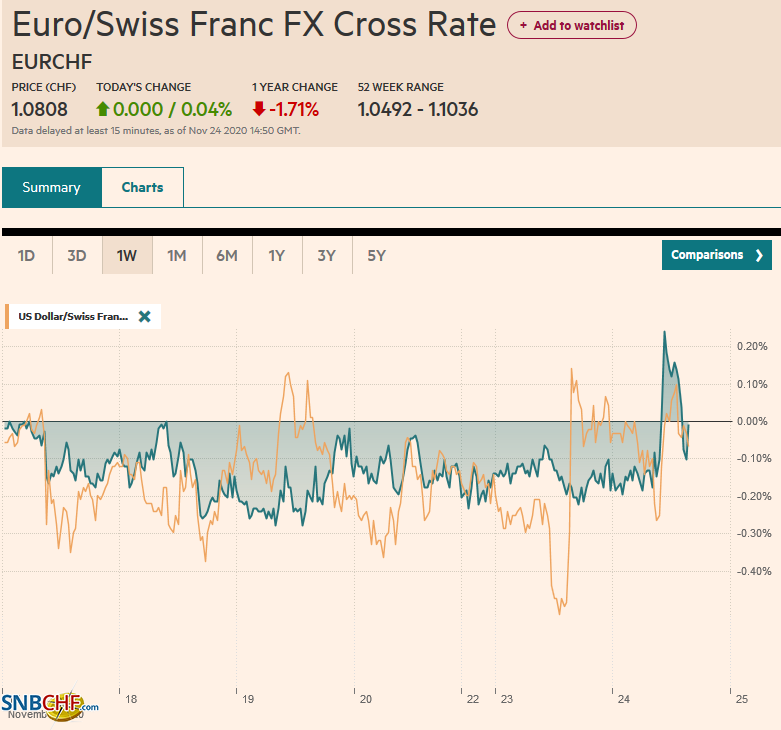

Swiss Franc The Euro has risen by 0.04% to 1.0808 EUR/CHF and USD/CHF, November 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The contrast between the eurozone and US preliminary PMI readings caught the short-term market leaning the wrong way, and the dollar snapped back after extending its recent losses. However, today the US dollar is back on its heels and returning to yesterday’s lows against most major currencies. The dollar bloc and Scandis lead the charge, while the Swiss franc and yen, gaining about 0.3%, are the laggards. Emerging market currencies are also mostly stronger, and the JP Morgan Emerging Market Currency Index is stabilizing after yesterday’s 0.5% decline, the largest of the month.

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brazil, Brexit, China, Currency Movement, Featured, newsletter, Peru, Politics, Turkey, USD

This could be interesting, too:

Investec writes The Swiss houses that must be demolished

Claudio Grass writes The Case Against Fordism

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Swiss FrancThe Euro has risen by 0.04% to 1.0808 |

EUR/CHF and USD/CHF, November 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

