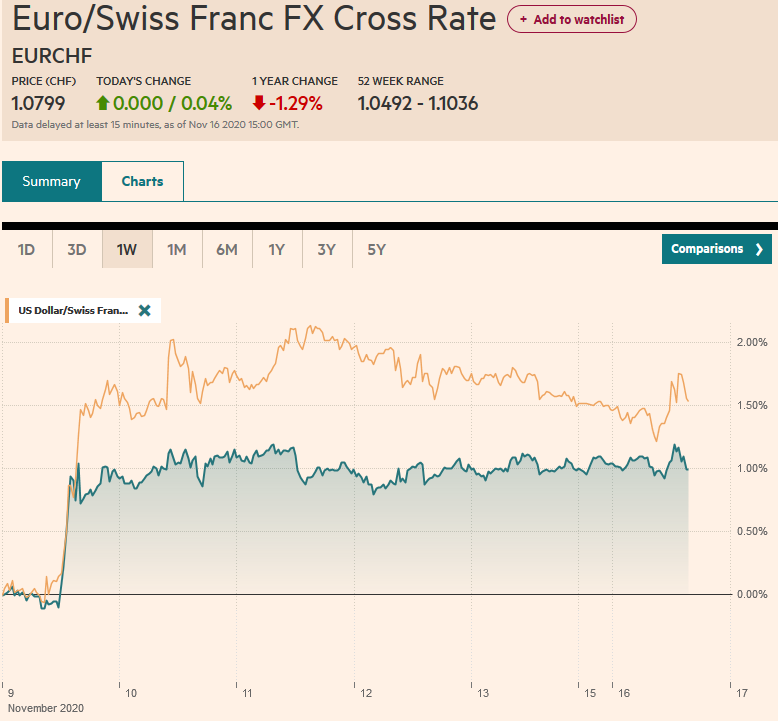

Swiss Franc The Euro has risen by 0.04% to 1.0799 EUR/CHF and USD/CHF, November 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Despite the surging pandemic and new restriction measure, risk-appetites appear strong to start the week. Led by 2% gains in the Nikkei and Taiwan’s Taiex, all of the Asia Pacific region’s equity markets advanced. European markets have followed suit and the Dow Jones Stoxx 600 is knocking on last week’s eight-month high. US shares are firmer, and the S&P 500 could gap higher at the open. Bonds are firm, and the US 10-year yield is a little softer at 0.88%. European yields are 1-3 bp lower. The greenback is trading heavier, with the Scandis and Antipodeans leading the majors.

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, ASEAN, Brexit, China, Currency Movement, Featured, Japan, newsletter, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.04% to 1.0799 |

EUR/CHF and USD/CHF, November 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Despite the surging pandemic and new restriction measure, risk-appetites appear strong to start the week. Led by 2% gains in the Nikkei and Taiwan’s Taiex, all of the Asia Pacific region’s equity markets advanced. European markets have followed suit and the Dow Jones Stoxx 600 is knocking on last week’s eight-month high. US shares are firmer, and the S&P 500 could gap higher at the open. Bonds are firm, and the US 10-year yield is a little softer at 0.88%. European yields are 1-3 bp lower. The greenback is trading heavier, with the Scandis and Antipodeans leading the majors. Sterling is struggling. Most emerging market currencies are trading higher, though the Turkish lira is an exception and sees last week’s strong gains pared (-1.25%). Gold is firm but holding just below $1900. Silver is up for a fifth consecutive session and is straddling $25. Oil is higher, with December WTI near $41 after rallying more than 11% over the past two weeks. Copper traded at a two-year high, encouraged by China’s industrial output. |

FX Performance, November 16 - Click to enlarge |

Asia PacificFifteen Asia Pacific countries signed a free-trade pact, the Regional Comprehensive Economic Partnership, over the weekend. It marries the 10 ASEAN countries with China, Japan, South Korea, Australia, and New Zealand. It includes nearly a third of the world’s GDP and population. The next step is the national ratification process. It was initially intended to be Beijing’s answer to the US-led Trans-Pacific Partnership, which crystallized the Obama Administration’s Asia pivot and a way to modernize NAFTA. Still, when President Trump formally withdrew from the TPP, he noted that both Clinton and Sanders were opposed to the pact too. Some dismiss this and claim that this was simply pre-election posturing by Clinton, though we will never know, and surely words matter. There is some handwringing about how Beijing is outflanking the US, and it plays into the thinking in some quarters that China is eclipsing the US. Yet, be careful about projecting broader significance. The RECP will not offset the tensions in the South China Sea. |

