Persistent risk-off impulses weighed on EM last week and that may continue this week. The Asian currencies outperformed last week while MXN, ZAR, and COP underperformed, and we expect these divergences to continue. Despite optimism about a stimulus package in the US, we think it remains a long shot. Meanwhile, virus numbers are rising in Europe and the US, with data from both regions likely to continue weakening. AMERICAS Mexico reports August trade Monday. A surplus of .03 bln is expected. Exports have fallen y/y since March but the larger collapse in imports has led the trade surplus to recover after an initial hit. Overall, the economy remains very weak and that is why we think the easing cycle may be extended into 2021. Banco de Mexico just cut rates 25 bp

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, emerging markets, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

![]() Persistent risk-off impulses weighed on EM last week and that may continue this week. The Asian currencies outperformed last week while MXN, ZAR, and COP underperformed, and we expect these divergences to continue. Despite optimism about a stimulus package in the US, we think it remains a long shot. Meanwhile, virus numbers are rising in Europe and the US, with data from both regions likely to continue weakening.

Persistent risk-off impulses weighed on EM last week and that may continue this week. The Asian currencies outperformed last week while MXN, ZAR, and COP underperformed, and we expect these divergences to continue. Despite optimism about a stimulus package in the US, we think it remains a long shot. Meanwhile, virus numbers are rising in Europe and the US, with data from both regions likely to continue weakening.

AMERICAS

Mexico reports August trade Monday. A surplus of $5.03 bln is expected. Exports have fallen y/y since March but the larger collapse in imports has led the trade surplus to recover after an initial hit. Overall, the economy remains very weak and that is why we think the easing cycle may be extended into 2021. Banco de Mexico just cut rates 25 bp to 4.25% last week, and consensus sees one more cut to 4.0% in Q4. Next policy meeting is November 12 another 25 bp cut is expected then.

Brazil reports central government budget data Tuesday. A primary deficit of -BRL101.2 bln is expected. Consolidated budget data will be reported Wednesday, where a primary deficit of -BRL97.7 bln is expected. September trade data will be reported Thursday. August IP will be reported Friday and is expected to fall -0.5% y/y vs. -3.0% in July. The economy is starting to pick up more but overall remains quite weak. No wonder the central bank issued its new dovish forward guidance. Consensus sees the tightening cycle beginning in Q2 2021 but we think it will much later than that. Next policy meeting is October 28 and no change is expected then.

EUROPE/MIDDLE EAST/AFRICA

South Africa reports Q2 unemployment Tuesday. It is expected to rise to a record high 34.8% from 30.1% in Q1. August CPI, trade, budget, money, and loan data will all be reported Wednesday. Headline inflation is expected to fall a tick to 3.1% y/y. If so, it would be near the bottom of the 3-6% target range. Next policy meeting is November 19 and no change is expected then. However, with the economy still very weak, we see some chance of a dovish surprise then. Much will depend on the external environment and how the rand is trading.

Turkey reports August trade data Wednesday. A deficit of -$6.3 bln is expected vs. -$2.7 bln in July. If so, the 12-month total would rise to -$34 bln, the highest since January 2019. After the surprise hike Thursday, the central bank continued to tighten conditions by accepting a very low amount of bids at the new 10.25%, forcing banks to go to more expensive options and boosting the average cost of funds to 10.88%. Yet the lira has already given up most of its post-hike gains and so further backdoor tightening is likely. Next policy meeting is October 22 and another policy hike is possible then if the lira continues to weaken.

Poland reports September CPI Thursday. Headline inflation is expected to rise a tick to 3.0% y/y. If so, it would remain in the upper half of the 1.5-3.5% target range. Next policy meeting is October 7 and no change is expected then. The bank has kept rates on hold at 0.10% since its last 40 bp cut in May. It has signaled rates will remain low for the foreseeable future.

ASIA

Korea reports August IP Tuesday. It is expected to contract -3.0% y/y vs. -2.5% in July. September trade will be reported Thursday, with exports expected to rise 4.4% y/y vs. -10.1% in August and imports expected to fall -4.9% y/y vs. -15.8% in August. Korea is shaping up to be one of the stronger economies in the region, helped by the recovery in China was well as the weak won relative to the yen. Next policy meeting is October 14 and no change is expected then.

China reports official September PMIs Wednesday. Manufacturing is expected at 51.3 vs. 51.0 in August, while non-manufacturing is expected at 54.6 vs. 55.2 in August. Caixin also reports its manufacturing PMI that day and it is expected to remain steady at 53.1. Between the combination of a solid economic recovery and the entry of China bonds into the FTSE Russell benchmark index, inflows are likely to remain strong and should keep the yuan relatively firm.

