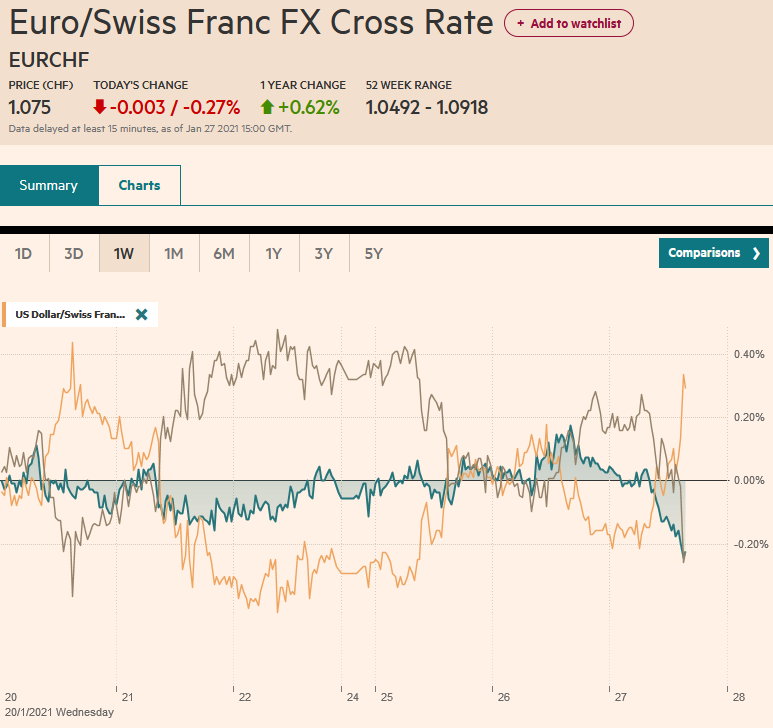

Swiss Franc The Euro has fallen by 0.27% to 1.075 EUR/CHF and USD/CHF, January 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Risk appetites seem subdued even if GameStop’s surge draws attention. Asia Pacific equities mostly slipped lower, and profit-taking was seen in Hong Kong and Seoul, which are off to an incredibly strong start to the year. Small gains were reported in Tokyo, Beijing, and Taipei. Europe’s Dow Jones Stoxx 600 opened lower but quickly recovered, with the help of the communications, real estate, and consumer discretionary sectors. US shares are a little heavy, but the NASDAQ futures are trading with a firmer bias. Apple, Facebook, Tesla, and Boeing are among the corporates reporting

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Australia, China, Currency Movement, currency war, EU, Featured, FOMC, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.27% to 1.075 |

EUR/CHF and USD/CHF, January 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