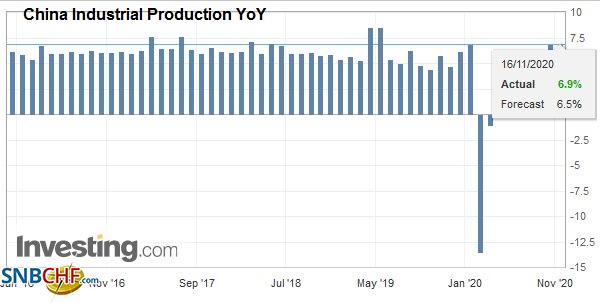

China Industrial Production YoY, October 2020(see more posts on China Industrial Production, ) Source: investing.com - Click to enlarge |

| It will not alter the wider security cooperation between the US, Japan, South Korea, Australia, and New Zealand. Australia will offer the first test of this hypothesis. Several of its exports to China have been blocked as Beijing expresses its disapproval of Canberra’s criticism and apparently closer ties with the US. India pulled out of the RCEP talks last year, and its tensions with China have escalated this year. Often what it looks like on paper is quite different in practice. Recall the Chiang Mai Initiative, the regional currency swap agreement (ASEAN and China, Japan, and South Korea), launched in 2010, that was heralded as an alternative to the IMF, has not been used. China launched the Asian Infrastructure Investment Bank (2104) to rival the World Bank and IMF and promote the yuan’s internationalization. Yet, its subscriptions and loans are primarily in US dollars.

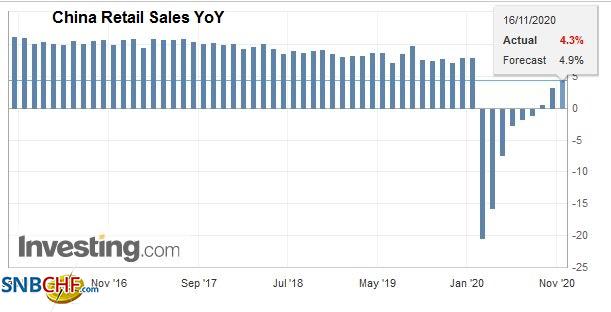

There are two developments in China to note. First, the October data showed the recovery remains intact. Industrial output matched September’s gain of 6.9%, while retail sales for by 4.3% after posting a 3.3% rise in September. |

China Retail Sales YoY, October 2020(see more posts on China Retail Sales, ) Source: investing.com - Click to enlarge |

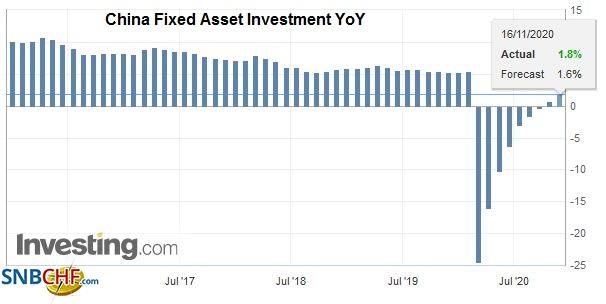

| Fixed asset investment rose by 1.8% after rising 0.8%, and the surveyed jobless rate slipped to 5.3% from 5.4%. There was an extended holiday in early October, which may have dampened some activity. Second, the PBOC’s money market operations were closely watched, and it did not disappoint. The CNY800 bln injection via the Medium-Term Lending Facility more than covers the CNY600 bln coming due this month at an unchanged rate of 2.95%. |

China Fixed Asset Investment YoY, October 2020(see more posts on China Fixed Asset Investment, ) Source: investing.com - Click to enlarge |

| Japan’s Q3 GDP expanded by 5%, a bit better than expected, and is the first quarterly growth in a year. After the Q3, the world’s third-largest economy is about 6% smaller than a year ago. While consumption rose 4.7% after falling 8.1% in Q2, business spending disappointed, falling by 3.4% after a 4.5% decline in Q2. Prime Minister Suga has formally begun drafting a third supplemental budget for JPY10 trillion (~$96 bln). |

Japan Gross Domestic Product (GDP) YoY, Q3 2020(see more posts on Japan Gross Domestic Product, ) Source: investing.com - Click to enlarge |

The dollar continued to retrace last Monday’s sharp gains on the back of the Pfizer new. It peaked in the middle of last week, a little shy of JPY105.70. Today, it reached a five-day low near JPY104.35. It is the first day since November 6 that the greenback has been unable to trade above JPY105.00. Resistance is now pegged near JPY104.70, where an option for almost $490 mln will expire today. The Australian dollar is firm, but it is struggling to re-establish a foothold above $0.7300. If it falters, it could signal a retreat on the lows from the second half of last week near $0.7225. The PBOC set the dollar’s reference rate at CNY6.6048, in line with expectations. Still, the dollar traded below the ranges seen last week and is approaching last week’s spike low near CNY.5640.

Europe

The departure of Cummings, the key strategist in Prime Minister Johnson’s government, comes as the UK faces challenges on several fronts. The virus is out of control. The economy is believed to be contracting again after rebounding in Q3. The UK-EU trade talks are dragging on past the middle of November (European Council meeting of the heads of state is November 21-22). There have been a couple of embarrassing and disturbing leaks recently, including the Bank of England’s recent decision. While there is speculation the Cummings will take vengeance, Johnson would seem freer to change the government’s position. Johnson was expected to launch several new initiatives this week, including a green infrastructure initiative. Still, given his contact with an infected person, he has had to move into self-isolation.

