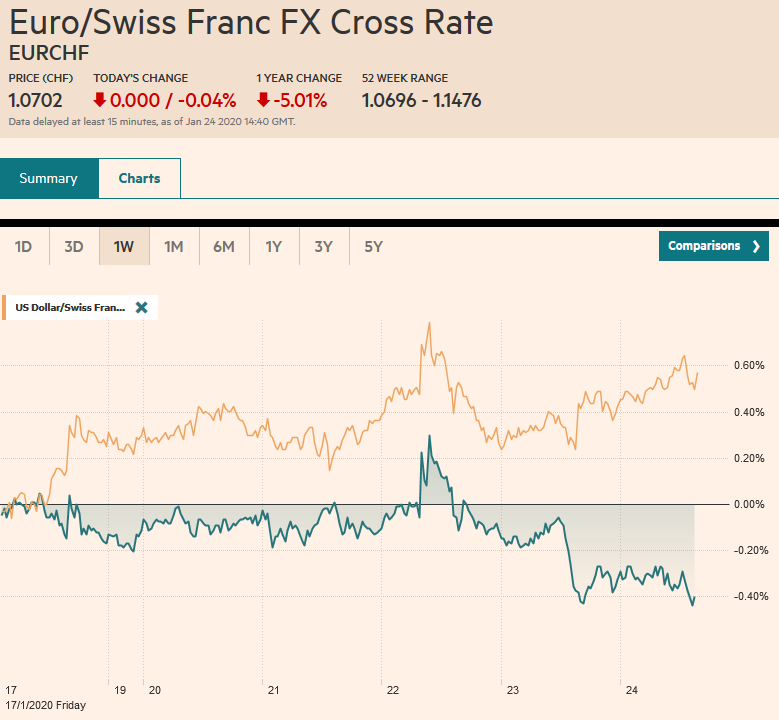

Swiss Franc The Euro has fallen by 0.04% to 1.0702 EUR/CHF and USD/CHF, January 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The new coronavirus in China has moved into the vacuum left by the US-China trade agreement and clear indications that the Bank of Japan, the European Central Bank, and the Federal Reserve are on hold as investors searched for new drivers. The World Health Organization refrained from calling it a public health emergency even though China has dramatically stepped up its efforts to contain the new virus. Many Asian markets are closed for the Lunar New Year, but equities Japan, Hong Kong, Australia, and India eked out small gains. Europe’s Dow Jones Stoxx 600 jumped 1.25%, its

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of England, China, EMU, Featured, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.04% to 1.0702 |

EUR/CHF and USD/CHF, January 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The new coronavirus in China has moved into the vacuum left by the US-China trade agreement and clear indications that the Bank of Japan, the European Central Bank, and the Federal Reserve are on hold as investors searched for new drivers. The World Health Organization refrained from calling it a public health emergency even though China has dramatically stepped up its efforts to contain the new virus. Many Asian markets are closed for the Lunar New Year, but equities Japan, Hong Kong, Australia, and India eked out small gains. Europe’s Dow Jones Stoxx 600 jumped 1.25%, its biggest increase since mid-December, if sustained, helped by preliminary PMI readings that lend credence to arguments that the worst may be behind the eurozone. It is recouping the losses of the last four sessions and is turning higher for the week. It would be the sixth weekly advance in the past seven. US shares are also trading firmer. After a strong recovery yesterday, the S&P 500 appears poised to gap higher at the opening. Again, buying on the dip strategy is being rewarded. Rising stocks sap the demand for bonds, and benchmark yields are 1-2 basis points higher in Europe and the US. Fading speculation of a Bank of England rate cut helped lift sterling to near three-week highs (~$1.3175) before the rally fizzled. The euro remains pinned near seven-week lows seen yesterday (~$1.1035). More broadly, the US dollar is little changed against the major currencies on the day, while holding on to weekly gains against most but sterling and the yen. Emerging market currencies are firm with the JP Morgan Emerging Market Currency Index is steady to higher, but is off about 0.35% on the week. Gold is a little heavy but is fairly flat with this week’s settlements in a tight range between $1558 and $1562. March WTI has stabilized after falling more than 5% over the past three sessions. |