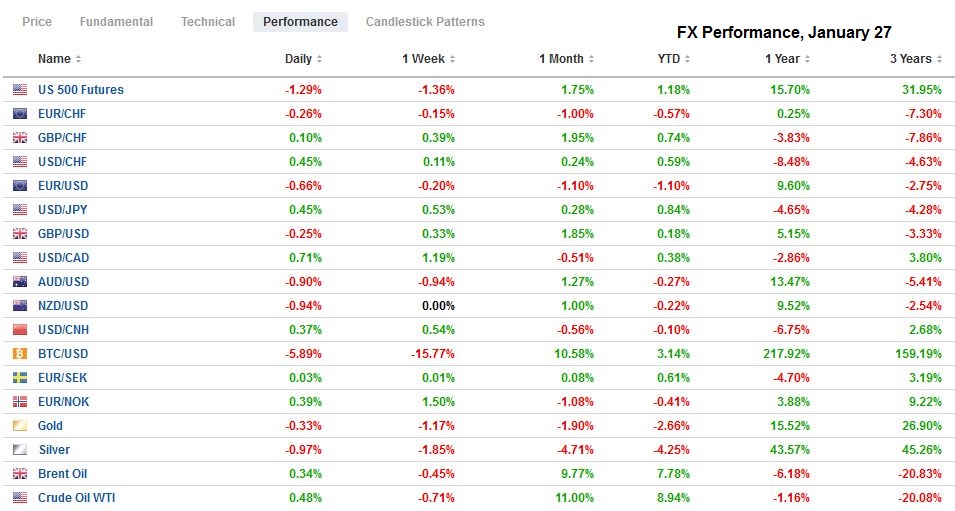

FX RatesOverview: Risk appetites seem subdued even if GameStop’s surge draws attention. Asia Pacific equities mostly slipped lower, and profit-taking was seen in Hong Kong and Seoul, which are off to an incredibly strong start to the year. Small gains were reported in Tokyo, Beijing, and Taipei. Europe’s Dow Jones Stoxx 600 opened lower but quickly recovered, with the help of the communications, real estate, and consumer discretionary sectors. US shares are a little heavy, but the NASDAQ futures are trading with a firmer bias. Apple, Facebook, Tesla, and Boeing are among the corporates reporting earnings today. Benchmark 10-year bonds are little changed, with the US Treasury yield around 1.04%. Italian bonds are firm despite the collapse of the government. The market’s confidence that this will be resolved without going to elections is behind the 13 bp decline in yields since the beginning of the week. The dollar is mostly firmer. The Scandis and Australian dollar are bearing the brunt and are off 0.3%-0.5% in late morning turnover in Europe. Although some of the Asian currencies are higher, the freely accessible currencies are mostly lower. Gold is straddling the 200-day moving average, a little below $1850. The yellow metal is taking a four-day losing streak into today, its longest slide since last April. A break of the $1840 level could signal a return to the $1800 area. March WTI is firm but in a narrow range around $53 a barrel. |

FX Performance, January 27 - Click to enlarge |

Asia Pacific

Australia’s Q4 20 CPI was softer than in Q3 but still above expectations. The headline CPI rose by 0.9% in the last three months of 2020, down from 1.6% in Q3, but a touch higher than the 0.7% forecast by the median response in the Bloomberg forecast. The year-over-year rate ticked up to 0.9% from 0.7%. The trimmed and weighted mean measures also edged higher. The figures do not change the outlook for policy. The RBA meets next week. Its forward guidance says no rate hike until inflation is sustainably in the 2-3% range. This will likely require stronger wage growth. It is also notable that tradable goods prices were off 0.4%, while non-tradable prices rose 1.5%, flattered by a hike in tobacco taxes.

China reported that the profits of its industrial firms rose by 20.1% in December. It was the seventh month of double-digit gains. Last year, profits increased by 4.1% to CNY6.5 trillion (~$1 trillion) after declining in 2019. Last year, profits at state-owned enterprises fell by 2.9% while rising by 3.1% in the private sector. Stronger production and exports helped lift profits, and producer prices edged higher in December for the first time since the start of the year. The steel sector bears watching. Rising iron ore prices have boosted input prices as demand weakens ahead of the Lunar New Year, and Beijing is trying to curb new capacity.

The dollar is in about a 20-tick range against the yen below JPY103.80. It has not been above JPY104 since last Tuesday and remains largely confined to last Friday’s range (~JPY103.50-JPY103.90). The Australian dollar posted an outside up-day yesterday, trading on both sides on Monday’s range and closing above its high. Initial follow-through buying lifted it to nearly $0.7765, a new three-day high, where it was greeted with fresh sales. Support was found in the European morning near $0.7720. A break of the $0.7670 area, yesterday’s low, to signal anything important. The PBOC set the dollar’s reference rate at CNY6.4665, which is a bit firmer than the median estimate from the bank models surveyed by Bloomberg (CNY6.4635). The PBOC money market operations have been exceptionally stingy as it drains liquidity. The overnight repo rate rose 23 bp to bring this week’s increase to 55 bp (now stands at 3%). The dollar continues to consolidate within the range set in the first two sessions of the year (~CNY6.43-CNY6.5150)

Europe

Less than a week before Biden was sworn in, the EU launched an initiative to promote the euro’s international use. The US was not cited by name, but the meaning was clear. As quoted in one media source: “The extraterritorial application of unilateral sanctions by third countries has seriously affected the EU’s and its member states’ ability to advance foreign policy objectives, to honor international agreements, and to manage bilateral relations with sanctioned countries. It continued: “At times, unilateral actions by third countries have compromised legitimate trade and investment of EU businesses with other countries.”