Hong Kong reports August retail sales Wednesday. Despite the weak economy, inflows have kept the Hong Kong dollar pinned to the strong end of the 7.75-7.85 trading band for most of August and September after a brief move off it in mid-July. Continual selling of HKD by the HKMA to maintain the band has boosted local liquidity and pushed interbank rates lower. Yet the recent decision by FTSE Russell to include the mainland bond market in its benchmark index suggests HK inflows will remain strong. We see no change to the HKD peg for the foreseeable future.

Indonesia reports September CPI Thursday. Headline inflation is expected to slow to 1.30% y/y from 1.32% in August. If so, it would remain below the 2-4% target range. Yet despite low price pressures, the bank left rates unchanged at its last two meetings August 19 and September 17. Next policy meeting is October 13 and no change is expected then if the rupiah remains under pressure.

Reserve Bank of India meets Thursday and is expected to keep the repo rate steady at 4.0%. CPI rose 6.7% y/y in August, down from the 7.22% peak in April but still above the 2-6% target range. Due to high inflation, the RBI unexpectedly left rates unchanged at its last meeting August 6. We see a small chance of a dovish surprise this week if the rupee remains relatively firm.

Philippine central bank meets Thursday and is expected to keep rates steady at 2.25%. CPI rose 2.4% y/y in August, the lowest since May and in the bottom half of the 2-4% target range. Yet despite low price pressures, the bank left rates unchanged at its last meeting August 20. We see a small chance of a dovish surprise this week if the peso remains relatively firm.

You Might Also Like

Risk assets remain hostage to swings in market sentiment. Stronger than expected US jobs data last week was welcome news. However, the tug of war between improving economic data and worsening viral numbers is likely to continue this week, with many US states reporting record high infection rates.

This is likely to be one of the most eventful weeks we’ve had in a while. Not only do three major central banks meet, but four EM central banks also meet, and we get important June and July data from the US, the first Q2 GDP reading from China, an OPEC+ meeting, and an EU summit.

EM FX was mixed last week, with most risk assets continuing to fight a tug of war between improving economic data and worsening virus numbers. Sentiment may be hurt early this week over lack of consensus in the EU and the US regarding further fiscal stimulus. Three of the four EM central banks meeting this week are expected to cut rates.

EM currencies took advantage of broad dollar weakness against the majors last week, with most gaining against the greenback. Yet the week ended on a bit of a risk-off note as concerns intensified about the resurgent virus and the impact on the still-weak global economy.

The dollar got some traction against the majors towards the end of last week. This weighed on EM FX, with the high best currencies TRY, BRL, CLP, and ZAR leading the losers. We downplay risk of contagion from Turkey, but we acknowledge it will keep investors wary of the countries with poor fundamentals.

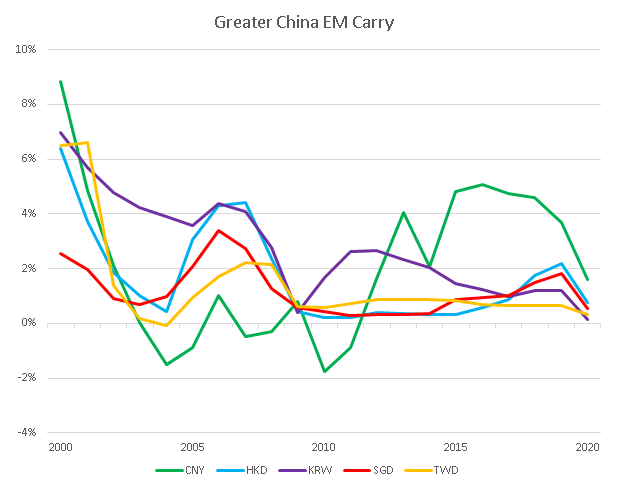

Where Has All the Carry Gone?

Where Has All the Carry Gone?

Despite broad-based dollar weakness, EM currencies have not fully participated in the risk on environment that’s now in place. The good news is that fundamentals matter again. The bad news is that there are a lot of EM countries with bad fundamentals, and the secular decline in carry no longer gives these weaklings any cover.

EM performance this week will hinge crucially on whether US equity markets can find some traction. If sustained, last week’s equity rout could lead to a deeper generalized risk-off trading environment this week that would weigh on EM FX and equities.

Our Latest Thoughts on the Dollar

Our Latest Thoughts on the Dollar

The dollar remains under pressure, due in large part to the Fed’s aggressive efforts to inject stimulus. We see dollar weakness persisting near-term. From a longer-term perspective, we note that the greenback remains largely rangebound and is unlikely to fall below its 2018 lows.

Tags: Articles,Emerging Markets,Featured,newsletter