The euro rose steadily through the Asia Pacific session to reach a five-day high near $1.1870. It has been sold in the European morning, pushing it back to around $1.1835. A close below $1.1850 today could signal further near-term losses. An option for 2 bln euros that is struck there expires tomorrow. Recall last week’s low was a little below $1.1750. The Bundesbank acknowledged what many have suspected, namely that the German economy could stagnate or shrink here in Q4. Sterling initially rose above $1.3235 to meet the (61.8%) retracement of last week’s decline from the November 11 high around $1.3310. Like the euro, it was greeted with selling in European turnover and found support near $1.3165. A close above $1.3200 would be constructive. The euro found support ahead of GBP0.8950 and needs to resurface above GBP0.9000 to take the pressure off.

America

President Trump has yet to acknowledge his defeat, and it is still two months before Biden is to take office. Nevertheless, the president-elect has sent two important foreign policy signals. Reports suggest that he reminded the UK Prime Minister that the US was a guarantor of the Good Friday Agreement and underscored the importance of avoiding a hard border between the Irish Republic and Northern Ireland. According to separate reports, Biden also reiterated Obama’s 2014 acknowledgment that the US security guarantee covered the Senkaku Islands, administered by Japan but claimed by China. Trump never confirmed its commitment, and China has repeatedly probed the airspace and waters, making it an obvious potential flashpoint. In doing so, Biden also confirms the willingness to work with traditional allies to counter China.

There are three highlights for the US today. First is the data. The Empire Manufacturing Survey, the first look at this month’s activity, is on tap. A small gain is expected. Second, around 1:45 pm ET today, Biden and Harris will hold a press conference to discuss their economic plans. Both have advocated additional stimulus. Third, two Fed officials (San Fran President Daly and Vice-Chair Clarida speak. Tomorrow the US reports October retail sales (a sold gain of around 0.5% is expected), and on Wednesday, October industrial output figures are released. Also, at midweek, the Senate is thought likely to vote on Shelton’s controversial nomination to the Federal Reserve.

Canada reports manufacturing sales (September) and existing home sales (October), but the highlight of the week is the CPI (October) in the middle of the week and retail sales (September) ahead of the weekend. Mexico has a light calendar this week. The main feature is tomorrow’s employment report. Recall the central bank stood pat last week, defying expectations of a rate cut. The large trade surplus in recent months (domestic demand compression), strong worker remittances, and the attractiveness of its relatively high nominal rates (~4.2%-4.4% on bills-cetes) have been underpinning the peso.

After starting last week at new lows for the year against the Canadian dollar (~CAD1.2930), the US dollar’s bounce ran out of steam near CAD1.3160, the (61.8%) retracement objective of the slide that began on November 4 near CAD1.3300. Initial support is now seen near CAD1.3080 and then CAD1.3050. The greenback fell to a five-day low against the Mexican peso near MXN20.2370 but steadied in the European morning. Resistance may be encountered in the MXN20.40-MXN20.45 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

Overview: The S&P 500 and NASDAQ set new all-time highs yesterday, but the continued outperformance of US equities have failed to lend the dollar much support. It was sold to new lows for the year yesterday against the euro, sterling, the Swedish krona, and the Australian dollar.

FX Daily, August 24: Markets Prove Resilient to Start New Week

FX Daily, August 24: Markets Prove Resilient to Start New Week

New virus outbreaks in Europe and Asia are not adversely impacting the capital markets today. Global equities are firmer. Some reports suggesting the US ban on WeChat may not be as broad as initially signaled helped lift Hong Kong shares, but nearly all the markets in the region traded higher.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

The capital markets are relatively quiet so far today as the FOMC meeting gets underway. Equity markets in the Asia Pacific region, but Japan and Australia advanced, and the regional benchmark rose for the fourth consecutive session. European stocks are a little firmer.

FX Daily, September 16: Dollar Eases Ahead of the FOMC

FX Daily, September 16: Dollar Eases Ahead of the FOMC

Overview: The dollar has been sold against nearly all the world’s currencies ahead of what is expected to be a dovish Federal Reserve, even if no fresh action is taken. The Scandis and Antipodean currencies are leading the majors.

FX Daily, October 1: Hope Springs Eternal

FX Daily, October 1: Hope Springs Eternal

Speculation that a new round of fiscal stimulus from the US is possible is encouraging risk-taking today. Many large Asian centers were closed for holidays today, and a technical problem prevented the Tokyo Stock Exchange from opening.

FX Daily, November 12: Nervous Calm in the Capital Markets

FX Daily, November 12: Nervous Calm in the Capital Markets

There is a nervous calm in the capital markets today. The equity rally in the Asia Pacific region stalled to end an eight-day rally, though the Nikkei’s rally remains intact.

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

Overview: Profit-taking, perhaps spurred by disappointing retail sales figures, sent Chinese equity markets down by 4.5%-5.2% today, the most since early February. It appears to be triggering a broader setback in equities today. The Hang Seng fell 2%, and most other markets in the region were off less than 1%.

Tags: #USD,ASEAN,Brexit,China,Currency Movement,Featured,Japan,newsletter,U.K.