Yesterday, a few hours after Yellen was confirmed as the US Treasury Secretary, it was leaked to the media that the ECB is looking into the euro’s appreciation against the dollar since the pandemic with interest in whether it was the result of the different stimulus measures. At last week’s ECB meeting, it was noted that higher interest rates failed to lift the dollar. The euro may have slipped as the headline shot across screens, but the euro recovered as participants read the story. Perhaps, others concluded as we did that it is a process-oriented inquiry into the reaction function of markets. We have sketched out our dollar view here at the end of last year, including our anticipation for a corrective bounce this month.

Already some are claiming this is a shot in the forever currency war. It does not seem likely. However, as we have argued, what is clear is that the US proclivity to sanctions and weaponizing access to the dollar (not the price) encourages the search for alternatives. Europe has experienced the sanction regime as an encroachment on sovereignty. This is not about exchange rates. It is about reducing its dependence on the numeraire and looking for ways to offer financial leadership, such as green and social bonds. There have been thousands of books and dissertations written about what drives the foreign exchange market, and another one may be in the making. Moreover, the conclusions will have to be so tentative by definition that the policy impact cannot be significant. The timing of the leak does not appear planned or part of a broader strategy. However, one takeaway from the timing of both events is that Biden’s election is not a return to 2016, or earlier, for that matter. Europe is more assertive.

The euro recovered yesterday after recording a four-day low just below $1.2110. The bounce faded near $1.2175, as the euro put in a lower high for the second consecutive session. It stopped shy of its 20-day moving average (~$1.2180) and has not been above it for almost three weeks. A break of the $1.21 could signal a test on the year’s low near $1.2050. Ahead of the FOMC conclusion, where Chair Powell is expected to bat away attempts to bait him into the tapering “debate”, we suspect the euro can rise back toward the $1.2150 area. Sterling posted an outside up-day, like the Aussie, and follow-through buying lifted it to a new high (~$1.3760) and its best level since May 2018. It appears to be consolidating above $1.3720, and the range is particularly narrow (less than 40 pips). That said, the high of the day may not be in place.

AmericaThe FOMC meeting concludes today, and expectations are running low for any new policy announcements. Recall that last month, the Fed refined its forward guidance to say that the asset purchases will continue until substantial progress toward the policy goals. Other than that, the statement was nearly identical to the one that followed the November meeting. The economy is evolving broadly in line with Fed expectations, and the rollout of the vaccine supports a more optimistic medium-term view. Similarly, the $900 bln stimulus bill is clearly what Fed officials had in mind when they advocated fiscal support. Powell is unlikely to be sucked into a detailed comment on President Bident’s fiscal proposal. More important will be how the fiscal stimulus impacts the Fed’s view of the economy, and that may not be known until the updated forecasts in March. However, we do note that based on the stimulus already approved in large part, the IMF revised up US growth this year to 5.1% from 3.1%. It also suggested that the $1.9 trillion-proposal would lift the economy another 1.25% points this year and five percentage points over the next three years. The issue of the fiscal stimulus directly impacts “substantial progress” criteria. Powell may point to high levels of near-term uncertainty but has consistently recognized the dependence on the virus’s course and progress to combat it. With new mutations and the seemingly slow rollout, Powell is unlikely to get caught up in defining “substantial progress.” Ahead of the outcome of the FOMC meeting, the US reports December durable goods orders. Economists expect the orders to be mainly in line with November’s 1% headline gain. Excluding aircraft and defense orders, a 0.5% increase is expected, matching the previous month’s rise. It is unlikely to elicit a strong market response, not just due to the proximity of the FOMC, but tomorrow’s first look at Q4 GDP. A little better than 4% annualized growth is expected, down, of course, from the incredible 33.4% expansion in Q3 (after the implosion in Q2). |

