterday. The greenback is around 0.15%-0.50% higher against the major currencies. The Japanese yen and Canadian dollar are among the more resilient, and the Australian dollar and sterling among the heaviest. Emerging market currencies are mostly lower, except the South Korean won and Turkish lira. Even the Hungarian forint, where the central bank is widely expected to be the first EU country to lift rates today, is weaker. The US 10-year yield continues to recover from the drop to almost 1.35% early yesterday and appears capped near 1.50%. European yields are mostly softer, while Australia and New Zealand saw a seven basis point jump in the yield of their 10-year benchmarks. Asia Pacific equities responded strongly to yesterday’s rally in the US, led by a 3%+ gain in Tokyo and 1.5% in Australia. Japan’s shares gained the most in around 12-month after yesterday’s first purchases by the BOJ in a couple of months. Hong Kong and Singapore failed to participate in the recovery after Monday’s slide. Europe’s Dow Jones Stoxx 600 and US indices futures are trading lower. Commodities are sporting a weaker profile. Copper is paring yesterday’s gains. Iron ore fell 3.6% in Shanghai to bring this week’s loss to over 8%. Steel rebar has fallen by nearly 5% this week. Gold snapped a six-day drop yesterday with a 1% gain but stalled in front of $1800 and is trading heavier again today. August WTI initially extended yesterday’s 2.6% gain and reached $73.35, its highest level in nearly two years, before slipping back to around $72.50. |

FX Performance, June 22 - Click to enlarge |

Asia Pacific

A leading adviser to the Japanese government called for a JPY1 trillion (~$9 bln) investment in semiconductor chip development this fiscal year and more in the coming years to revive the national industry. The US, China, EU, South Korea, and Taiwan are all trying to strengthen their capacity. It is becoming, as the Japanese adviser said, as important as food and energy security. A new advanced fabrication facility costs more than $10 bln, according to some estimates. The US has earmarked a little more than $50 bln, while Taiwan’s TSMC alone has announced plans to invest $100 bln over the next three years. South Korea’s Samsung and Hynix are talking around $150 bln investment over the next decade.

Since last week’s stronger than expected jobs data, several observers now expect the Reserve Bank of Australia to temper its emergency policy next month. Some attribute this to yesterday’s drop in Australian bank shares, the most in a year, but the logic is elusive, and the beginning of the normalization of monetary policy is understood to be supportive of financial institutions. Indeed financials recovered today, rising 2%.

The dollar is at a three-day high around JPY110.50 near midday in Europe after staging an impressive recovery after falling to almost JPY109.70 yesterday. Last week’s highs in the JPY110.70-JPY110.80 area are the immediate target. It might take a push higher in the US yields to get lift the greenback above the JPY111.00. Initial support is in the JPY110.20-JPY110.30 area. Note that the dollar has fallen only once against the yen in the last eight sessions.

The Australian dollar remains confined to the pre-weekend range (~$0.7475-$0.7560). Some link the Aussie’s weakness to the drop in iron ore prices. Still, it is finding support just below $0.7500 in Europe. Initial resistance is seen near $0.7520 and then $0.7550.

The greenback edged higher against the Chinese yuan for the fourth consecutive session and the ninth day in the past 11. It is at its best level since early May (~CNY6.4745). The PBOC set the dollar’s fixing lower for the second consecutive session than the bank models in the Bloomberg survey anticipated (CNY6.4613 vs. CNY6.4626). Heavy bond issuance by local government and quarter-end demand tightened liquidity conditions in China and sent the overnight repo rate six basis points higher to 2.31%, bringing the cumulative increase to 44 bp over the past three sessions to its highest level in four months.

Europe

After striking the bilateral trade agreement with Australia earlier this month, the UK will formally apply to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership today. The UK had initially filed the request to join the bloc in February. The CPTPP covers about 15% of the world’s GDP. Reports suggest the UK is looking forward to opportunities to export autos, services, whiskey, and beef and lamb. In addition to Australia, the UK already has struck deals with seven of the bloc members.

Hungary is expected to become the first EU country to lift rates, followed by the Czech Republic tomorrow. Although expect a 30 bp hike to 90 bp, there is the risk of a larger move. The Deputy Governor spoke of “decisive action.” However, like many others, price pressures have risen before the economic strength has fully returned. Also, the central bank anticipates a stimulative budget next year ahead of elections. The one-week repo rate is at 75 bp. It is adjusted once a week on Thursdays and may be brought into line with the base rate that will be hiked today. The central bank may also phase out other stimulus measures. It appears the market is expecting about two hikes. The Czech Republic is expected to hike its key repo rate by 25 bp tomorrow to 50 bp. The market also has almost 50 bp of tightening discounted for H2.

The eurozone’s preliminary June PMI will be released tomorrow. While manufacturing may stabilize at elevated levels, the service sector is expected to have accelerated as the vaccination program has intensified. The composite is expected to rise to around 58.8 from 57.1. The UK’s flash PMI is expected to moderate slightly as the contagion increased and forced a postponement to the economy-wide re-opening into the middle of next month. The risk may be on the downside of the median forecast in the Bloomberg survey for 62.5 from 62.9 in May.

The euro finished yesterday near its high of around $1.1920 but has come back offered today. Last Friday and yesterday, the euro found bids near $1.1850. We suspect it may not have to return there to catch a bid today. We are looking at the $1.1870 area for a possible base.