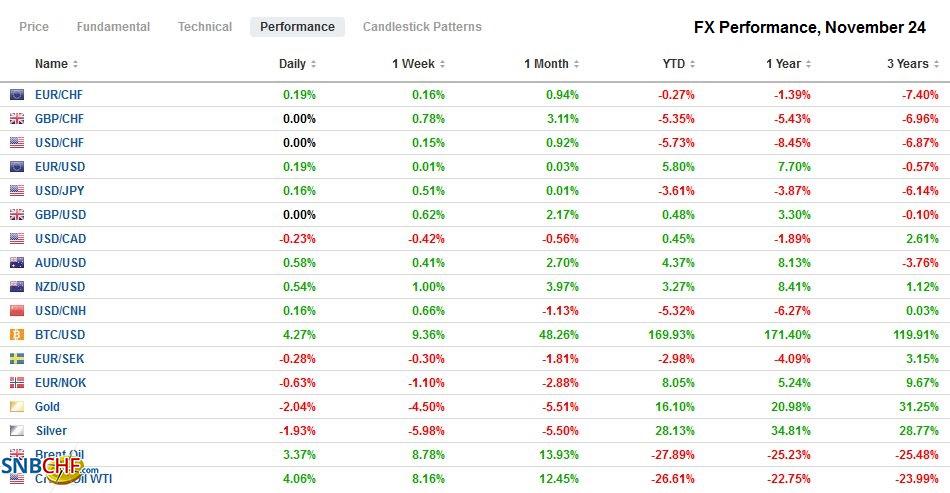

FX RatesOverview: The contrast between the eurozone and US preliminary PMI readings caught the short-term market leaning the wrong way, and the dollar snapped back after extending its recent losses. However, today the US dollar is back on its heels and returning to yesterday’s lows against most major currencies. The dollar bloc and Scandis lead the charge, while the Swiss franc and yen, gaining about 0.3%, are the laggards. Emerging market currencies are also mostly stronger, and the JP Morgan Emerging Market Currency Index is stabilizing after yesterday’s 0.5% decline, the largest of the month. Despite Turkey abolishing rule that required banks to extend credit and buy government debt, the Turkish lira is a notable exception. It has been sold, seemingly led by local names, and the dollar probed TRY8.0. After yesterday’s holiday, Japanese markets reopened and played a little catch-up, gaining 2% to lead the Asia Pacific region. Chinese and Taiwanese shares fell. European bourses are higher, and the Dow Jones Stoxx 600 is up around 0.6% in late morning turnover. The S&P 500 and Dow Jones Industrials are poised to gap higher at the US opening. Core bond yields are slightly firmer, leaving the US 10-year benchmark near 0.86%. Peripheral European yields are a little softer. Gold’s slump continues. It is lower for the sixth session of the past seven and tested $1810, a four-month low. Oil is moving in the opposite direction and the January WTI contract pushed into the $43.50-$43.75 area to reach a new 2.5-month high. |

FX Performance, November 24 - Click to enlarge |

Asia Pacific

Reports suggest China has dramatically stepped up its purchases of agricultural products. Its corn imports from the US last month look to be the second-highest on record and twice last year’s pace, more than a million tons for the third consecutive month. Imports of wheat, barley, sugar, and pork are also running near twice the year-ago pace. Soy is also in strong demand, and the risk of that dry weather lowers the Brazilian crop and helps lift prices that reached six-year highs yesterday. At $12 a bushel, soy has gained 45% since mid-March. The CRB Index is at new eight-month highs. The Chinese yuan has appreciated by about 3% since the end of September, cushioning the CRB’s 6% gain.

The Trump Administration is reportedly still considering executive action that would sanction more Chinese companies, and some link the decline of Chinese shares to such speculation. Separately, but not completely unrelated, the UK appears to be moving closer to formalizing its ban on the installation of new Huawei equipment and to order replacing existing equipment by 2027. Australia’s Prime Minister Morrison tried to strike a more conciliatory note to Beijing, which is taking out its displeasure over Canberra’s policy in limiting trade in a number of areas. However, Morrison’s claim of reluctance to take sides in the US-China competition rings hollow. Australia is a member of the Quad, which seeks to check China’s rise in the region, for example. Australia has made its choice. On the other hand, Yellen, who has been tipped as the next Treasury Secretary, does not accept what has become a seemingly popular charge in the US that China is responsible for the US worldwide deficit. Although it is a common thread in American political commentary to blame others for its challenges, the global imbalance pre-dates China’s rise. Some used to make the same charge against Japan, and these days, Japan runs a trade deficit, and the US trade shortfall is larger than ever.

Several Asian countries, including South Korea, Thailand, and Japan, have complained or warned against their currencies’ strength. There has been a general reprieve in recent days as the dollar moved off its lows and consolidated. Off a base around JPY103.65, the greenback bounced to about JPY104.65 yesterday, a five-day high and the (50%) retracement of the recent decline from the JPY105.70-area. Support today is seen near JPY104.00. The Australian dollar was pushed back after its nemesis at $0.7340 held yesterday, but with a running start today, it jumped to $0.7370 in early European turnover. The year’s high was set on September 1 near $0.7415. The New Zealand dollar tested $0.7000 for the first time since May 2018. A call by parliament for the central bank to take property prices into account in setting monetary policy is seen as another factor reducing the chances of negative rates. The PBOC set the dollar’s reference rate at CNY6.5809, nearly spot-on expectations. Several state-owned enterprises have defaulted over the past couple of weeks, and this is making local investors more nervous and appears to be tightening money market conditions faster than the PBOC is countering. The dollar appears to be consolidating between CNY6.55 and CNY6.60.