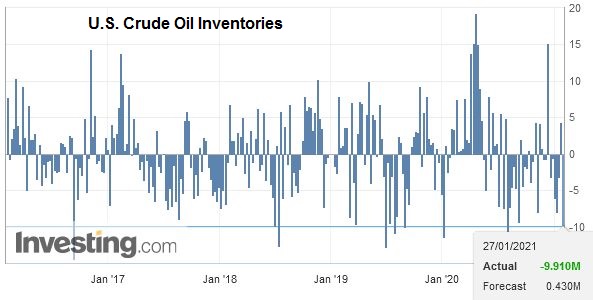

U.S. Crude Oil Inventories, January 27, 2021(see more posts on U.S. Crude Oil Inventories, ) Source: investing.com - Click to enlarge |

Canada and Mexico have light economic diaries today. The US dollar was rebuffed yesterday near CAD1.2780 and retreated to close on its lows just above Monday’s lows (~CAD1.2680). Despite the downside reversal, follow-through selling was minor, and the greenback is trading around CAD1.2720 in the European morning. Ahead of the FOMC outcome, we expect the US dollar to come off and possibly return toward the lows. Similarly, against the Mexican peso, its initial rally yesterday was reversed, and the greenback settled on its lows, a little below MXN20.00. Since bottoming on January 21 near MXN19.55, the greenback has been holding above the five-day moving average found near MXN19.97 today. Maybe an inside day is the most likely scenario (yesterday’s range ~MXN19.9350-MXN20.29)

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, December 17: Dollar Thumped

FX Daily, December 17: Dollar Thumped

2020-12-17

Overview: The prospects of a UK-EU deal and US stimulus continue to underwrite risk appetites and weigh on the dollar. Equity markets are moving higher. Led by Australia and China, the MSCI Asia Pacific Index rose to new record highs, while Dow Jones Stoxx 600 in Europe is at its best level since February.

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

2020-11-05

Overview: The markets did not wait for the final vote count and took stocks and bonds higher while pushing the greenback lower. While it appears Biden will be the next US President, investors seemed to like the fact that his agenda will be checked by a Senate that may remain in Republican hands. Stocks are on a tear.

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

2020-08-18

The NASDAQ rallied 1% yesterday to record highs as the Dow Industrials struggled, and the S&P 500 was able to eke out a small gain. The coattails were short, and the strength of the yen may have contributed to a 0.2% loss of the Nikkei. Still, its 6.2% advance this month is the best among the G10.

FX Daily, October 15: Markets Shake and Dollar Goes Bid

FX Daily, October 15: Markets Shake and Dollar Goes Bid

2020-10-15

A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off.

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

2020-11-09

The new week has begun with robust risk appetites, driving stocks and stocks higher and sending the dollar broadly lower. Nearly all the equity markets in the Asia Pacific region gained more than 1%, except Malaysia and Indonesia.

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

2020-11-13

Overview: The largest bourses in the Asia Pacific region followed the US equity market lower, with the Nikkei posting its first loss in nine sessions. China, Hong Kong, and Australia moved lower as well. On the week, the MSCI Asia Pacific Index gained about 1% after rising 6.3% in the prior week.

FX Daily, November 19: Surging Virus Saps Risk Appetites

FX Daily, November 19: Surging Virus Saps Risk Appetites

2020-11-19

Overview: News that the New York City was closing the schools to contain the virus sent stocks reeling in late North American dealings yesterday and spurred some profit-taking in the Asia Pacific and Europe. Equities in the Asia Pacific region were mostly lower, though China, South Korea, and Australia’s advanced and Tokyo markets were mixed.

FX Daily, January 22: Faltering Friday

FX Daily, January 22: Faltering Friday

2021-01-22

Fear that social restrictions may have to be broadened and extended is helping spur a wave of profit-taking and de-risking, which has also been encouraged by disappointingly high-frequency data. The equity rally seemed to falter a bit in the US, as the S&P 500 eked out a minor 0.03% gain yesterday.

Tags: #USD,Australia,China,Currency Movement,currency war,EU,Featured,FOMC,newsletter