FX Performance, January 24 - Click to enlarge |

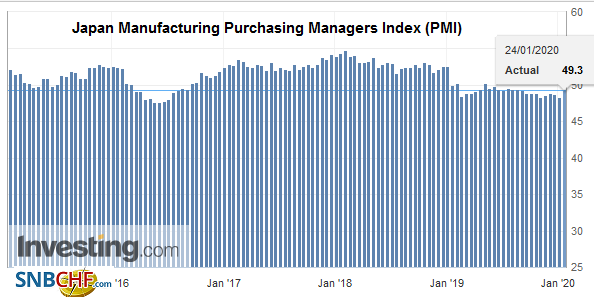

Asia PacificChina has stepped up its efforts to contain the new coronavirus. Travel for some 40 mln people has been restricted covering at least ten cities. Incidents have now been reported in 32 of 34 provinces. China appears to be responding in a more transparent way than the experience with SARS in the early 2000s. Market participants are already turning their attention to the possible economic fallout. The SARS crisis saw Chinese GDP fall by around two percentage points. Toward the end of next week, after Chinese returns from the Lunar New Year, it will report the official PMI. The contagion is expected to hit services harder than manufacturing. It will also add to the typical distortion of the data at the start of the calendar year. The underlying slowing of the Chinese economy, the continued protests in HK, the recent election results in Taiwan, and now this virus are surely testing the leadership of President Xi. Japan reported December CPI figures and the preliminary January PMI. Japan’s inflation ticked up with the headline reaching 0.8%, an eight-month high. The core measure, which excludes fresh food, rose from 0.5% to 0.7%. The increase appears to reflect the sales tax increase. The PMI reflected an economy rebounding after the sales tax and typhoons. The composite PMI rose to 51.1 from 48.6, a five-month high. While manufacturing remains below the 50 boom/bust level (at 49.3), the pace of contraction moderated from 48.4 in December. The service PMI rose to 52.1 from 49.9. |

Japan Manufacturing Purchasing Managers Index (PMI), January 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The dollar is virtually flat against the yen today (~JPY109.50). It has hardly moved more than 10 ticks away from JPY109.55. The technical indicators have turned lower for the dollar, but this does not preclude a retest of the JPY110 area early next week. Support is seen near JPY109.30. The Australian dollar has risen in three sessions so far this year, and yesterday’s 0.0.4% gain was one of them. On the week, the Aussie is off about 0.6%. It is the fourth consecutive weekly decline.The price action warns that a low is probably not in place, and near-term potential extends toward $0.6800. The onshore yuan market is closed, but in the offshore market, the yuan (CNH) has softened a little to bring this week’s loss to a little more than 1%, the largest decline since last September.

EuropeThe eurozone economy seems to be on the mend, and although the dovish spin to Lagarde’s comments yesterday seemed to be more about trying to explain the price action, i.e., the euro’s losses rather than arguably a robust understanding of what she said. In fact, she recognized a “modest improvement in underlying inflation,” and continued to expand on the idea that while downside risks remain, they have diminished. |

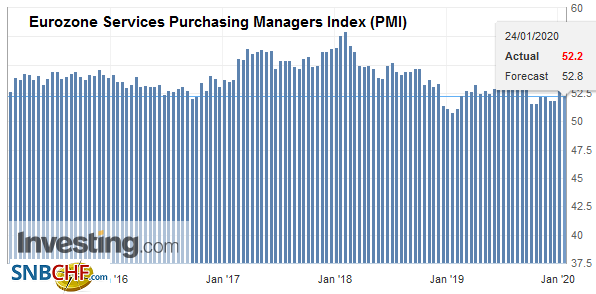

Eurozone Services Purchasing Managers Index (PMI), January 2020(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