Europe

Sterling did not seem to react adversely to signs that another deadline was slipping past for the UK to secure a new trade agreement with the EU. Sterling’s pullback after nearing $1.34 was a function of the dollar’s recovery. The euro remained pinned below GBP0.8900 was previously offered support and now has morphed into resistance. Participants remain hopeful that a deal does emerge and recognize several legal maneuvers that the EU can undertake to expedite the ratification process. As we noted, the UK’s chief negotiator Barnier suggested he is prepared for the talked to carry over into December. That said, assessments like 95% of a deal have been reached is simply meaningless. First, nothing is agreed until everything is. Second, the more difficult issues are naturally resolved last. Third, if there are 60 elements of the agreement, to be 95% complete means three issues (state aid, fishing rights, and conflict resolution mechanism) remain.

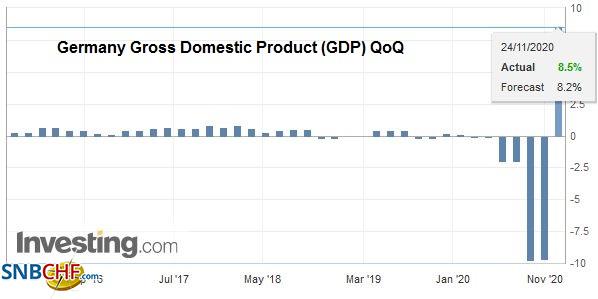

| Germany revised Q3 GDP to show a quarterly increase of 8.5% rather than 8.2%, fueled by stronger consumption. While the revision is positive, it is a bit dated, and many worry about the stagnation or worse this quarter. |

Germany Gross Domestic Product (GDP) QoQ, Q3 2020(see more posts on Germany Gross Domestic Product, ) Source: investing.com - Click to enlarge |

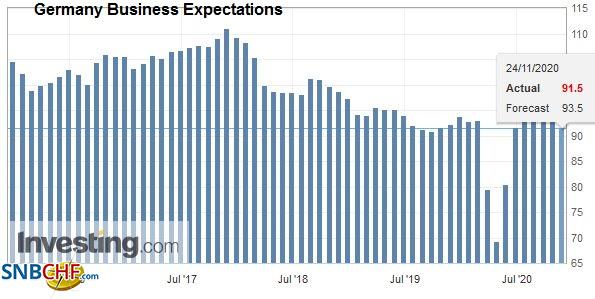

| While the expectations component fell more than expected (to 93 from 95), the current assessment held in better and was little changed (90.0 vs. 90.3). |

Germany Business Expectations, November 2020(see more posts on Germany Business Expectations, ) Source: investing.com - Click to enlarge |

| Separately, the November IFO softened, but the overall assessment of the investment climate did not weaken as much as feared. It fell to 90.7 from a revised 92.5 (initially 92.7). |

Germany Ifo Business Climate Index, November 2020(see more posts on Germany IFO Business Climate Index, ) Source: investing.com - Click to enlarge |

The euro had its biggest range in two weeks yesterday. It first pushed above $1.19 and sold-off quickly after the US better than expected preliminary PMI that underscored the divergence between the US and Europe here in Q4. European social restrictions are more severe than in the US, and the latter’s better economic performance comes at a high cost in terms of lives and the pandemic. The euro has recovered to almost $1.19 in late-Asia/early Europe, but the intraday technicals are stretched, and caution against playing for the breakout. Sterling was turned back from approaching $1.34 yesterday and found support near $1.3265. It has returned to $1.3380 today before stalling. Initial support is seen around $1.3320. The euro slumped to GBP0.8865 yesterday and has stabilized today, trading within yesterday’s range.

America

After much delay, President Trump, without conceding defeat, authorized his administration to begin the transition process. The move comes after senior party members urged the president to accept that his legal recourses were exhausted and after Biden’s new nominations were leaked to the press. It is important for the political process, ensuring the new administration is prepared, that adversaries do not sense a vacuum, and that the coordination of the response to the pandemic can begin. Biden is expected to formally announce several nominations later today. The president-elect appears to be surrounding himself with many familiar faces from the Obama administration. The leaks seem to lend credence to the view that Biden will seek to govern from the middle, and it would not be surprising if at least one Republican was offered a cabinet post.