Similarly, sterling, which mounted an impressive recovery yesterday from below $1.3790 to almost $1.3940 stalled, is testing the $1.3860 near midday in Europe. However, it too may find support near here, and a move back above $1.3900 would help stabilize the tone.

America

In prepared remarks for his appearance before the House Select Subcommittee on the Covid Crisis, Fed Chair Powell reiterates the view that once the supply imbalance is addressed, price pressures will ease. While Powell is unlikely to break new ground, his comments will help blunt the more hawkish comments of Bullard and Kaplan. Many think that the dot plots showed the fraying of the average inflation target regime, with 11 of the 18 Fed officials seeing two hikes in 2023 and seven anticipating a hike next year. Powell and the Fed’s leadership can be expected to push back and defend the approach.

The bipartisan effort to find a compromise on the infrastructure initiative may be drawing close. A key issue is how to pay for it, and President Biden has rejected the proposal to index the gasoline tax to inflation. Moreover, the compromise is for a $579 bln package, which pales in comparison with what Biden has proposed. One strategy that is being debated is to go do as much as the bipartisan effort will allow and then come back for the remainder using the reconciliation process. However, that would require the full support of all the Democrats in the Senate, which does not look possible. Separately, there appears to be growing concern that the Senate’s minimum global corporate tax will not be ratified.

The US reports May existing home sales today. They are expected to have fallen for the fourth consecutive month. The overall level remains elevated, but the pace has slowed. Some link it to the lack of supply of new homes as construction is delayed. Tomorrow, the US reports new home sales (a small increase is expected following a nearly 6% decline in April) and the flash PMI (which is expected to soften from strong levels). In addition to Powell’s testimony, regional presidents Mester and Daly will speak today. Canada and Mexico’s economic calendars are light ahead of tomorrow’s April retail sales reports.

The US dollar reversed lower against the Canadian dollar yesterday after reaching almost CAD1.2490. It fell to about CAD1.2355 but stabilized today. So far, it has been confined to a roughly CAD1.2360-CAD1.2395 range. The CAD1.2400-CAD1.2425 offers nearby resistance. A convincing break of CAD1.2350 could spur a test on CAD1.2300.

The greenback found support a little below MXN20.50 and appears to be carving out a new range. If the MXN20.40-MXN20.50 is the lower end of the new range, then the MXN20.70-MXN20.75 might be the upper end.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-21

Update June 21 2021: SNB intervening. Sight Deposits have risen by +1.1 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

2021-06-08

The capital markets appear to be in a holding pattern ahead of this week’s big events, including the US CPI and the ECB meeting. Equities are little changed but with a heavier bias evident. Most of the large bourses in the Asia Pacific region were lower, except Australia, which eked out a small gain.

FX Daily, June 02: The Dollar Snaps Back

FX Daily, June 02: The Dollar Snaps Back

2021-06-02

The US dollar is enjoying broad, even if not large, gains today following yesterday’s recovery from three-year lows against sterling and four-year lows against the Canadian dollar. The greenback is firmer against all the major currencies.

FX Daily, May 31: China Raises Reserve Requirement for FX, Stemming the Yuan’s Rise

FX Daily, May 31: China Raises Reserve Requirement for FX, Stemming the Yuan’s Rise

2021-05-31

US and UK markets are closed for holidays today, contributing to the rather subdued price action today. The MSCI Asia Pacific Index rallied two percent last week, the most in three months, and most markets began off the week with modest gains. Japan, Australia, and Singapore, for notable exceptions.

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

FX Daily, May 26: RBNZ Joins the Queue, while Yuan’s Advance Continues

2021-05-26

The decline in US rates and the doves at the ECB pushing back against the need to reduce bond purchases next month have seen European bond yields unwind most of this month’s gain. The inability of US shares to hold on to early gains yesterday did not deter the Asia Pacific and European equities from trading higher.

FX Daily, May 25: Softer Yields Weigh on the Greenback

FX Daily, May 25: Softer Yields Weigh on the Greenback

2021-05-25

The decline in US 10-year rates to two-week lows below 1.59% is helping rebuild bullish enthusiasm for stocks and weighing on the US dollar. The NASDAQ reached two-week highs yesterday, and almost all the large markets in the Asia Pacific region rose, though India struggled.

FX Daily, May 20: Market Stabilize after Yesterday’s Tumultuous Session

FX Daily, May 20: Market Stabilize after Yesterday’s Tumultuous Session

2021-05-20

US equity indices finished lower, but the real story was their recovery. Asia Pacific equities were mixed, with Australia’s 1.5% rally leading the recovery in some markets, including Tokyo and Singapore. Europe’s Dow Jones Stoxx 600 is up a little more than 0.5% near mid-session, led by information technology and industrials, while energy and financials lagged with small gains.

FX Daily, May 18: Risk Appetites Return Bigly

FX Daily, May 18: Risk Appetites Return Bigly

2021-05-18

In Asia, equities markets rallied strongly, led by the more than 5% gain in Taiwan, the most in over a year as Monday’s 3% drop was more than overcome. The Nikkei gained more than 2% despite the deeper than expected contraction in Q1 GDP. Hong Kong, South Korea, and India also rose more than a 1% gain as tech came roaring back.

Tags: #USD,Czech,EUR/CHF,Featured,federal-reserve,Hungary,Japan,newsletter,RBA,semiconductors,U.K.,USD/CHF