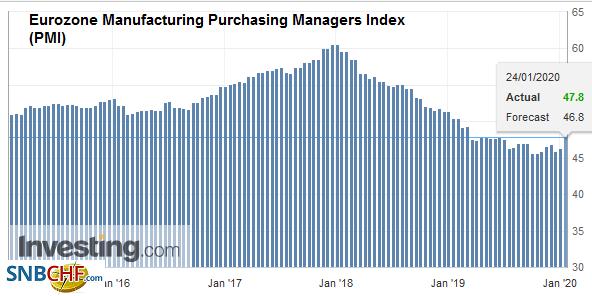

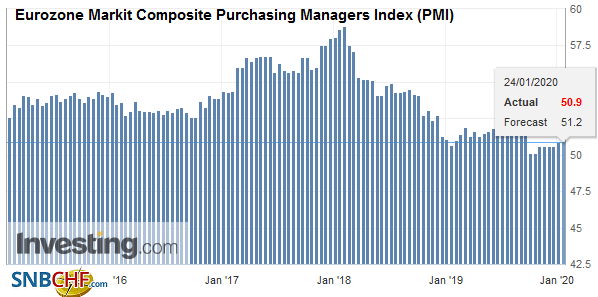

| Germany’s flash PMI was better than expected, but the strikes in France weighed on the service sector and was a drag on the aggregate reading. Germany’s manufacturing PMI rose to 45.2 from 43.7. While still obviously below 50, it is at its best level in 11-months and has edged higher in three of the past four months. The service sector remains resilient and improved to 54.2 from 52.9. The composite rose to a five-month high of 51.1 from 50.2. New business grew for the first time in seven months, and manufacturing orders saw the smallest decline in 15 months.The French manufacturing PMI rose to 51.0 from 50.4, but the service PMI fell to 51.7 from 52.4 (and was a larger decline than expected). The composite PMI eased to 51.5 from 52.0. The EMU aggregate manufacturing PMI rose to 47.8 from 46.3. It is the highest since last April. The service PMI fell to 52.2 from 52.8. This left the EMU composite reading unchanged at 50.9. |

Eurozone Manufacturing Purchasing Managers Index (PMI), January 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The strength of the UK PMI pushed the market further in the direction it was going and that as to downgrade the chances of a rate cut next week. The manufacturing PMI rose to 49.8 (from 47.5), and the service PMI improved to 52.9 (form 50.0). This succeeded in lifting the composite to 52.4 (from 49.3), which is the strongest since September 2018. At the end of last week, the derivatives market discounted about a 70% chance of a cut next week. The odds had fallen to a little more than 60% as of yesterday, and today the odds are around 50/50. |

Eurozone Markit Composite Purchasing Managers Index (PMI), January 2020(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

However, the euro and sterling have been unable to sustain even modest upticks today. The euro is making new lows since early December and appears to be headed for a test of last November lows in the $1.0980 area. This will be the fourth consecutive weekly loss for the euro, which finished last year a little above $1.12. Sterling initially moved above yesterday’s highs but has reversed lower to take out yesterday’s lows. Technically, it could be a key reversal, and a close below yesterday’s low (~$1.3100) would give a decidedly negative tone to start the new week. Initial support is seen near $1.3030-$1.3050. There are two option expires of note for sterling today. One if for a little more than GBP585 mln at $1.31, and the other is for GBP510 mln at $1.3150.

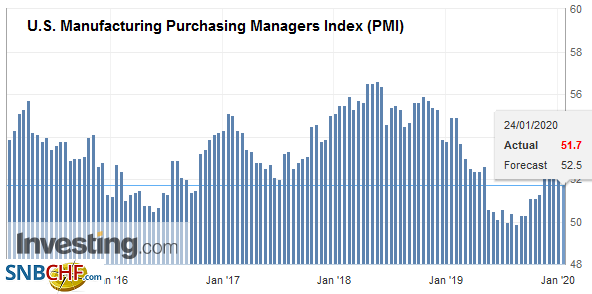

AmericaThe US sees its flash January PMI. It is expected to be little changed from the December readings, which put the manufacturing sector at 52.4 and the service sector at 52.8. The composite stood at 52.7 in December, the highest since last April. The FOMC holds its first meeting of the new year next week, and it should be without much fanfare. The first estimate of Q4 GDP will also be a highlight. The Atlanta and NY, Fed GDP trackers, have growth below 2% at an annualized pace, and bank forecasts appear a little higher than the trackers. |

U.S. Manufacturing Purchasing Managers Index (PMI), January 2020(see more posts on U.S. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

In Canada, retail sales in November are expected to recover from the unexpectedly sharp decline in October sales (-1.2%). Economists forecast that half of the loss was recouped at the headline level and nearly completely offset when autos are excluded. Mexico reports monthly economic indicator for November. It has fallen in five of the six months through October. However, the economy appears to have bounced back, and the median forecast in the Bloomberg survey is for a 0.45 reading, which would be the strongest since May 2018.

Follow-through buying of the Canadian dollar has been limited after yesterday’s upside reversal. Demand for US dollars re-emerged near CAD1.3120. The intraday technicals are stretched for the US dollar, and chart resistance is seen near CAD1.3160. That said, there is a $625 mln option at CAD1.3150 that expires today. The greenback has gained about 0.5% against the Mexican peso this week. The high yields offset the domestic policy risks to attract financial flows. The dollar did spike to around MXN18.85 yesterday and briefly traded above the 20-day moving average for the first time in a couple of weeks. However, the dollar was sold into the bounce, and it finished below MXN18.80.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Bank of England,China,EMU,Featured,newsletter