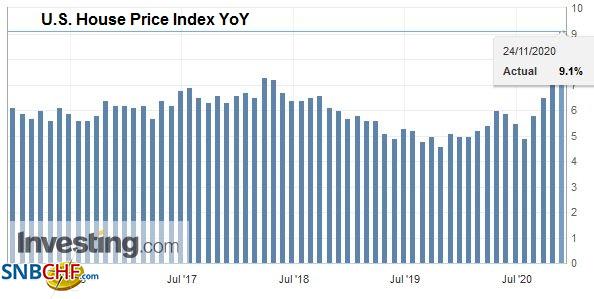

| The US political agenda trumps the economic diary today. September house prices and the Conference Board’s preliminary November consumer confidence report are on tap. The Richmond Fed’s Manufacturing survey results are also due. The regional Fed surveys are mixed so far. The Empire surprised on the upside, while Philadelphia’s was softer than expected, the Kansas City Fed’s slightly lower but in line with forecasts. Mexico reported October unemployment figures (expected to slip to 5.0% from 5.1%). More interesting will be the biweekly inflation report that could see the year-over-year CPI eased to 3.6% from above 4.0%, which would be the lowest since mid-year and open the door to a small rate cut by Banxico either next month or early next year. In contrast, Brazil reported IBGE inflation, and it is expected to have risen above 4% for the first time since February. |

U.S. House Price Index YoY, September 2020(see more posts on U.S. House Price Index, ) Source: investing.com - Click to enlarge |

It seems like a bold move. Amid a political crisis that has seen three different presidents in a fortnight, Peru has issued three bonds to raise $4 bln, including a 100-year obligation. In addition to the century bond, Peru also issued a 12- and 40-year bond. The former was sold at 100 bp on top of US Treasuries. Peru has a solid credit rating (BBB+ by Fitch and S&P, and the equivalent of A- by Moody’s). A week ago, the Peruvian sol touch a record low. It is off by around 8% this year against the dollar and is flat this quarter. Peru’s shutdown had been among the most severe in the region, based on cell phone data collected by Google, according to press reports. The economy bounced back in a big way in Q3 and expanded by nearly 30% quarter-over-quarter contracted by about the same in Q2. The government has enacted among the largest stimulus programs estimated to be about 20% of GDP.

Rising equities and commodity prices lifted the Canadian dollar today. The greenback spiked to almost CAD1.30 in late Asian activity before rebounding to CAD1.3040 in Europe. There is scope for CAD1.3060 or so. Recall that earlier this month, the US dollar recorded the low for the year near CAD1.2930. The greenback recovered smartly after falling to a new nine-month low yesterday against the Mexican peso (~MXN19.9480), but new sellers capped it near MXN20.18. It remains within yesterday’s range and has thus far remained above MXN20.00, albeit barely. Initial resistance is seen near MXN20.10 now.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, August 5: Corrective Pressures in the FX Market Prove Short-Lived

FX Daily, August 5: Corrective Pressures in the FX Market Prove Short-Lived

The drop in US yields to new lows amid paralysis in Washington, except apparently over a lip-syncing app’s threat to US national security, sent the dollar back to its lows after a modest recovery in early North American trading yesterday.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

A flurry of deals, including the still-evolving Oracle-TikTok tie-up, helped lift equity markets in the Asia Pacific region. South Korea’s Kospi, and Indonesia, which had been battered last week, led the advance. The MSCI Asia Pacific Index rose for the third consecutive sessions. European bourses are little changed while US stocks are firmer.

FX Daily, November 19: Surging Virus Saps Risk Appetites

FX Daily, November 19: Surging Virus Saps Risk Appetites

Overview: News that the New York City was closing the schools to contain the virus sent stocks reeling in late North American dealings yesterday and spurred some profit-taking in the Asia Pacific and Europe. Equities in the Asia Pacific region were mostly lower, though China, South Korea, and Australia’s advanced and Tokyo markets were mixed.

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs.

FX Daily, August 10: Monday in August

FX Daily, August 10: Monday in August

Overview: The new week has begun slowly with Singapore and Tokyo markets closed for national holidays. The MSCI Asia Pacific Index rose 2% last week and edged higher today, led by 1.5%-1.7% rallies in South Korea and Australia. Hong Kong was a notable exception and eased around 0.6%.

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

The NASDAQ rallied 1% yesterday to record highs as the Dow Industrials struggled, and the S&P 500 was able to eke out a small gain. The coattails were short, and the strength of the yen may have contributed to a 0.2% loss of the Nikkei. Still, its 6.2% advance this month is the best among the G10.

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

Overview: The S&P 500 and NASDAQ set new all-time highs yesterday, but the continued outperformance of US equities have failed to lend the dollar much support. It was sold to new lows for the year yesterday against the euro, sterling, the Swedish krona, and the Australian dollar.

Tags: #USD,Brazil,Brexit,China,Currency Movement,Featured,newsletter,Peru,Politics,Turkey